What Is A Consumer Loan?

A consumer loan is a type of credit provided to a consumer to help them finance only a set of specific expenditures. Generally, one may secure this kind of loan, i.e., the borrower has to provide a certain asset as a guarantee, or it may be unsecured too based on the loan’s monetary value, i.e., no asset backing of the borrower is required.

Borrowers can use this to reduce their debt burden through consolidated loans. This process is also called refinancing, and people do this to get rid of the debt burden faster by availing of refinance loans at a cheaper interest rate. Personal loans also belong to consumer loans, which help people fulfil experiences like traveling abroad, completing their education, etc.

- A consumer loan is a credit type offered to customers to aid them in financing only specific expenditures.

- Consumer loans are mortgages, credit cards, auto loans, education loans, refinance loans, home equity loans, and personal loans.

- The documents required for consumer loans are identity proof, address proof, income proof, and other documents such as a current credit card or loan statement.

- The minimum eligibility to apply for a consumer loan is 21, and the maximum is up to 60 years.

Consumer Loan Explained

A consumer loan is a sum offered to customers to buy personal devices, home appliances or gadgets. One can use a consumer loan from banks under criteria that differ from bank to bank. Some banks allow consumer loans to individuals above 21 years and earn above a certain sum on a monthly basis.

In the modern era, even a physical presence at the bank’s office is not required as customers can apply through the website for an online consumer loan and present the required documents if they are eligible. It is also important to note that these loans can be secured as a fixed loan or a revolving credit account which customers can use at their own discretion.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

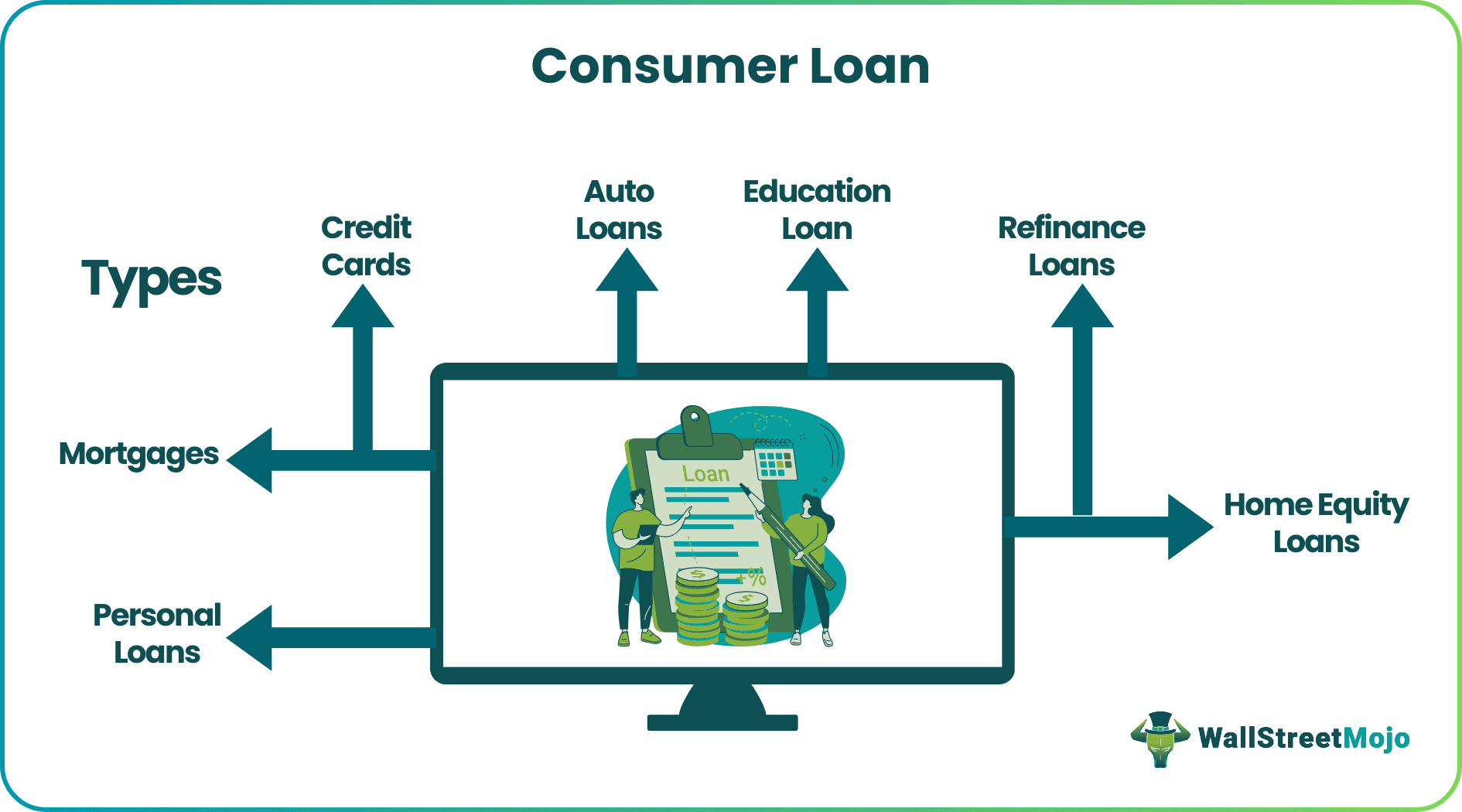

Types

Let us understand the different types of conventional and online consumer loans through the discussion below.

- Mortgages: Mortgages are typically linked to buying a new house. Banks give this type based on the credit score and the ability of down payment, which a borrower has to facilitate buying a new home.

- Credit Cards: This is the most widely used and popular consumer loan. A credit card helps borrowers purchase their daily needs, from apparel to groceries, through a credit line granted to them by the credit card company. However, the interest charges are a bit high in this case, and failing to pay attracts a high level of penalty.

- Auto Loans: Auto loans are typically meant for buying vehicles. These are generally available at the bank or the car dealership itself.

- Education Loans: Education loans are targeted to fulfill the education needs of students in terms of paying their college or tuition fees. It helps students pursue their education, and the loan repayment starts when they have graduated from college.

- Refinance Loans: A refinances the loan, as the name suggests, is used to refinance an already existing loan. For example, one can use it to refinance their car loans, education loans, house loans, and even credit cards. A refinance loan ideally has a fixed payment at a lower interest rate, which helps the borrower close the earlier loan.

- Home Equity Loans: This is a kind of consumer loan where one can utilize the equity value of one’s home to borrow money. Typically, this is used for making improvements to the houses.

- Personal Loans: Personal loans cater to the buyer’s daily needs and can work on various purchases. Personal loans allow the borrower to do anything from repairs to business investments.

Examples

Let us understand the concept in depth with the help of a couple of examples.

Example #1

Martha wanted to purchase a car to commute to work as public transport took too much time and she could not travel to other places with ease. However, since she could not afford to pay the whole amount for a car, she decided to acquire a car loan from her bank.

Through the bank’s website, Martha applied for an online consumer loan. After uploading all the required documents, a representative from the bank delivered further details.

The loan was a fixed interest loan with a repayment period of 4 years with an interest rate of 5.5%. She availed the loan and purchased a brand new car to commute to work and made her commute easier.

Example #2

In February 2023, consumer loans such as mortgage, credit card delinquencies, and auto loans rose from $1.3 trillion to $16.9 trillion in one year. It is believed to be from the defaults of payments from consumers after the aggressive rate hiking campaign by the Feds.

The most concerning factor among all was that the increase in outstanding payments rose drastically despite the fact that new loans or originations declined in the same period.

Even student loans which drastically dip during the pandemic accounted for over $1.6 trillion in the fourth quarter of 2022.

Eligibility

The minimum eligibility to apply for a consumer loan is 21, and the maximum can go up to 60 years of age. If one is salaried, the maximum age limit is 60 years. However, if some are self-employed professionals, they can go till 65 years of age. Also, this depends on bank to bank, and factors such as credit score are also considered.

However, depending on the bank and laws at the state level, the minimum monthly recurring income criteria differs for consumer loan processing.

Interest Rates

It is important to know the interest rates for consumer loan processing beforehand. It gives the individual an idea of how much extra they would be spending to purchase the product or asset they are availing of the loan.

The below rates are based on rates levied in the USA: –

- Personal loans = 5% – 36% depending on credit score

- Education loans = 4.5 % – 6%

- Credit card = 13% to 16%

- House loan = 3.5% – 4%

- Refinance loan = 3.5% – 4%

- Auto loans = 5.3% – 6%

Documents Required

Irrespective of applying for an online consumer loan or a conventional loan from the branch office of a bank, the below-mentioned documents would be required to be presented by the borrower.

- Identity Proof: Driving license, passport, state ID, birth certificate, certificate of citizenship, utility bills, etc.

- Address Proof: Current rent agreement or any documents with the address mentioned.

- Income Proof: Banks statement, tax returns, and payslips.

- Other Documents: Current credit card or loan statement, an alternate source of income proof, current rent, or mortgage.

Uses

Based on the spending patterns, consumer’s individual spending psychology, the uses of an conventional or online consumer loan differs. Let us understand them through the explanation below.

- Refinance a current loan outstanding.

- Pursue education and thus help in the payment of tuition fees.

- Buying a car for private or commercial use.

- Building a house or going for improvement or repairs.

- Aim to purchase daily needs like groceries or clothing.

Benefits

Let us understand the benefits of consumer loan processing through the discussion below.

- Easy access to funds whenever the need arises and in times of critical requirement.

- It offers to enhance financial flexibility ranging from various types of loans.

- It offers decent interest rates and is versatile.

- They are good when it comes to debt consolidation.

- One can borrow the amount one requires, and loan approval is quick.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

What happens if one cannot make payments on consumer loans?

If one cannot make payments on these loans, they may be charged with late fees and penalties; hence this negatively impacts the credit score.

What is the difference between credit cards and consumer loans?

A credit card is for smaller purchases that one can pay back immediately. In contrast, one can use a consumer loan for larger purchases that one can pay over a longer duration.

What are commercial loans vs consumer loans?

A commercial loan is a financial tool that allows business owners to appeal for short-term capital requirements. One can use the approved amount to boost the working capital, obtain new machinery, construct new infrastructure, or fulfill operational costs and other expenditures. A consumer loan is offered to one or more individuals for household, family, and additional personal spending. It does not involve a small business, farm loan, or home mortgage.

What is a BB&T consumer loan?

BB&T consumer loans provide secured and unsecured loans that one may use to finance their startup expenditures, retain cash flow, and make changes for various other business expenditures. These lumpsum loans include monthly repayments with fixed or variable interest rates.

Recommended Articles

This article is a guide to what is Consumer Loan. Here we explain its examples, types, interest rates, documents required, and eligibility. Also, you can learn more about it from the following articles: –