Part of our Capital Budgeting guide

Cost-Benefit Analysis Definition

The cost-benefit analysis compares the costs and benefits of a project and then makes a decision on whether or not to proceed with the project. The project’s costs and benefits are measured in monetary terms after adjusting for the time value of money, thus providing a true picture of the costs and benefits. Net Present Value and Benefit-Cost Ratio are the two most common methods of doing a cost-benefit analysis. The NPV model chooses the project with the highest NPV. The benefit-cost ratio model chooses the project with the highest benefit-cost ratio.

How to do Cost Benefit Analysis?

When doing the cost-benefit analysis, there are two main methods of arriving at the overall results. These are Net Present Value (NPV) and the Benefit-Cost Ratio (BCR).

#1 – Net Present Value Model

The NPV of a project refers to the difference between the present value of the benefits and the present value of the costs. If NPV > 0, then it follows that the project has economic justification for going ahead.

It is represented by the following equation:

NPV = ∑ Present Value of Total Future Benefits – ∑ Present Value of Total Future Costs

#2 – Benefit-Cost Ratio

On the other hand, the Benefit-Cost provides value by calculating the ratio of the sum of the present value of the benefits associated with a project against the sum of the present value of the costs associated with a project.

BCR = ∑ Present Value of Total Future Benefits / ∑ Present Value of Total Future Costs

The greater the value above 1, the greater are the benefits associated with the alternative considered. If using the Benefit-Cost Ratio, the analyst has to choose the project with the greatest Benefit-Cost Ratio.

Let’s take a quick look at the cost-benefit analysis suggesting a comparison between the two:

| Project Alternative 1 | Project Alternative 2 |

|---|---|

|

|

From this cost-benefit analysis, it can be seen that while both investment proposal provides a net positive outcome. However, the NPV and BCR methods of obtaining results provide slightly varied outcomes. Using NPV suggests investment option 1 provides a better outcome as the NPV of $70 million is greater than the NPV of option 2 ($ 5 million). On the other hand, applying the BCR method, option two would be preferred as a BCR of 2.22 is greater than the BCR of 1.88.

In cost-benefit analysis, the overall result may be determined by considering the costs involved in option one, which are much greater, or determined by considering the overall much greater benefits (in monetary terms) obtained by choosing alternative 1. Hence what we can see is that the results of Cost-Benefit Analysis are not close-ended. Presenting both forms of analysis by different methods may be most appropriate as the authorities can weigh the decision based on all perspectives.

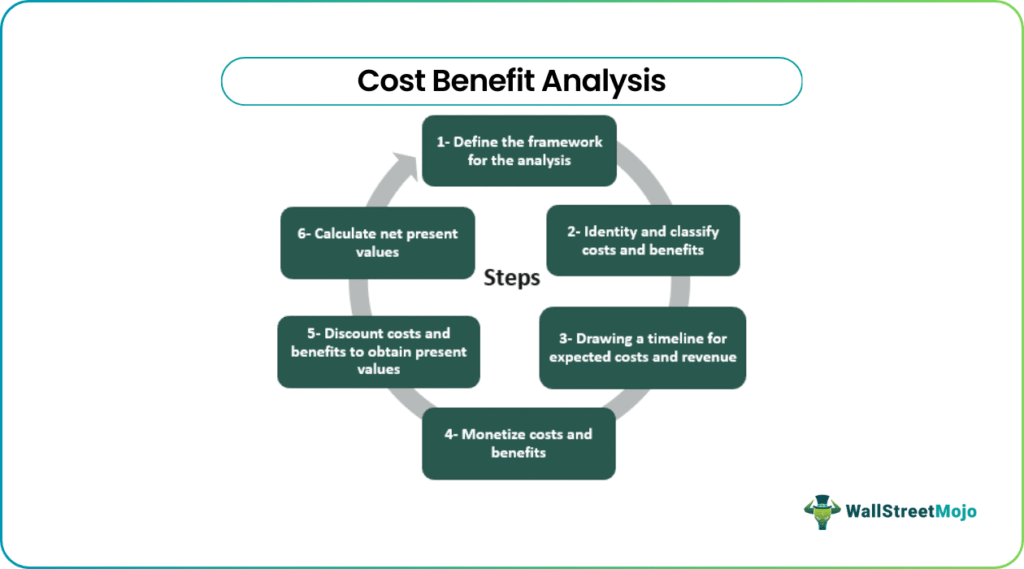

Steps of Cost-Benefit Analysis

We all know it’s quite simple to make an investment decision when the benefits overshadow the costs, but only a few of us know the other key elements that go into the analysis. The steps to create a meaningful model are:

The steps to create a meaningful Cost-Benefit Analysis model are:

- Define the framework for the analysis.

Identify the state of affairs before and after the policy change or investment on a particular project. Analyze the cost of this status quo. We need to first measure the profit of taking up this investment option instead of doing nothing or being on ground zero. Sometimes the status quo is the most lucrative place to be in.

- Identity and classify costs and benefits.

It is essential to costs and benefits are classified in the following manner to ensure that you understand the effects of each cost and benefit.- Direct Costs (Intended Costs/Benefits)- Indirect Costs (Unintended Costs/Benefits),- Tangible (Easy To Measure And Quantify)/- Intangible (Hard To Identify And Measure), And- Real (Anything That Contributes To The Bottom Line Net-Benefits)/Transfer (Money Changing Hands)

- Drawing a timeline for expected costs and revenue.

When it comes to decision making, timing is the most crucial element. Mapping needs to be done when the costs and benefits will occur and how much they will pan out over a phase. It solves two major issues. Firstly, a defined timeline enables businesses to align themselves with the expectations of all interested parties. Secondly, understanding the timeline allows them to plan for the impact that the cost and revenue will have on the operations. This empowers businesses to better manage things and take steps ahead of any contingencies.

- Monetize costs and benefits.

We must ensure to place all costs and all benefits in the same monetary unit.

- Discount costs and benefits to obtain present values.

It implies converting future costs and benefits into present value. It is also known as discounting the cash flows or benefits by a suitable discount rate. Every business tends to have a different discount rate.

- Calculate net present values.

It is done by subtracting costs from benefits. The investment proposition is considered efficient if a positive result is obtained. However, there are other factors to be considered, as well.

Principles of Cost-Benefit Analysis

- Discounting the costs and benefits – The benefits and costs of a project have to be expressed in terms of equivalent money of a particular time. It is not just due to the effect of inflation but because a dollar available now can be invested, and it earns interest for five years and would eventually be worth more than a dollar in five years.

- Defining a particular study area – The impact of a project should be defined for a particular study area. E.g., A city, region, state, nation, or the world. It’s possible that the effects of a project may “net out” over one study area but not over a smaller one.

- The specification of the study area may be subjective, but it can impact the analysis to a significant extent.

- Addressing uncertainties precisely – Business decisions are clouded by uncertainties. It must disclose areas of uncertainty and discretely describe how each uncertainty, assumption, or ambiguity has been addressed.

- Double counting of cost and benefits must be avoided – Sometimes though each of the benefits or costs is seen as a distinct feature, they might be producing the same economic value, resulting in the dual counting of elements. Hence these need to be avoided.

Importance of Cost-Benefit analysis

- Determining the feasibility of an opportunity: Nobody wants to incur losses in business. When a massive sum of money is invested in a project or initiative, it should at least break even or recover the cost. To determine whether the project is in the positive zone, the costs and benefits are identified and discounted to present value to ascertain the viability.

- To provide a basis for comparing projects: With so many investment choices around, there has to be a basis for choosing the best alternative. Cost-benefit analysis is one the aptest to tools to pick through the available options. When one out of the two options seems more beneficial, the choice is simple. However, a problem arises when there are more than two alternatives to evaluate. This model helps businesses to rank the projects according to their order of merit and go for the most viable one.

- Evaluating Opportunity Cost: We know that the resources at our disposal are finite, but investment opportunities are many. Cost-benefit analysis is a useful tool for comparing and selecting the best option. However, while choosing the most viable project, it is also imperative to be aware of the Opportunity Cost or the cost of the next best alternative foregone. It helps businesses to identify the benefits that could have arisen if the other option was chosen.

- Performing Sensitivity Analysis for the various real-life scenarios: Situations are not always the same, and the exact outcome cannot be predicted. The discount rate can be tested over a range. Sensitivity analysis can be instrumental in improving the credibility of a Cost-benefit analysis and is mainly used where there is ambiguity over the discount rate. The investigator may change the discount rate and the horizon value to test the sensitivity of the model.

Limitations

Like every other quantitative tool, Cost-benefit Analysis also has certain limitations: A good CBA model is the one which circumvents these hurdles most effectively: Few of the limitations are:

- Inaccuracies in quantifying costs and benefits – A cost-benefit analysis requires that all costs and benefits be identified and appropriately quantified. However, specific errors, such as accidentally omitting certain costs and benefits due to the inability to make a forecast, may result in difficult causative relationships, thereby giving an inaccurate model. Moreover, the ambiguities over assigning monetary values further lead to inefficient decision-making.

- An element of subjectivity – All costs and benefits cannot be quantified easily. There are certainly other elements involved that call for subjectivity. The monetary value of benefits such as employee satisfaction, client satisfaction, or costs such as reduction of trust, etc. is difficult to be ascertained. But since the standard Cost-Benefit Analysis model calls for quantification, businesses might quantify these factors, and there is a limited scope of accuracy involved. Decision-makers might get emotionally carried away, and this again results in skewed and biased analysis.

- Cost-Benefit analysis might be mistaken for a project budget – The elements involve estimation and deemed quantification; however, there are possibilities that, at some level, the Cost-Benefit Analysis model may be mistaken for a project budget. Forecasting budget is a more precise function, and this analysis can only be a precursor to it. Using it as a budget may lead to a potentially risky outcome for the project under consideration.

- Ascertaining the discount rate – A significant concern in the usage of discounting is the value pertains to the discount rate chosen. The standard method of discounting to present value is based on the timing of costs and benefits. This method of discounting s assumes that all costs and benefits occur at the end of each year (or maybe this timing is used for the ease of calculation). However, in certain scenarios, the timing of costs and benefits needs to be considered more thoroughly and in a distinguished manner. Let’s say if a cost is incurred halfway through the year or in the last quarter of the year, discounting it at the end of the year could skew the results to some extent. Thus the timing of discounting the costs and benefits needs to be adjusted depending on the life span of the project.

Recommended Articles

This article has been a guide to what is the cost-benefit analysis. Here we discuss how to do cost-benefit analysis along with examples, importance & limitations. You can also have referred to the following recommended articles to learn more about Corporate Finance –