Part of our Banking and Financial Institutions guide

What Is Basel II?

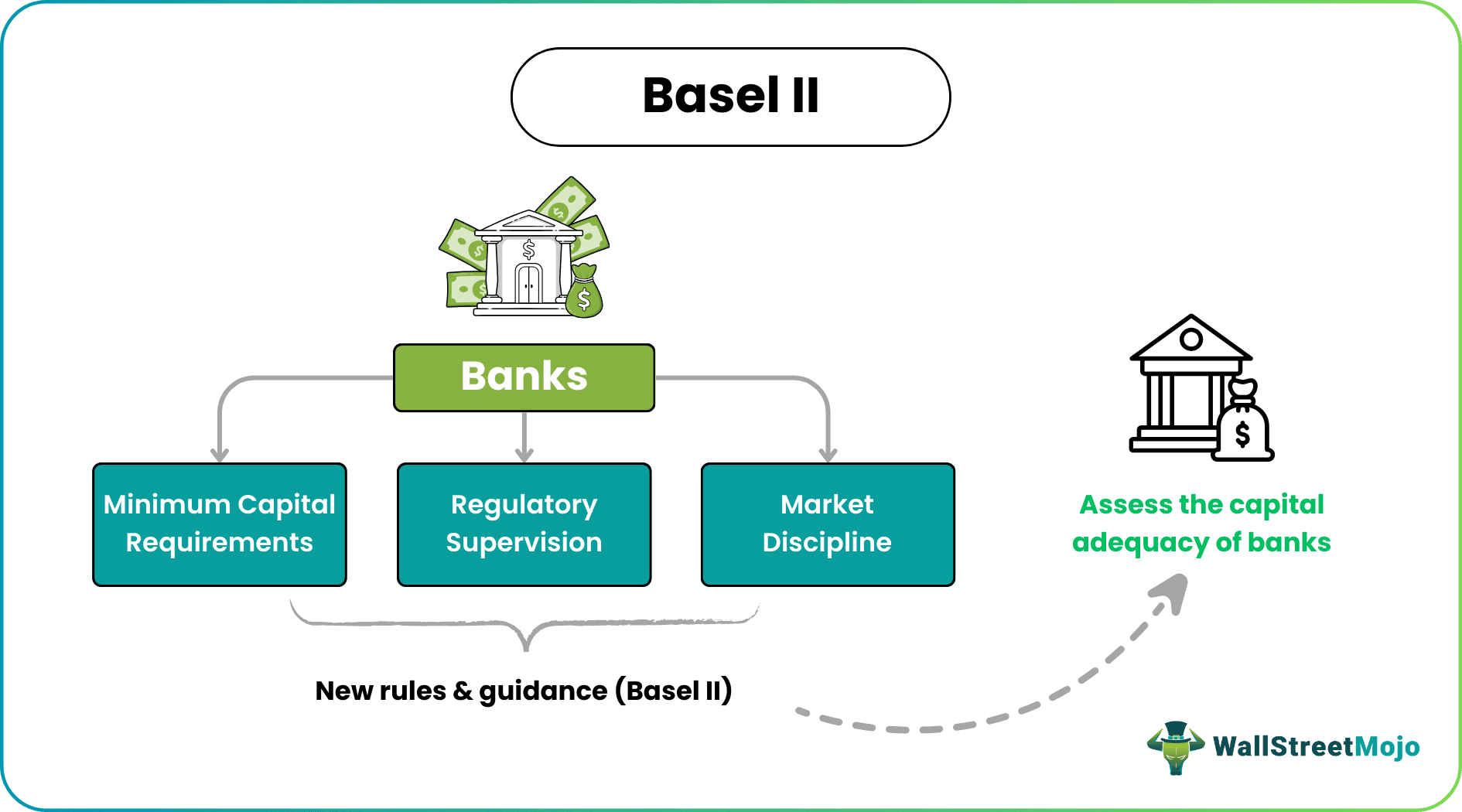

Basel II is the second set of regulations on the minimum capital requirement, supervisory review, the role, and market discipline, including disclosure created for international banks by the Basel Committee on Bank supervision to maintain a transparent and risk-free banking environment.

These norms are developed to make the banking sector more secure. It also helps the regulators to keep track of the funds that are flowing in and out of the banks and save investors’ money from being misused. Banks should always follow the best approach and invest in less risky assets.

- Basel II is the second set of rules regarding the minimum capital requirement, supervisory review, role, and market discipline, which was developed for international banks.

- Basel II’s goal is to ensure that the bank performs a thorough risk analysis of the asset they seek to invest in.

- Basel III differs from Basel II despite being inherited from Basel II. Therefore, areas, where the authorities felt extra caution should be exercised were made tougher.

- However, Basel II has shortcomings in light of the catastrophic outcomes, such as minimum capital requirements not being established. Thus, even during a severe crisis, banks can not be saved through this accord.

Basel II Explained

The banking system depends totally on trust. Investors can only gain trust when they know that their money is secured. Basel II norms are designed to prevent banks from taking risks independently and don’t respect depositors’ money. The business model of any bank is to accept deposits in the form of savings or fixed deposits and to use this capital to issue loans to individuals or businesses. So the main focus of regulators should be to check how much the inflow is vs. the outflow of capital. Basel II norms focus on the minimum capital requirement of the banks and other areas.

Objectives

- To save investors’ money in case of any risk, banks will have to set aside capital based on the assets they hold. Bank’s assets are the bank’s investments, such as issuing a loan. Basel II framework objective is to ensure that the bank does a thorough risk analysis of the asset on which they are planning to invest. So capital should be allocated considering the risk factor involved in assets.

- Earlier, Basel’s objective was to make banks concentrate only on the credit risk of the individual or organization that the bank is issuing the loan to. Nowadays, along with credit risk, a bank must also concentrate on operational and market risk.

- The disclosure requirement of the banks has been increased, which will help any market participant calculate on their own as to whether the bank is maintaining proper capital as per their asset. The objective is to open things so that if the regulators miss something, other participants can find it out.

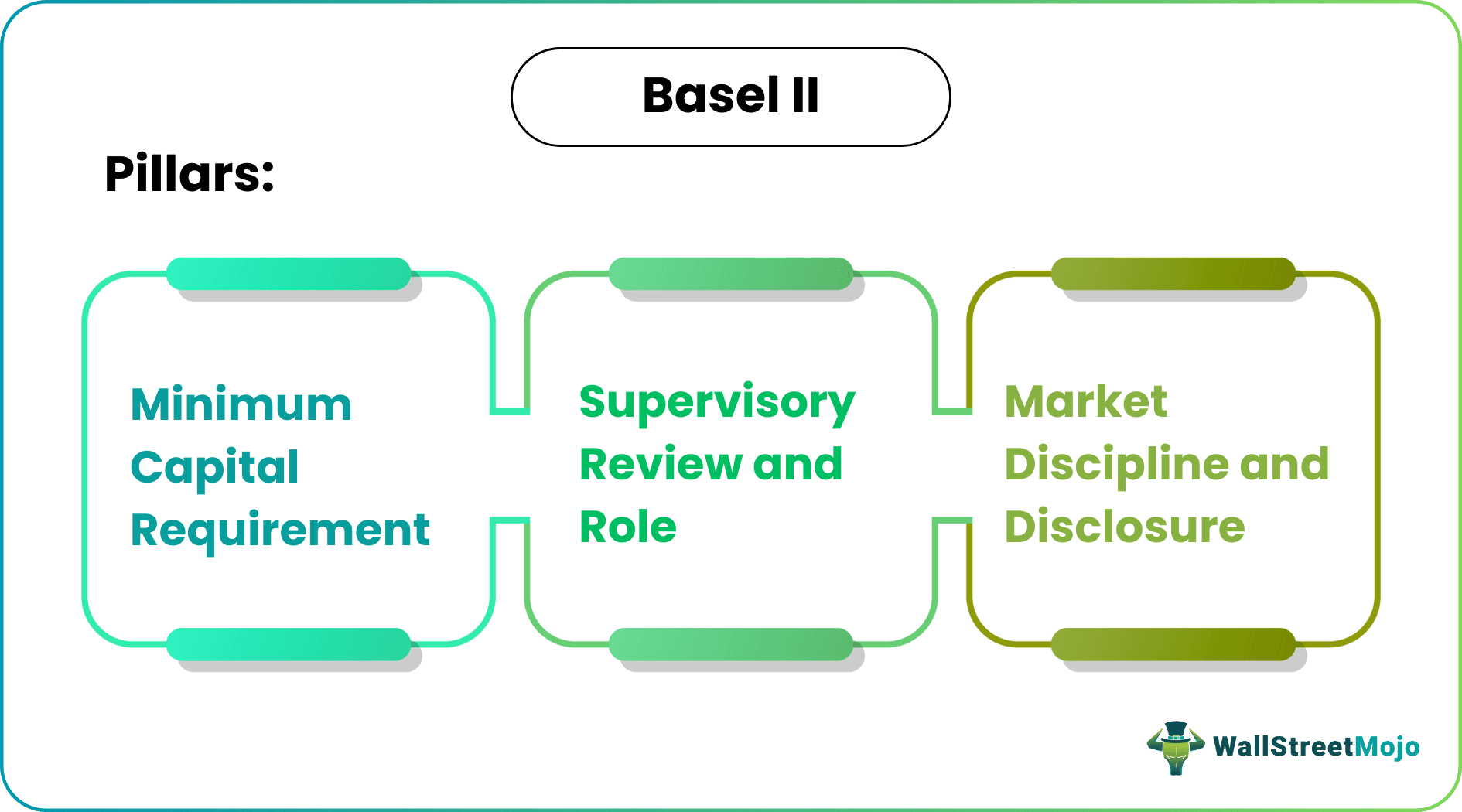

Pillars

The pillars of Basel II framework are the Minimum Capital Requirement, Supervisory Review and role, and Market Discipline and Disclosure.

#1 – Minimum Capital Requirement

This pillar ensures that the bank calculates assets based on risk, also known as risk-weighted assets. Now the bank will not consider only credit risk, but also operational risk associated with the assets and decide the capital requirement. The minimum capital requirement is 8% of the risk-weighted assets per Basel II.

#2 – Supervisory Review and Role

Regulations are of no use if proper supervision is not done. As per Basel II, it is the primary duty of the supervisor to ascertain that the bank has covered enough capital that will deal with operational, credit, and market risk of the assets that the bank has invested in. So the supervisor can intervene in the daily operations to ensure that capital doesn’t fall the desired threshold. Therefore, the review role of the supervisor should be extremely strong and should always try to maintain the capital above the required level.

#3 – Market Discipline and Disclosure

Nowadays, markets are extremely disciplined. There are informed market participants who are well informed about the minimum requirement of capital by the banks. So if any time bank drops below the desired level of capital requirement, then market participants can identify it with the disclosures made by the banks. So this helps investors to make informed decisions. Basel II has stated banks to make full and timely disclosures.

Example

The minimum capital requirement is very crutial for any bank. The one-time capital requirement was based on the asset that the bank used to hold. Each asset is not equal, risk-wise. So if we think practically, if the bank is holding a very risky asset and a very safe asset, should the capital reserve kept for default be the same for both the assets? No. It should be higher for risky investments and lower for less risky assets. However, the norm states that the banks should maintain a minimum capital reserve of 8% of risk-weighted assets.

Effects

Basel II’s main objective is to make the banking sector extra cautious while handling highly risky assets. The capital requirement is based on risk-weighted assets now, so banks will have to charge extra spread while issuing loans to lower rating individuals/businesses. So now it will be really difficult to raise money from risky businesses which is a which was a limitations of Basel II. Depositors will be more confident in the banking sector, and they will start to save more instead of spending. This will increase the capital base of the banking sector even more.

Advantages

- It has helped the banking sector be more secure due to the strict capital requirement norms.

- Strict supervision has helped many banks not deviate from the stipulated minimum capital requirement. This practice has helped banks to save themselves from the worst scenarios.

- Disclosure requirements have helped the banking sector be more transparent and have allowed investors from all over the world to make informed decisions.

Disadvantages

- Importance was lacking on the crucial capital ratios that help predict the shortfall.

- Minimum Basel II capital requirements were not set considering the extreme outcomes. Even Basel II regulations can’t save a bank in a severe crisis. The capital reserve will be useless if a bank has invested too much in risky assets and the entire market drops. There will be a bank run.

Basel 2 Vs Basel 3

- Basel III is built upon Basel II. So areas where the regulators thought that more care should be taken, were made stricter. The capital requirement is even more stringent which was a limitations of Basel II.

- Basel III considers the credit ratings of the assets that the bank is planning to invest to set up a relation between the market risk and the risk of the asset.

- Capital ratios are extremely important to find the capital status of banks. Basel III has tightened the capital ratio requirements compared to the Basel II capital requirements.

- Banks’ capital kept for risky times is divided into common equity tier 1 capital, tier 1 capital, and Tier 2 capital.

- The overall requirement of capital consisting of all three segments was 8% in Basel II. It remains the same. The changes are made inside the common equity tier 1 capital and tier 1 capital.

- The minimum common equity tier 1 capital changed from 4% to 4.5%, and minimum tier capital changed from 4% to 6%.

Frequently Asked Questions (FAQs)

Frequently Asked Questions

1. Is Basel II still in force?

u003cpu003eThe Basel Committee on Banking Supervision’s recommendations for banking rules and regulations, known as the Basel Accords, include Basel II.u003c/pu003e

2. Why did Basel II fall?

u003cpu003eBy transferring credit rating agency failings into banking regulation, the import of external credit risk assessment undercut Basel II.u003c/pu003e

3. Does Basel II have operational risk? Why?

u003cpu003eAccording to Basel II and Basel III, operational risk is the possibility of suffering a loss due to insufficient or failing internal processes, people, and systems or as a result of outside occurrences.u003c/pu003e

Recommended Articles

This has been a guide to what is Basel II. We explain its pillars, its differences with Basel III, its objectives, effects, advantages and disadvantages. You may learn more about financing from the following articles –