Part of our Credit Concepts guide

What Are The Types of Credit?

The types of credit refer to the list of credit options that borrowers can access and utilize to meet their financial requirements. They let one know of the benefits and limitations of each of the options so that individuals or institutions seeking finances or loans can choose the alternative that best suits them.

Learning about the types of credit help borrowers explore different credit options, be it in the form of credit cards instalments or loans. When businesses leverage the credit properly, they can have better cash flows, funds to hire people and resources, and also reinvestment opportunities.

- Credit means the system where the borrower obtains the money from the lender. In return, a borrower agrees to pay the interest for the duration when money is taken with the borrower and agrees to pay it back after a fixed time.

- Open Credit has the characteristics of both instalment and revolving Credit. Electricity, gas, and telephone bills are examples of available Credit.

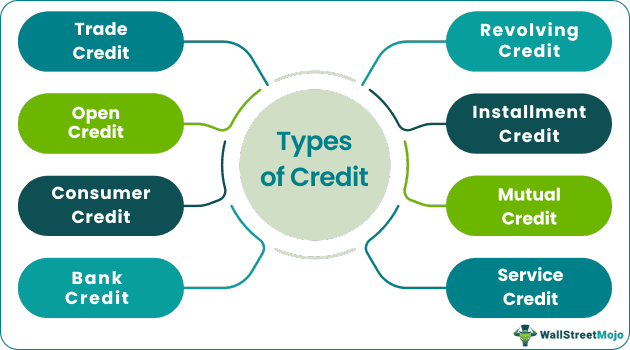

- Trade Credit, Consumer Credit, Bank Credit, Revolving Credit, Open Credit, Installment Credit, Mutual Credit, and Service Credit are the types of Credit.

Types of Credit Explained

Types of credit allows individuals and institutions to learn about the opportunities and restrictions that each and every credit alternative offers. Credit is the arrangement where the borrower receives the money from the lender and, in turn, agrees to pay the interest for the period during which money is held with the borrower and promises to repay after a predetermined time.

From an installment credit to a revolving one, the credit types differ widely. Each of these options has their own set of pros and cons, which help fund seekers check if a particular type fits their requirements. The one that fits could be chosen and this is what makes differentiating between the credit types useful.

Some of the types of credit include mortgage loans, letters of credit, bank guarantees, consumer credit, trade credit, etc.

Top 8 Credit Types

The credit types exist in various forms. Some of them have been listed below followed by their detailed explanation:

- Trade Credit

- Trade Credit

- Bank Credit

- Revolving Credit

- Open Credit

- Installment Credit

- Mutual Credit

- Service Credit

#1 – Trade Credit

Trade Credit refers to credit in business dealings like selling goods on credit where the customer promises to pay money later, buying goods on credit where we, the customer of the supplier, promise to pay to the supplier on a later date. It is given based on the borrower’s financial capability, i.e., credit taker. In some cases, it is given based on a relationship with the person asking for credit, or it depends upon business rules. In a large organization, the credit rules are the same for all the customers.

#2 – Trade Credit

Consumer Credit refers to money, goods, or services provided on the agreement with the consumer to pay later with the charges for using the credit. Consumer credit is specifically designed for consumers to give them various benefits. Consumer credit involves the hire purchase goods, personal loans, credit insurance, vehicle finance, etc. consumer credit is given on the basis creditworthiness of the consumer, and rules of credit are the same for all the parties. Purchasing goods on EMI is also an example of consumer credit. The banks gives the overdraft facility also falls under consumer credit..

#3 – Bank Credit

Bank Credit is an extension of consumer credit. In bank credit, the bank gives loans and credit facilitates to clients. Consumer credits are given based on creditworthiness, analysis of financial statements, and value of the asset given by consumers as security. Examples of consumer credit are mortgage loans, cash credit facility, housing loans, etc., letter of credits, bank guarantee, discounting of bills of exchange also falls under the bank credit facility.

#4- Revolving Credit

Revolving credit involves the continuous credit in which the lender gives the extension of credit to the borrower so long as the account is regular and open by regular payments like in case of credit card the credit is given regularly and limit of credit is given and payment to be made on monthly or quarterly basis. And the account will continue till it is closed, i.e., credit is extended every month.

#5 – Open Credit

Open Credit has a feature of both installment credit and revolving credit. If an open credit limit is not set, the credit card is given, and then one will use it throughout the month, and at the end of the month, the bill will be given to the cardholder to re-pay and continue the service. Electricity bills, gas bills, telephone bills, etc., are examples of available credit, i.e., use first and then pay later and available for all.

#6 – Installment Credit

Installment credit is the extension of bank credit. When we obtain credit from banks by way of loan, the bank sets the fixed monthly installment as repayment type of loan along with interest up to a certain period till the loan gets re-paid along with interest. The bank or finance company charges a penalty if the borrower cannot pay the installment.

#7 – Mutual Credit

In mutual credit, money is not used as in this case. If one person owes another person for something that another person also owes to the first one, the credit becomes mutual credit. So credit gets canceled with each other, and in case a balance remains after that, then the same is settled by the mode of cash or equivalent. Like in business, one person is a creditor and a debtor. Hence, they mutually settle the payments.

#8 – Service Credit

In-service credit, the credit is given for services availed earlier. Like lawyers ask for final fees once the case is over, the accountants charge after filing the returns. Electricity bills, telephone bills, gas bills, and post-paid bills are examples of service credit. Service credit borrowers can pay after availing of the service at fixed intervals. But if the service receiver fails to pay at fixed intervals, it may cancel services or charge a penalty for late payments.

Frequently Asked Questions (FAQs)

How many types of credit scores are there?

Lenders and financial institutions use various types of credit scores to assess an individual’s creditworthiness. The different kinds of credit scores are FICO Scores,

Vantage Scores, industry-specific Score, and Educational Credit Scores.

What are the types of credit risk?

Credit default risk, Probability of Default (POD), Exposure at Default (EAD), Loss Given Default (LGD), and Concentration risk are the types of credit risk.

What are the types of credit policies?

Lenient and restrictive are the two types of credit policies. The lenient credit policies possess few rules, and the restrictive credit policies have strict regulations over the terms. The policy components comprise customer information, credit limits, creditworthiness, cash discounts, credit terms, and collection period.

Recommended Articles

This has been a guide to what are Types of Credit. Here, we explain the concept along with a list of top 8 types of credit that borrowers can consider. You may learn more about financing from the following articles –