Part of our Banking and Financial Institutions guide

What is Basel I?

Basel I, also known as the 1988 Basel accord, is the standard set of banking regulations on the minimum capital requirement for banks based on certain percentages of risk-weighted assets. These rules are adopted and implemented to minimize credit risk.

The banks that operate internationally must maintain a minimum capital of 8% on risk-weighted assets. So far, three sets of regulations have been introduced, of which Basel I norms were first followed by Basel II and Basel III. Together, all of them are called Basel Accords. These norms build confidence among international investors, customers, the government, and other stakeholders.

- Basel I is one of the most common banking regulations based on specific percentages of risk-weighted assets to reduce credit risk.

- Basel I focused on risk-weighted assets and credit risk and benefitted from making the global banking system more stable by improving how the government ran the nation’s capital.

- Assets in Basel I are classified as per their risks ranging from 0-100%. Basel I focuses more on the book value of assets rather than the market value.

Basel I Explained

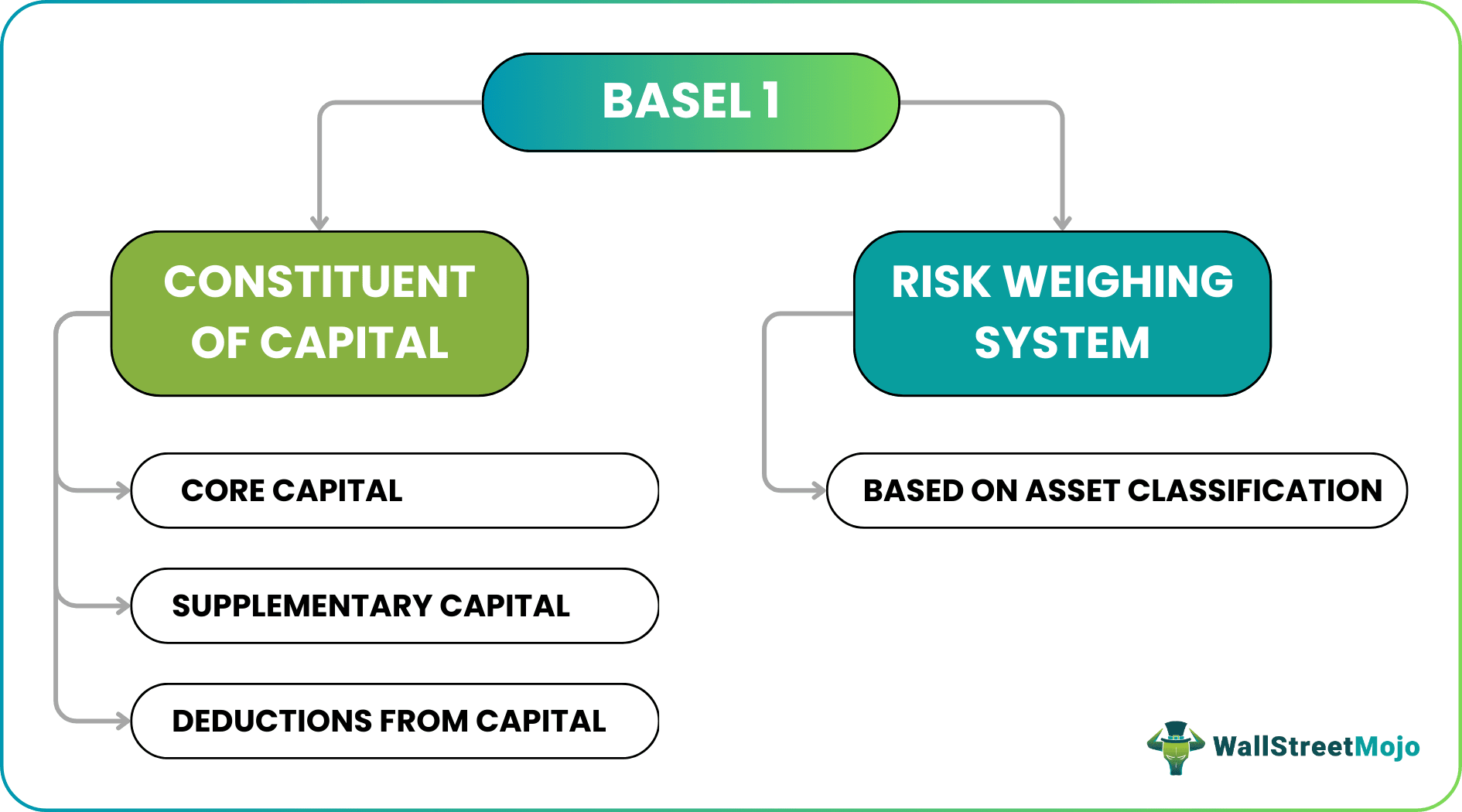

The Basel I accord primarily focuses on risk-weighted assets and credit risk. Here the assets are classified based on the risks associated with them. The risk may range from 0% to 100%. Under this charter, the committee members agree to implement a full Basel accord with active members. Under the Regulatory Consistency Assessment Programme (RCAP), the committee publishes semi-annual reports on members’ progress in implementing the Basel standards. They also keep updating all the G-20 countries involved as members. Banks’ capital is classified under Basel I accord, i.e., tier I and tier II. Tier I capital is the capital, which is more permanent and makes up at least 50% of the bank’s total capital base.

In contrast, tier-II capital is fluctuating and more temporary. Members of the Basel accord must implement this regulation in their home countries. This accord lowers the bank’s risk profile and drives investment back into banks distrusted post subprime loan of 2008.

Capital Requirements

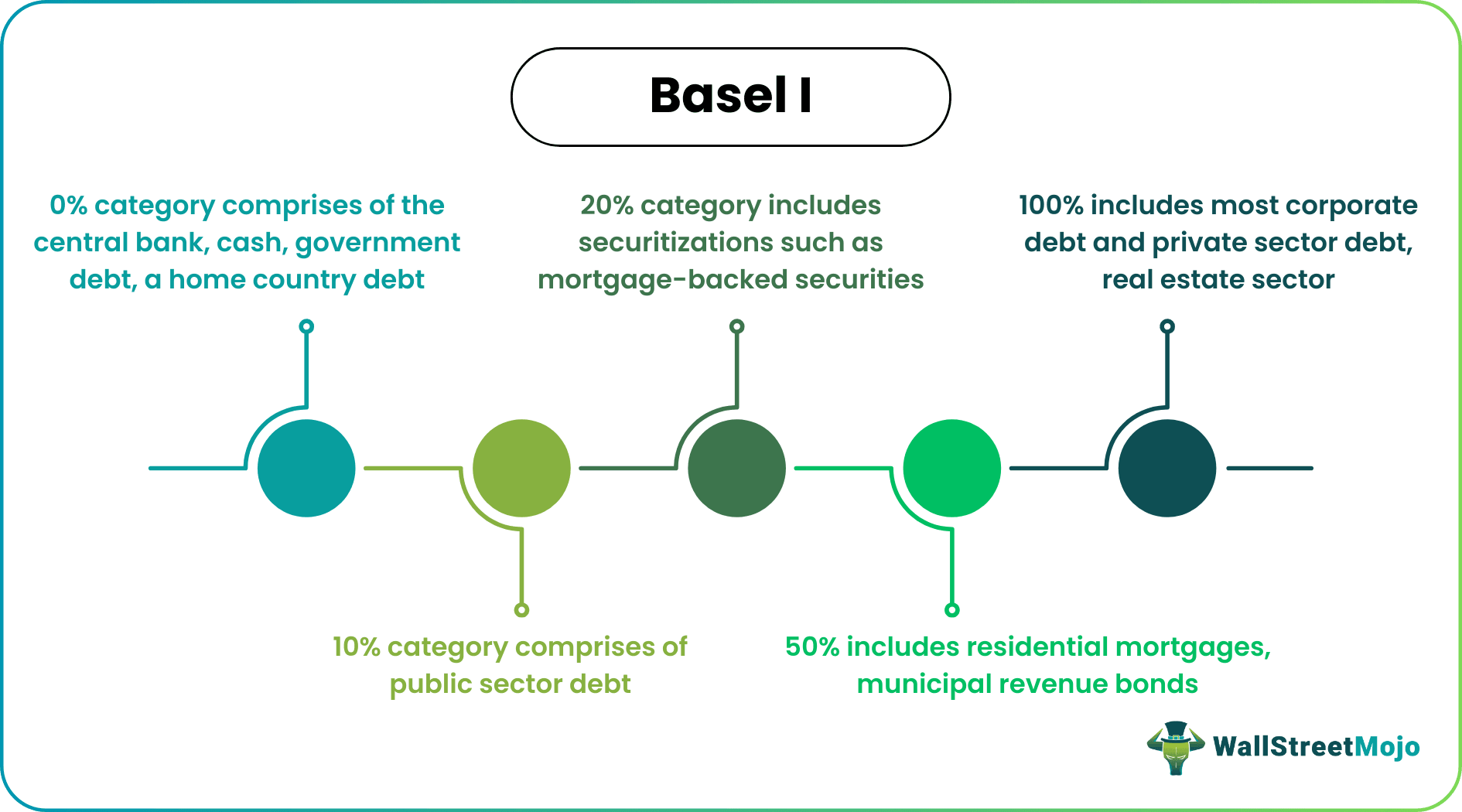

The capital requirements of the banks depend on asset classification, which is one of the most vital parameters comprising the risk-weighing system of the accord. The Basel I pillars classify a bank’s assets into five categories based on risk in the form of a percentage, that is, 0%, 10%, 20%, 50%, and 100%. The nature of the debtor decides the category where bank assets are to be categorized. Some common examples are as follows: –

- 0% category comprises the central bank, cash, government debt, a home country debt like treasuries, and any OECD government debt;

- 10% category comprises public sector debt;

- 20% category includes securitizations such as mortgage-backed securities with the highest AAA ratings;

- 50% includes residential mortgages, municipal revenue bonds;

- 100% includes most corporate debt and private sector debt, real estate sector, non-OECD bank debt where maturity term is over a year.

The bank needs to maintain capital (Tier 1 and Tier 2) equal to 8% of the risk-weighted assets under which category it falls. For example, if a bank has risk-weighted assets of over $200 million, it must maintain a capital of about $16 million.

Examples

Let us consider the following examples to understand the Basel I norms thoroughly:

Example 1

Let’s say a bank has a cash reserve of $200, $50 as a home mortgage, and $100 as loans given out to different companies. The risk-weighted assets as per the set norms will be as follows: –

=($200*0) +($50*0.2) +($100*1)

=0+10+100

= $110.

Therefore, according to Basel I, this bank has to maintain a minimum of 8% of $110 as a minimum capital (and at least 4% in tier 1 capital).

Example 2

Russia did not have an organized banking system before the central bank of the nation stripped the licenses of many banks out there based on the Basel Accords before 2017. The Basel Accords were introduced in the 1980s in Switzerland in the presence of central bankers and finance ministers. It has been upgraded to the Basel-III post the Great Recession period of 2008-09. This led to the bankruptcy of several private banks, keeping only the deserved ones to operate across the country.

Advantages & Disadvantages

Basel I managed to make banking services well-organized, well-managed, and well-regulated, thereby becoming a necessary regulation for the banks. However, it had some loopholes, which led to the modifications. These changes in guidelines and requirements resulted in the introduction of the next two provisions – Basel II and Basel III.

Let us have a quick look at the pros and cons of this Basel accord:

Benefits

- After the accord’s implementation, there has been a significant increase in capital adequacy ratios in internationally active banks. It removed a source of competitive inequality that arose from the differences in national capital requirements.

- It helped to strengthen the stability of the banking system internationally.

- It augmented the management of the nation’s capital.

- Compared to another set BASEL, it has a relatively more simple structure.

- It provides a benchmark for the assessment by the participants of the market since it is adopted worldwide.

Limitations

- It emphasizes more on book value rather than market value.

- The accord could not adequately assess the risks and effects of new financial instruments and risk mitigation techniques.

- Basel I is based on capital adequacy, which depends on credit risk, while all other risks such as market and operational risks are excluded from the analysis.

- It does not differentiate between the debtors of different credit ratings and quality while assessing credit risk.

Basel I vs. Basel II

In June 1999, the committee replaced the 1988 accord for a new capital adequacy framework. This led to the establishment of the revised capital framework in 2004 called Basel II that consists of three pillars mentioned as follows: –

- Minimum capital requirements

- Effective disclosure as a medium for strengthening market discipline and for sound banking practices.

- The internal assessment process and review of an institution’s capital adequacy.

The main difference between both the regulations is that Basel II incorporates the credit risk held by financial institutes to make out the regulatory capital ratios.

Frequently Asked Questions (FAQs)

Frequently Asked Questions

1. What is the Basel I regulation?

u003cpu003eFormed in Basel, Switzerland, Basel regulations aim to reduce credit risk and specify the minimal capital needs for financial organizations. Basel I is the name of a series of international banking laws governed by the Basel Committee on Bank Supervision (BCBS).u003c/pu003e

2. What are the pillars of Basel I regulatory framework?

u003cpu003eThree pillars of regulation now exist market discipline, supervisory scrutiny, and minimum capital requirements (Pillars 1 and 2). (Pillar 3).u003c/pu003e

3. What is the main purpose of Basel I?

u003cpu003eThe Committee’s efforts quickly shifted to focusing mostly on capital adequacy after establishing the groundwork for overseeing internationally active banks.u003c/pu003e

4. What countries follow Basel?

u003cpu003eThe only developed nations that were members up to 2009 were Belgium, Canada, France, Germany, Italy, Japan, Switzerland, the United Kingdom, and the United States.u003c/pu003e

Recommended Articles

This has been a guide to what is Basel I. We explain vs Basel II and capital requirements per the accord along with advantages, disadvantages, and examples. You may learn more about financing from the following articles –