Part of our Banking and Financial Institutions guide

What is Basel III?

Basel III is a regulatory framework, an extension of the Basel Accords, designed and agreed upon by the Basel Committee on Banking Supervision to strengthen the capital requirements of banks and mitigate risk. This is done by requiring the banks to hold more capital reserves against their assets, which would reduce the capacity of banks to get leverage.

The Basel III requirements clearly specify a certain level of capital adequacy, liquidity, and leverage. They conduct stress testing so that the risk of the banks and their customers are mitigated and the bank has an adequate capital reserve. After the 2008 financial crisis, the committee extended its member countries to 28 jurisdictions and 45 institutions.

- Basel III is a regulated structure made by the Basel Committee on Banking Supervision to strengthen the capital sufficiency of banks and annihilate their risks.

- The agreement’s mission is to hold greater security in reserve, and it strives to improve the banking regulatory framework drafted in the previous Basel agreements.

- Basel III has three requirements: requiring banks to maintain a minimum level of cap reserve, implementing leverage requirements, and additional capital requirements.

Basel III Explained

Basel III is a set of measures and norms that are internationally agreed upon on banking supervision curated by the Basel committee. Though initiated in the 1970’s it was redefined and extended to multiple other countries and institutions after the 2008 financial crisis.

The Basel Committee on Banking Supervision was established in 1974 to ensure financial stability by making stringent regulations on banking practices and finances. The committee comprised governors from central banks of ten different countries – headquartered in Basel, Switzerland.

The Basel committee initially consisted of the G10 members. Later in 2009, it expanded its membership to institutions from Brazil, Australia, India, Saudi Arabia, Russia, Japan, Italy, Mexico, Argentina, Canada, Belgium, Indonesia, Switzerland, South Africa, the United Kingdom, and the United States, all of which form and follow the Basel III standards.

Basel III is arguable a good step in strengthening the banking environment after the global financial crisis in 2008. The situation showed that bigger banks are eyeing rapid expansion without giving due weightage to riskier lending. The result was a pressing need for a stricter framework to regulate leverage, liquidity, and capital buffer within the sector.

It was introduced with revisions and strength to the principles of Basel II. The new framework prescribes higher capital adequacy for RWAs, capital conservation buffers, and countercyclical buffers for RWAs, thus strengthening the international banking system.

However, it has certain weaknesses that expose the sector to inefficiencies. It was widely accepted, and implementation was carried out across the globe. However, harmonization of banking regulations worldwide can also lead to deteriorating results as some countries already have better frameworks.

Objectives

Following the Basel III requirements gives institutions and jurisdictions better liquidity and leverage. However, there are objectives on a deeper level that we can understand through the discussion below.

Basel III introduced reforms that aimed to mitigate risk in the banking system. The objective behind the accord is to keep more security as a reserve before raising money. It aims to enhance the banking regulatory framework that was prescribed in the earlier Basel accords. It emphasized improving the resilience of banks by considering financial and risk management with stress testing in extreme situations. It ensures the strengthening of banks during times of liquidity crisis and financial distress.

Implementation

Implementation of the Basel III standards has evolved quite a few times since its inception in the 1970s. The changes come in light of the changing requirements of the banking sector and corresponding to the newer forms of doing business.

Basel III came into existence upon agreement by members of BCBS in November 2010. The implementation was scheduled from 2013 but suffered repeated extensions in the rollout. The first is scheduled for March 2019, while the second is due in January 2022.

In the United States, Basel III has been said to be applicable to all institutions with In the United States, Basel III has been said to apply to all institutions with assets over US$ 50 billion with differences in ratio requirements and calculations. In 2013, the Federal Reserve Board approved the U.S. version of the liquidity coverage ratio of the Basel III accord. The United States has also proposed the categorization of liquid assets in three levels with 0%, 20%, and 50% risk-weighting, with special importance given to the systematically important banks and financial institutions.

The scheduled imposition of capital requirements, leverage ratio, and liquidity requirements in the European context varied in time.

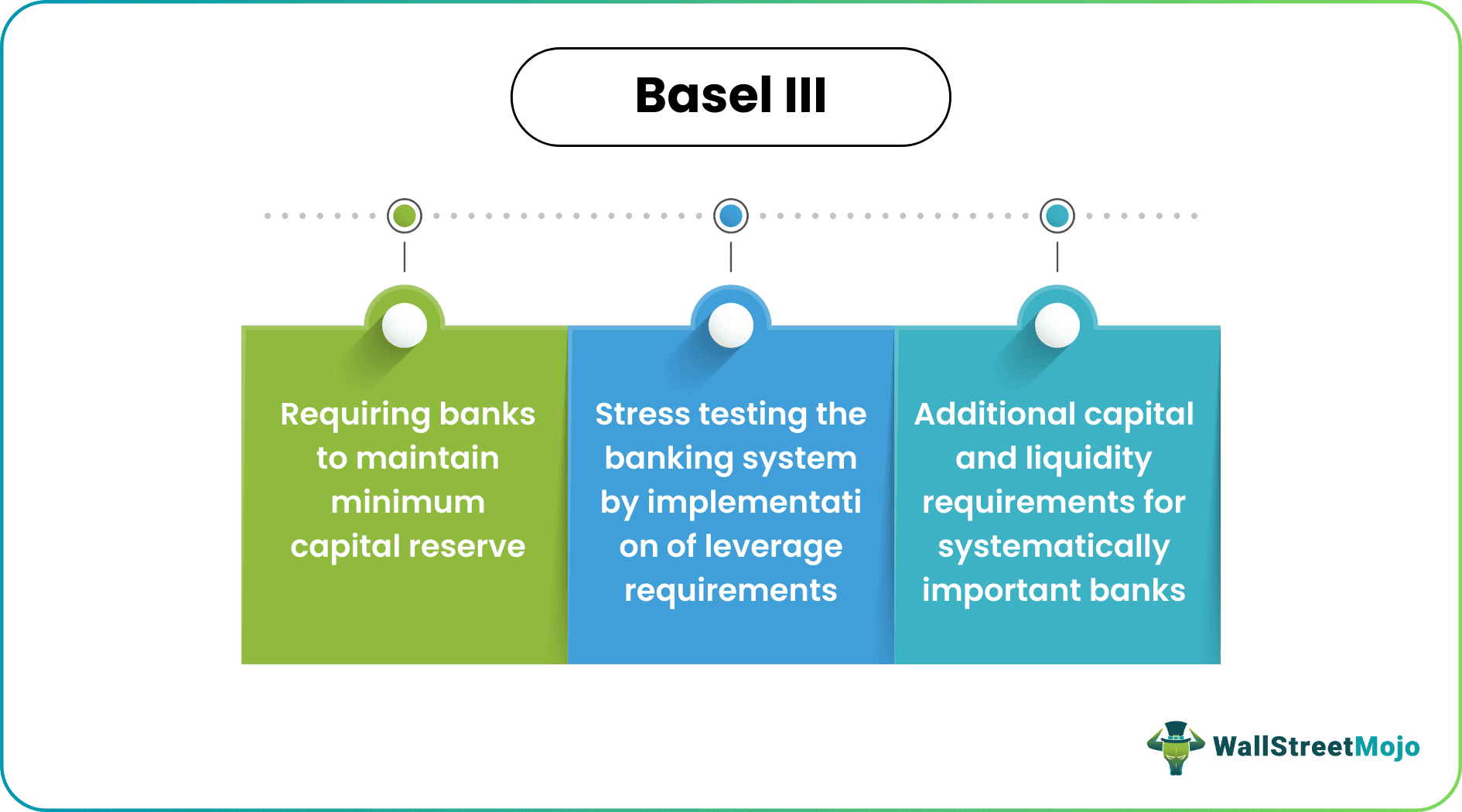

Pillars

The Basel III requirements are curated based on a set of principles or better referred to as the pillars of the concept. These will help us understand the importance of the committee and how these pillars help the governance of banking. Let us do so through the explanation below.

- Requiring banks to maintain the minimum capital reserve and an additional buffer layer in common equity.

- Stress testing the banking system by implementation of leverage requirements.

- Additional capital and liquidity requirements for systemically important banks.

Norms

The Basel III standards are set or framed around a set of norms that must be strictly adhered to by member jurisdictions and institutions. The number of members who follow these rules has expanded extensively post the financial crisis in 2008. Let us understand the norms in their evolved form through the discussion below.

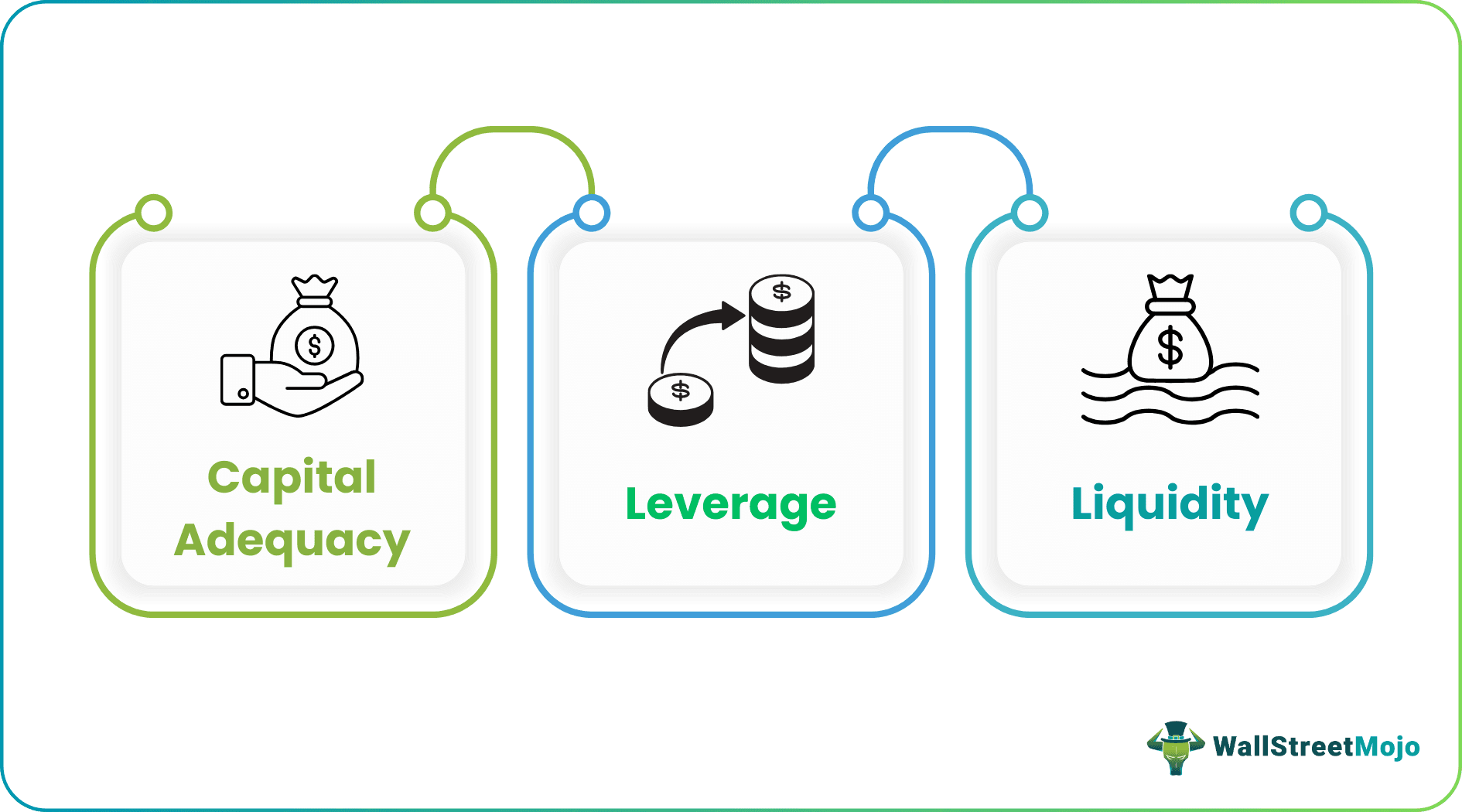

Capital Adequacy

- Capital reserve requirements increased to 7%, including the capital of 2.5% buffer against risk-weighted assets (RWAs). Additional legislation requires a countercyclical buffer of 0% to 2.5% of RWAs for CET1

- It requires common equity funding of 4.5% for risk-weighted assets. In Basel II, this requirement was 2%

- Minimum Tier 1 capital increased from 4% in Basel II to 6% in Basel III, comprising of 4.5% of CET1 and an additional 1.5% of AT1 (Additional Tier 1)

Leverage

- Banks must maintain a leverage ratio of at least 3%. That is, the Tier 1 Capital should be at least 3% or more of the total consolidated assets (incl. non-balance sheet items).

Liquidity

- Banks must hold high-quality liquid assets to cover total cash outflows over 30 days.

- Net Stable Funding Ratio requirement increased to over one-year.

Impact

The impact of adhering to Basel III requirements has been extensively discussed and followed by multiple organizations across the globe. Let us understand its impact on a macro level through the explanation below.

Stringent Basel II norms will certainly impact the ease of business that banks around the globe enjoy. The tightened requirements of the capital buffer, leverage, and liquidity will hit the profitability and margins of the banks. For example, a higher capital requirement of 7% introduced in Basel III will cut banks’ profits to some extent. In addition, the size of loan disbursements will be directly affected by the capital reserve requirement.

An OECD (Organization for Economic Cooperation and Development) study in 2011 showed that the effect of Basel III on GDP would be -0.05% to -0.015% annually in the medium-term. Another study showed that banks had to increase an estimated 15 basis points on their lending spreads to meet the requirements of the capital reserve rule.

Criticism

Despite the fact that the Basel III standards help banks and other institutions maintain enough capital and improve their liquidity and leverage, there have been factors that have attracted stiff criticism for the concept. Let us understand them through the points below.

- Capital reserve requirements will reduce competition in the banking sector as the barriers to entry increase. Critics argue that stringer norms will shield the sector in adverse ways.

- Leverage and capital adequacy requirements will also impact the efficiencies of bigger banks with consistent growths based on stable margins.

- The risk-weighting methodology is the same in Basel III to calculate RWAs as in Basel II. This might give importance to rating agencies that rate assets based on riskiness. Critics argue that such reliance on rating agencies is troublesome after the 2008 subprime crisis.

- Basel III’s criticism is not limited to its principles and regulations but also the implementation.

- Critics have repeatedly underscored the delay in implementation of the framework.

- The American Bankers Association criticized the regulation stating that Basel III would not only impact but cripple the smaller banks in the United States.

Frequently Asked Questions (FAQs)

Frequently Asked Questions

Has Basel 3 been put into practice?

u003cpu003eBasel III, finalized in December 2017, will go into effect on January 1, 2023.u003c/pu003e

What are the changes in Basel III?

u003cpu003eDue to the bank’s weighted assets, Basel III increased its minimum capital requirements from 2% in Basel Accord II to 4.5% in common equity.u003c/pu003e

What Basel III means for gold?

u003cpu003eSince Basel III is derived from Basel II and Basel I, it impacts the price of gold. In addition, it mitigates the risk of reserve capital since they prevent financial institutions from using derivatives and condemn them to own physical gold assets.u003c/pu003e

Recommended Articles

This has been a guide to what is Basel III. Here we explain Basel III’s objectives, implementation, pillars, and norms along with criticism and impact. You may learn more about financing from the following articles –