Part of our Banking and Financial Institutions guide

What Is Basel IV?

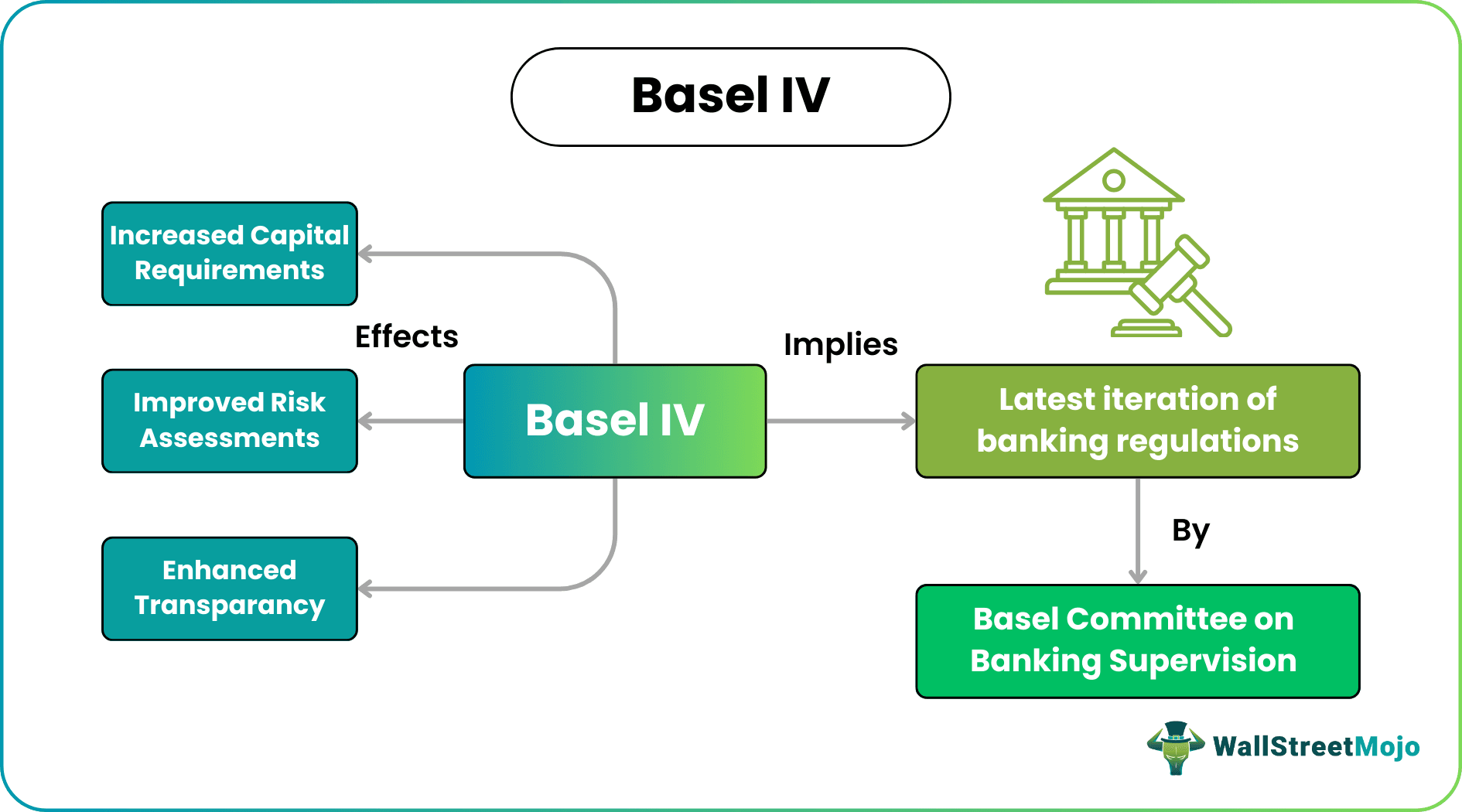

Basel IV is the iteration of global banking regulations developed by the Basel Committee on Banking Supervision (BCBS). It aims to enhance the stability and resilience of the banking sector by strengthening the regulatory framework and addressing the shortcomings identified in previous Basel accords.

Its importance lies in safeguarding the financial system against potential risks, ensuring that banks hold adequate capital to absorb losses, and enhancing transparency and comparability of their risk profiles. It restores trust in the banking sector, provides a level playing field for institutions worldwide, and mitigates the potential impact of financial crises by reinforcing global standards for banking regulation and supervision.

- Basel IV introduces stricter capital requirements, enhancing the resilience and stability of the banking sector by ensuring banks hold higher capital levels to absorb potential losses.

- The framework emphasizes improved risk assessment and management, promoting more accurate measurement and monitoring of credit, operational, and market risks. This enables banks to make better-informed decisions and mitigate vulnerabilities.

- Basel IV aims to enhance transparency and comparability of risk profiles, facilitating better assessments of banks’ financial health by regulators, investors, and market participants.

- Implementing Basel IV promotes global regulatory harmonization, reducing regulatory arbitrage and creating a level playing field for banks worldwide.

Basel IV Explained

Basel IV are regulations for operating banks developed by the Basel Committee on Banking Supervision (BCBS). It builds upon the previous Basel III framework and introduces several key changes and enhancements to strengthen the global banking system.

The Basel IV will improve risk management practices, increase capital requirements, and promote consistency in measuring and reporting banks’ risk exposures. One of the main objectives of Basel IV is to address the shortcomings and loopholes identified in the previous accords. It aims to achieve greater consistency, comparability, and transparency in banks’ risk measurement and capital adequacy assessment. Basel IV introduces more stringent rules for calculating risk-weighted assets, particularly in areas such as credit, operational, and market risks.

The framework also emphasizes leveraging technology and data to enhance risk management capabilities. It encourages banks to adopt more sophisticated models for risk assessment, stress testing, and liquidity management. Basel IV also introduces additional requirements for capital buffers, leverage ratios, and the measurement of funding stability.

Examples

Let us look at the examples to understand the concept better.

Example #1

As per an article by Reuters, Basel IV, or the “Basel endgame,” refers to the anticipated proposal from regulators in the United States to overhaul capital rules, expected to be unveiled in July 2023. The Basel Committee agreed upon these reforms in December 2017. However, the rules are not expected to be finalized until around mid-2024, as Federal Deposit Insurance Corporation Chairman Martin Gruenberg stated on June 22.

According to the article, regulators are contemplating the expansion of stricter capital rules to encompass banks with assets exceeding $100 billion. Federal Reserve Chair Jay Powell also conveyed a similar message to Congress, highlighting that most capital reforms would primarily apply to the largest firms. The proposed changes are part of ongoing efforts to enhance the stability and resilience of the banking sector.

Example #2

Consider that Basel IV regulations are in place. A major global bank, Bank X, has historically used lenient risk-weighting methodologies for its loan portfolio, resulting in lower capital requirements and potentially underestimating its risk exposure. Under Basel IV, stricter rules are implemented to accurately measure credit risk.

As a result, Bank X is required to reassess its loan portfolio using the new regulations. The revised risk-weighting methodologies reveal that certain loans were underestimated in terms of their riskiness. Consequently, Bank X must hold higher capital levels against these loans to ensure adequate risk coverage. By enforcing more rigorous risk assessment and capital requirements, Basel IV enhances the resilience of banks, reduces the probability of unexpected losses, and strengthens the overall stability of the financial system.

Effects

Let us look at the effects on the banking industry and the financial system:

- Increased capital requirements: Basel IV introduces stricter capital requirements for banks, particularly for risk-weighted assets. Banks must hold higher capital levels to cover potential losses, ensuring they have a stronger buffer against financial shocks. This increased capitalization enhances the overall stability and resilience of the banking sector.

- Improved risk assessment and management: The framework introduces more robust methodologies for measuring and managing risks, such as credit risk, operational risk, and market risk. Banks must adopt more sophisticated models and processes to assess and monitor risks accurately. This leads to a more comprehensive understanding of risks, enabling banks to make better-informed decisions and mitigate potential vulnerabilities.

- Global regulatory harmonization: It promotes greater harmonization of banking regulations across different jurisdictions. This alignment reduces regulatory arbitrage and creates a level playing field for banks worldwide.

- Enhanced transparency and comparability: It aims to improve the consistency and comparability of risk measurement and reporting across banks globally. This allows regulators, investors, and market participants to have a clearer view of banks’ risk profiles and enables better financial health assessments.

Basel IV And The Butterfly Effect

There is a connection regarding both concepts in terms of their potential impacts on the financial system. The butterfly effect, derived from chaos theory, suggests that a small change in one part of a system can have far-reaching and unpredictable consequences in another part of the system. In the context of Basel IV, implementing new regulations and changes in capital requirements could introduce subtle shifts in the behavior of individual banks or the financial industry as a whole. These seemingly minor adjustments can ripple through the system and create unintended effects.

Like, stricter capital requirements may lead banks to reassess their risk profiles and lending practices. This could result in changes in credit availability, interest rates, or the allocation of resources within the financial system. Such alterations in one part of the system can trigger a chain reaction, impacting other banks, borrowers, investors, and even broader economic conditions.

Also, the interconnectedness of global financial markets means that regulation changes can reverberate globally, affecting international banking institutions, cross-border transactions, and market dynamics. This highlights the potential for a small regulatory adjustment, such as those introduced by Basel IV, to have significant and unpredictable consequences throughout the financial ecosystem.

Basel IV vs Basel III

Let us look at some key differences between Basel IV and Basel III:

| Aspect | Basel IV | Basel III |

|---|---|---|

| Capitalization | Stricter capital requirements | Introduced minimum capital ratios |

| Risk-weighting | More stringent rules for risk-weighted assets | Less detailed and flexible risk-weighting methodologies |

| Credit risk | Enhanced assessment and modeling requirements | Introduced standardized approach and internal models |

| Operational risk | Increased emphasis on operational risk | Introduced separate standardized approach |

| Market risk | Revised framework for market risk | Introduced standardized and internal models |

| Liquidity | Additional requirements for liquidity buffers | Introduced liquidity coverage and net stable funding ratios |

| Technology and data | Emphasizes leveraging technology for risk management | Lesser focus on technological advancements |

Frequently Asked Questions (FAQs)

Frequently Asked Questions

1.How does Basel IV impact banks’ lending activities and profitability?

<p>Basel IV’s stricter capital requirements may increase banks’ capital costs. As a result, banks may become more cautious in extending credit, particularly to riskier borrowers. This cautious approach can potentially limit access to financing for certain individuals or businesses, affecting lending activities.</p>

2.Will Basel IV affect smaller banks differently from larger banks?

<p>Basel IV is designed to apply to banks of all sizes, including smaller institutions. However, the impact of Basel IV may vary depending on the scale and complexity of a bank’s operations. Smaller banks may face compliance costs and resource allocation challenges to meet the enhanced regulatory requirements.</p>

3.How does Basel IV address the shortcomings of previous Basel accords?

<p>Basel IV aims to improve the shortcomings identified in previous Basel accords, particularly Basel III. It addresses inconsistencies in risk measurement and capital requirements by introducing more stringent rules and enhanced risk assessment methodologies. The framework introduces robust frameworks for credit, operational, and market risks, ensuring a more comprehensive understanding of risks.</p>

Recommended Articles

This article has been a guide to what is Basel IV. Here, we compare it with Basel III, and explain its examples, effects, and relation with the butterfly effect. You may also find some useful articles here –