What is Personal Finance?

Personal finance comprises investment, budgeting, savings, risk allocation, mortgages, and personal banking. It is financial management pertaining to an individual or household. It focuses on individual financial objectives. Achieving financial goals requires some level of financial literacy—knowledge of tax laws, investment opportunities, interest rates, etc.

Financial growth at the individual level involves reducing debts, reducing credit card reliance, avoiding impulsive buys, and long-term planning. Everyone needs to save up for retirement and emergencies. In addition, individuals must possess knowledge of credit scores to maintain their creditworthiness.

- Personal finance deals with an individual or household’s income, spending, and savings.

- The five fundamental focus areas of personal finance are income, spending, savings, investing, and protection.

- Understanding a country’s tax system can help individuals save a lot of money. This requires proper tax planning. Tax avoidance is a legal method of saving money by paying fewer taxes—by claiming various tax deductions and credits.

Basics of Personal Finance Explained

Personal finance can be understood as the art of managing money. It deals with an individual’s or household’s earnings, savings, and expenses —based on needs and preferences. Individuals who plan their finances have a better shot at reaching their financial goals. Even with limited earnings, they can afford a decent standard of living and future financial security.

Everyone should possess basic finance know-how. But, in the end, finance boils down to personal discipline and control over unnecessary expenses. Further, everyone needs to learn the difference between needs and wants. Once individuals narrow down on a financial goal, they can start saving. In addition, they can invest in suitable opportunities and create multiple sources of income.

Foundation of Personal Finance

The following areas act as the foundation for personal finance:

- Income: It refers to the cash inflow or earnings made by individuals or families—salary, wages, commission, bonus, pension, rent, profit, dividends, etc.

- Spending: It refers to incurred monthly expenses—rent, travel, utilities, mortgage payments, taxes, and leisure.

- Savings: It refers to money that is left after expenses and investments.

- Investing: For financial growth, individuals invest in profitable assets—securities, bonds, mutual funds, and fixed deposits. Investments require proper analysis of potential risks and returns.

- Protection: Insurance offers financial security to individuals—health insurance, motor insurance, life insurance, product insurance, etc.

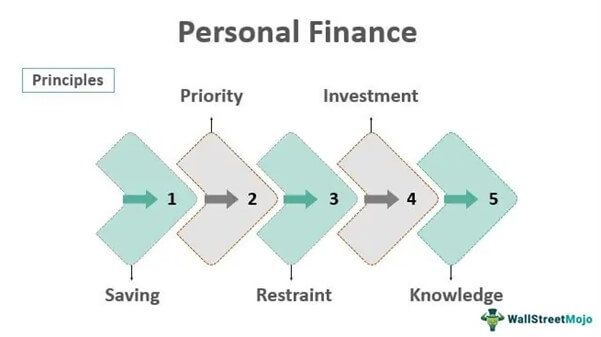

Principles

The principles of personal finance are as follows.

- Prioritization: Decide your priorities before spending—segregate all the unavoidable expenses from the ones that can wait.

- Assessment: Before investing, analyze the costs and benefits of each financial product, investment opportunity, or business idea.

- Restraint: The 30-day savings rule is highly recommended. Before spending your money on something you want but don’t need, stop and think for 30 days. This financial technique protects individuals from impulse buying.

- Knowledge: Develop an interest in financial management—better knowledge of finance and markets lead to better decision-making.

Types

Financial planning at the individual level comprises the following:

- Budgeting

- Savings

- Investment

- Banking

- Mortgages

- Loans

- Retirement Planning

- Estate Planning

- Tax Planning

- Insurance

Personal Finance Tips

Following are some strategies for efficient personal finance management:

- Allocate a personal finance budget. Further, break it down into—necessary expenses, savings, and investments.

- Credit cards may seem bliss, but they can very well end up being a curse. Use them only for emergencies.

- Keep track of your credit score—a poor credit report will result in expensive or no loans for the future. Timely payment of installments is highly recommended.

- Individuals must restrict their borrowings through mortgages and credit cards.

- Always save something for emergencies—a reserve of three to six months of earnings should be set apart.

- Tax planning should be done in advance. Tax avoidance is a legal method of saving money by paying fewer taxes—by claiming various tax deductions and credits.

- Everyone needs long-term financial planning for the future. Pension plans

- and long-term investment plans provide constant and periodic returns post-retirement.

Example

Let us consider a fictional example to understand the practical application of personal finance.

Arthur and Brendan work in XYZ Bank as Probation Officers. In a month, they earn $4000 each. Both are married and have a child. While Arthur is keen on personal finance, Brendan does not plan his finances. Thus, for a family of 3, their spendings are as follows:

| Expenses | Arthur ($) | Brendan ($) |

|---|---|---|

| House Rent | 2000 | 1900 |

| Utilities | 600 | 780 |

| Transportation | 150 | 120 |

| Child’s Education | 600 | 600 |

| Debt Repayment | 100 | 200 |

| Miscellaneous | 250 | 500 |

| Investment | 100 | – |

| Savings | 200 | – |

| Total | 4000 | 4100 |

Note: Miscellaneous expenses include outings, leisure, and entertainment.

From the above table, it is evident that Brendan spent $100 more than he’s earning using his credit card. This is on top of the $200 debt repayment for past borrowings. Also, he does not have any savings or investments. Clearly, Brendan had no financial planning.

On the contrary, Arthur plans, budgets, and tracks his finances. As a result, he invests $100 and saves $200 every month. The differences between planned and unplanned finances add up over time. By comparing current expenses and prospective investments, individuals can determine the feasibility of engaging in alternative asset ventures. For instance, understanding precise gold stats is invaluable for anyone considering diversifying with precious metals. With gold prices soaring to record figures anticipated in 2024, such insights are crucial for making informed investment decisions.

Frequently Asked Questions (FAQs)

1. What are the main sources of personal finance?

Following are the various ways through which an individual or household generates income:

• Salary/Business/Professional income;

• Rental income from leasing or renting premises;

• Interest received on savings or fixed deposit account;

• Dividends and interests received on other investments like securities, bonds, and debentures;

• Accumulated savings;

• Proceeds from mortgage loans;

• Borrowing from peers and family members.

2. What is the 30-day rule?

The rule applies to purchases that an individual wants but does not really need. So, the 30-day rule recommends waiting 30 days before spending. After 30 days of pondering, if the individual still fancies, they can go ahead with the purchase. This financial management technique protects individuals from impulse buying.

3. How to plan your finance?

Personal finance planning involves the following steps:

• Making a budget of income and expenses;

• Deciding a financial goal;

• Listing out the inevitable expenses:

• Limiting unnecessary spending;

• Investing in suitable opportunities;

• Retirement planning:

• Insurance Saving for emergencies.

Recommended Articles

This has been a guide to What is Personal Finance & its Meaning. Here we discuss personal finance budget, planning, examples types, principles, and strategies. You can learn more about it from the following articles –