What is the Pension Plan?

A pension plan is a retirement plan where the employer makes a guaranteed payment to the employee once they retire. Employees receive a specified monthly income post-retirement from their employer’s investment. However, traditional and defined benefit plans have become exceedingly rare and have been replaced by plans that are less heavy on the employer such as 401K plans.

A retirement pension plan differs from a 401k plan in that the employer, rather than the employee, contributes to the retirement funds. However, these plans vary depending on the employer and the employee’s tenure with the company. The pension amount will typically be a percentage of the employee’s regular salary during their employment with the company.

- A pension plan is a retirement plan in which the employer will guarantee to pay a specified amount to the employee upon retirement.

- The employer will contribute on the employee’s behalf and manage the investments. However, in some cases, an employee may choose to contribute toward the retirement plan.

- The future pension income depends on how long the employee has worked for the company and how much they earned.

- Pension and 401k plans differ in several ways, such as contributions, payments, and portfolio management.

How does Pension Plan Work?

Pension plans are benefits, meaning an employer will guarantee the employee a payment once the employee retires. The payments will be consistent, giving the employee a reliable income stream during retirement. These plans are not the same as 401k, although many people confuse them with one another.

Below are the common aspects of pension plans and how they work to give the employee a retirement income:

Employer-Funded

These plans are employer-funded, meaning the organization will contribute to a retirement portfolio for the employee. It also means that the employee will not contribute to the fund at their own expense. However, the employee can also contribute to the fund in some cases.

The Fund

With the contributions on the employee’s behalf, the company will invest in a portfolio containing various securities. The fund’s primary goal is to grow the investments over time and give the company the money needed to make payments to the employee during retirement.

Until recently, pension plan calculators were used to calculate investments which were almost exclusively invested in safer stocks and bonds. Now the funds will be distributed to an assortment of diverse investments, including:

- Stocks

- Bonds

- Derivatives

- Real Estate

- Commodities

- Infrastructure

According to research from the National Association of State Retirement Administrators (NASRA), the average pension fund will distribute 47.1% of the fund in public equities (stocks), followed by 24% in fixed income (bonds), 19% in alternative investments, 7% in real estate, and 2% in cash and cash equivalents.

Payment Amount

In most cases, the size of the pension payout depends on the length of time the employee worked for the company and how much they earned during their tenure.

Every plan will have different terms and conditions that apply to them based on what the employer has set in place. However, the pension plan calculator to determine a payout amount will work like this:

(Years Employed * Accrual Rate * Average Salary)

In this case, the Years Employed would be the years the employee worked for a particular employer.

The Accrual Rate will be the amount of interest applied, typically a part of the employee’s retirement benefits with their employer. It is a significant factor as it will be multiplied by the total years of employment and the average salary to determine the pension payout. The higher the accrual rate the employee receives, the greater their retirement plan will be.

The Average Salary calculation considers the average salary of the last few years of employment. Depending on the employee’s location, it could be the final three or five years of work.

For example, an employee worked at a company for 25 years. A standard accrual rate is around 2%, and their average salary is $100,000.

In this case, the pension payout amount would be 25 * 2% * 100,000 = $50,000 a year.

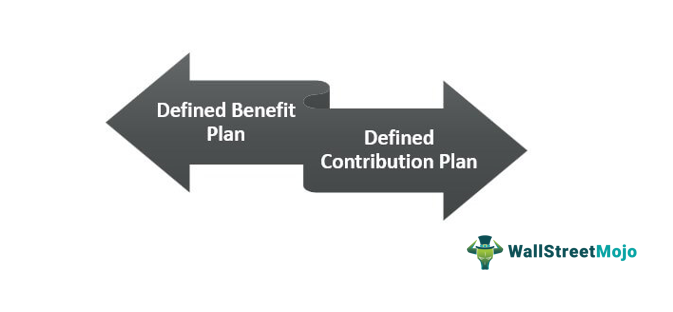

Types

Let us understand the different types of retirement pension plans through the detailed explanation below.

#1 – Defined Benefit Plan

- The defined benefit plan will guarantee a set amount of funds upon retirement.

- The employer will make additions to the fund on the employee’s behalf. However, in many cases, the employee can also make contributions.

- Many factors affect payouts, such as years of employment and how much the employee earned.

- The employer will manage the investments in most plans.

- Payouts will typically last for life after retirement.

#2 – Defined Contribution Plan

- With the defined contribution plan, payouts vary with several factors, such as how much the employee contributes and how well the investments perform.

- The employee will be making contributions to these types of plans. However, in some cases, the employer can match it.

- The employee will control the investments with a defined contribution plan.

- Payouts will last as long as the money in the fund lasts.

Benefits

In the modern day, these plans have been replaced by modern forms of retirement plan calculators such as 401k plans to reduce the pressure and responsibilities from the employer. Regardless of the shift, there are still huge benefits for both the employer and employees. Let us understand them through the discussion below.

#1 – Assured Payments

One of the most significant benefits of these plans is the guaranteed payouts once the employee retires. Unlike other retirement plans, these plans do not rely on the performance of any financial market. Instead, these plans will base their payment on employment-related factors.

#2 – Employer Managed

The employer typically manages these plans. It works in most people’s favor as not everyone is a financial expert. With other retirement plans, the employee will have to manage their investments.

#3 – Safety

The employer may have to step in and contribute if the fund does not perform well enough. If they go bankrupt and cannot make the payments, an agency like the Pension Benefit Guaranty Corporation (PBGC) will often step in.

Pension Plan vs. 401k

Pension plans and 401k plans are two types of retirement plans that often get mistaken. While the former is a defined benefit plan without employer matches, the latter is a defined contribution plan with employer matches.

However, there are a few differences in their fundamentals and implications. Let us understand the differences between retirement pension plan and 401k plans through the comparison below.

#1 – Contributions

One of the main differences between both plans is the contributions made. The employer makes the contributions with pension plans, whereas with 401k plans, the employee contributes, and the employer can match it.

#2 – Payments

With pension plans, the employee guarantees payments after retirement. In 401k plans, the payout will only last as long as funds are there.

#3 – Control

Employers will have control over the investments before retirement with pension plans. It is different from 401k plans, where the employee will have control over assets.

Frequently Asked Questions (FAQs)

1. What is a cash balance pension plan?

A cash balance pension plan is a type of defined benefit plan where the employer contributes a fixed percentage of an employee’s salary plus interest credits. The plan maintains individual accounts for each employee, similar to a defined contribution plan, and provides a lump sum benefit at retirement based on the accumulated balance.

2. Do pension plans have beneficiaries?

Yes, pension plans typically have beneficiaries. Beneficiaries are individuals designated by the plan participant to receive pension benefits in the event of the participant’s death. Depending on the plan’s rules, beneficiaries can be spouses, children, or other dependents.

3. What are the risks associated with a pension plan?

Risks associated with pension plans include investment risk, where the performance of pension plan investments may not meet expected returns, leading to funding shortfalls. There is also longevity risk, as people are living longer, increasing the duration of pension payments. Changes in interest rates, economic conditions, and employer financial stability can also impact pension plan funding and benefits. Regulatory and legal changes can introduce uncertainties and obligations for plan sponsors.

Recommended Articles

This has been a guide to a what is a Pension Plan. Here we discuss how it works, its types, and benefits, and compared it with a 401K plan. You may learn more about financing from the following articles –