Part of our Market Regulations guide

What Is Rule 144A?

Rule 144A is a regulation framed by the Securities Exchange Commission (SEC) under the Securities Act of 1933, which facilitates the buyers of private securities to resell their securities to Qualified Institutional Buyers (QIBs). It was implemented to encourage foreign companies to sell securities in the United States capital markets.

This rule, introduced in 2012, allows QIBs to trade these investments among themselves, which leads to higher liquidity of the involved securities. In addition, QIBs can purchase these private securities and resell them without registering with the SEC. However, analysts and economists have criticized this rule for the non-scrutiny from SEC and the attraction of foreign institutions to enter the U.S. securities market.

- Rule 144A is a regulation under the Securities Act which allows Qualified Institutional Buyers (QIBs) to purchase private securities and trade among themselves.

- QIBs don’t need to register themselves with the Securities Exchange Commission (SEC) to carry out such trades.

- The SEC does not scrutinize the trades of Rule 144A bonds and securities unless the trade volume exceeds 5,000 shares or $50,000 in value.

- It has drawn criticism from experts for the non-transparency and leniency of the SEC, which might attract fraudulent activities from foreign investors on U.S. soil.

Rule 144A Explained

Rule 144A facilitates the buying and reselling private securities among QIBs by altering the restrictions without interference from the SEC. This regulation has attracted divided opinions among analysts and experts in the market.

A group of experts believes it will attract more foreign investment and improve the economy, as well-informed investors require limited protection and information compared to an individual or retail investor.

On the flip side, a few believe that even though foreign investments are suitable for the economy’s growth, they need to be scrutinized by the SEC to ensure no fraudulent activities are brewed due to the lack of scrutiny. Moreover, clarity and transparency in defining what establishes a QIB are required to ensure no unethical or corrupt activities are carried out. Therefore, rule 144A restrictions need to be increased, in their opinion.

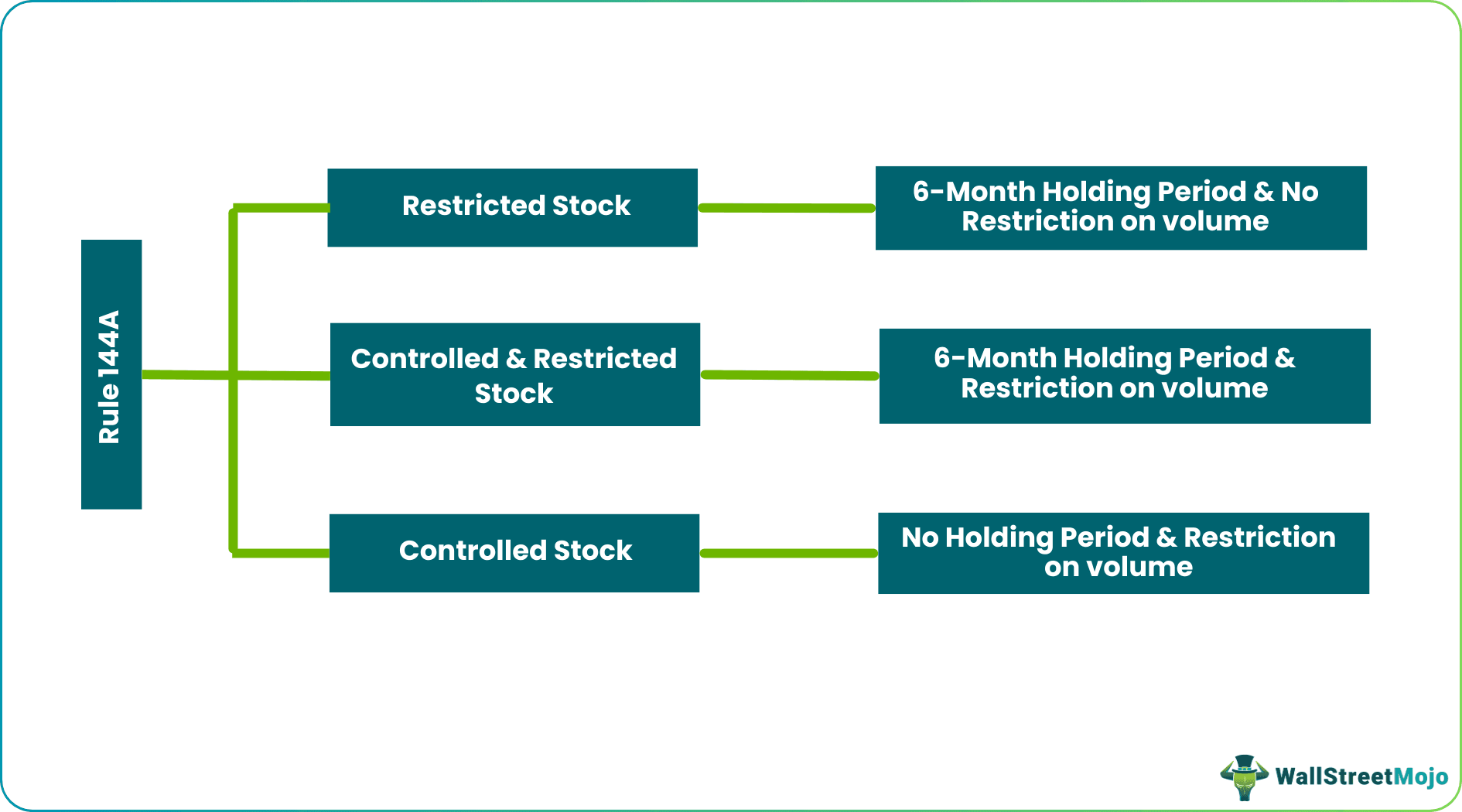

This rule eased the holding period from the initial two-year holding period window to a minimum six-month for reporting companies and a one year-year minimum period for issuers. The period commences on the same day of the purchase, and payment in full is made for the securities.

The resale of rule 144A securities has to be facilitated by a registered firm or a brokerage complying with the affiliate sales rules. A minimal commission is charged to carry out the sale where neither the seller nor the broker can involve themselves in postulating the security’s sales.

Since there is no intervention or scrutiny from the SEC on such trades, the market’s liquidity is increased, and the sales flow is much more efficient. However, if a sale of more than 5,000 shares or the value of the sale exceeds $50,000 in any quarter of the year, the sale has to be reported & disclosed to the SEC on Form 144.

Any sale through an affiliated entity need not be filed or reported to the SEC.

Requirements

- Rule 144A disclosure requirements allow the resell of securities if they have adhered to the following criteria:

- The buyer is a Qualified Institutional Buyer (QIB)

- The buyer can request the required information from the original issuer of the security

- Security is of a different class than what is traded on the National Securities Exchange

- The seller has taken active steps to establish that the buyer is aware of the seller’s reliability on rule 144A restrictions to resell the security.

Examples

The technicalities and regulatory rules might be slightly tricky to understand. Therefore, let us take the help of the practical examples below to understand the concept better:

Example #1

Velocity Corporation has 10,000,000 outstanding shares of common stock. In the last four weeks, their average weekly trades were 125,000 shares.

Inertia Group Inc., an affiliated entity, decided to sell 125,000 as the trading volume exceeded 1% (100,000) of the outstanding volume of shares.

Even though the number of shares exceeded 5,000, Inertia Group, an affiliated entity, did not file it with the SEC on Form 144 stating the specifics of the sale. The broker carried out the transaction, where neither Inertia Group nor the broker was involved in securing a buyer. The broker might sell the securities in the broker’s transaction if the conditions are met.

Example #2

Sarepta Therapeutics, Inc., a market leader in precision genetic medicine in September 2022 announced the pricing of $980 million of the principal amount to unsecured notes, which will mature in September 2027 unless repurchased, converted, or redeemed. The sale will be carried out through QIBs only.

An affiliate with a board of directors member at Sarepta had also agreed to buy $20 million in a private placement.

Rule 144A vs Reg S

Rule 144A and Regulation S (or Reg S) are regulations through which securities are purchased and resold among QIBs. However, there are a handful of differences in the practical application and a few fundamentals. Let us understand them through the table below:

| Basis | Rule 144A | Reg S |

|---|---|---|

| Basic Function | QIBs can trade rule 144A bonds without registration and scrutiny from the SEC. | Regulation S is a type of bond open for offers and trades outside the United States of America for U.S. and non-U.S. Qualified Institutional Buyers. |

| Clearance systems | Usually cleared through the Depository Trust and Clearance Corporation (DTCC) | Usually cleared through Euroclear and Clearstream |

| Identification Numbers | The committee on Uniform Securities Identification Procedures number or CUSIP number is issued and applied with an ISIN code for clearing. | International Securities Identification Number or ISIN Code is generally accepted for clearance. |

Frequently Asked Questions (FAQs)

Which statement describes trading rule of 144A issues?

Rule 144A issues are sold in blocks only to QIBs (Minimum $500,000). The trading from QIBs to QIBs happens through the online facility called PORTAL. As a result, the trading activity is minimal compared to the trading carried out in publicly traded securities.

What is the difference between rule 144 and rule 144A?

Rule 144A restricts resales only to QIBs and applies only to specific securities. Rule 144, on the other hand, states resale is possible only to adherence to the holding period and volume and is open to the public.

What is a qualified institutional buyer rule 144A?

Insurance companies and state funds such as pension, investment, and trust funds hold and invest at least $1000,000,000 in non-affiliated securities. Therefore, according to the rule, any dealer/broker who holds and invests the same amount also qualifies as a qualified institutional buyer (QIB).

Who can buy Rule 144A securities?

The SEC only permits QIBs who own and invest $100 million in non-affiliate securities. However, investment companies or insurance companies with assets under management equal to or above $100 million can trade these controlled or restricted securities.

Recommended Articles

This has been a guide to what is Rule 144A & its meaning. We explain it in detail with its requirements, examples, and comparison with Reg S. You may learn more from the following articles –