What Is A Credit Agreement?

A credit agreement is a legal document that outlines the terms between a lender and a borrower. Both parties are legally bound to fulfill their end of the loan agreement. It acts as proof when a borrower defaults; the loan agreement enables lenders to seize collateralized assets or property.

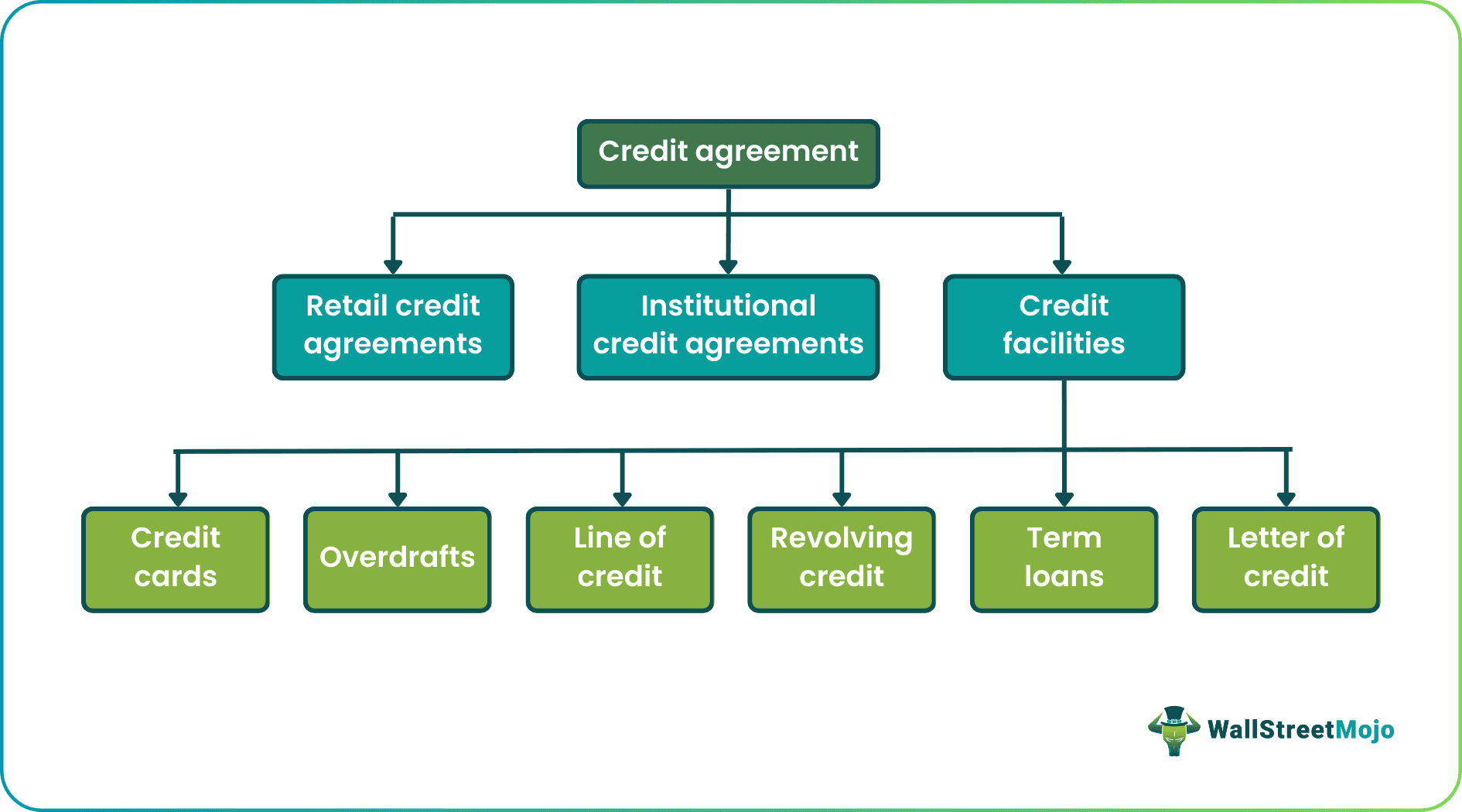

The loan agreement is mentioned in the borrower’s credit report. It outlines past loans, current mortgages, interest rates, the amount paid, the number of installments, and the amount left. In addition, the agreement is used to secure different types of loans—credit cards, home loans, car loans, mortgages, or business loans.

- Credit agreements are legally binding; it outlines loan terms and conditions. However, the legal document requires signatures from both parties to be considered valid.

- The lender could charge a fixed interest rate or a floating interest rate. In addition, lenders demand collateral to mitigate credit risks. Some lenders lend without collateral, but such loans come with a higher interest. Loan agreements elaborate on these conditions in detail.

- Consumer loan agreements are regulated by the Financial Services and Markets Act 2000 (FSMA 2000) and the Consumer Credit Act 1974 (CCA 1974).

Credit Agreement Explained

A credit agreement is a legal document that outlines the terms between a lender and a borrower. Both parties are legally bound to fulfill their end of the loan agreement. It acts as proof when a borrower defaults; the loan agreement enables lenders to seize collateralized assets or property.

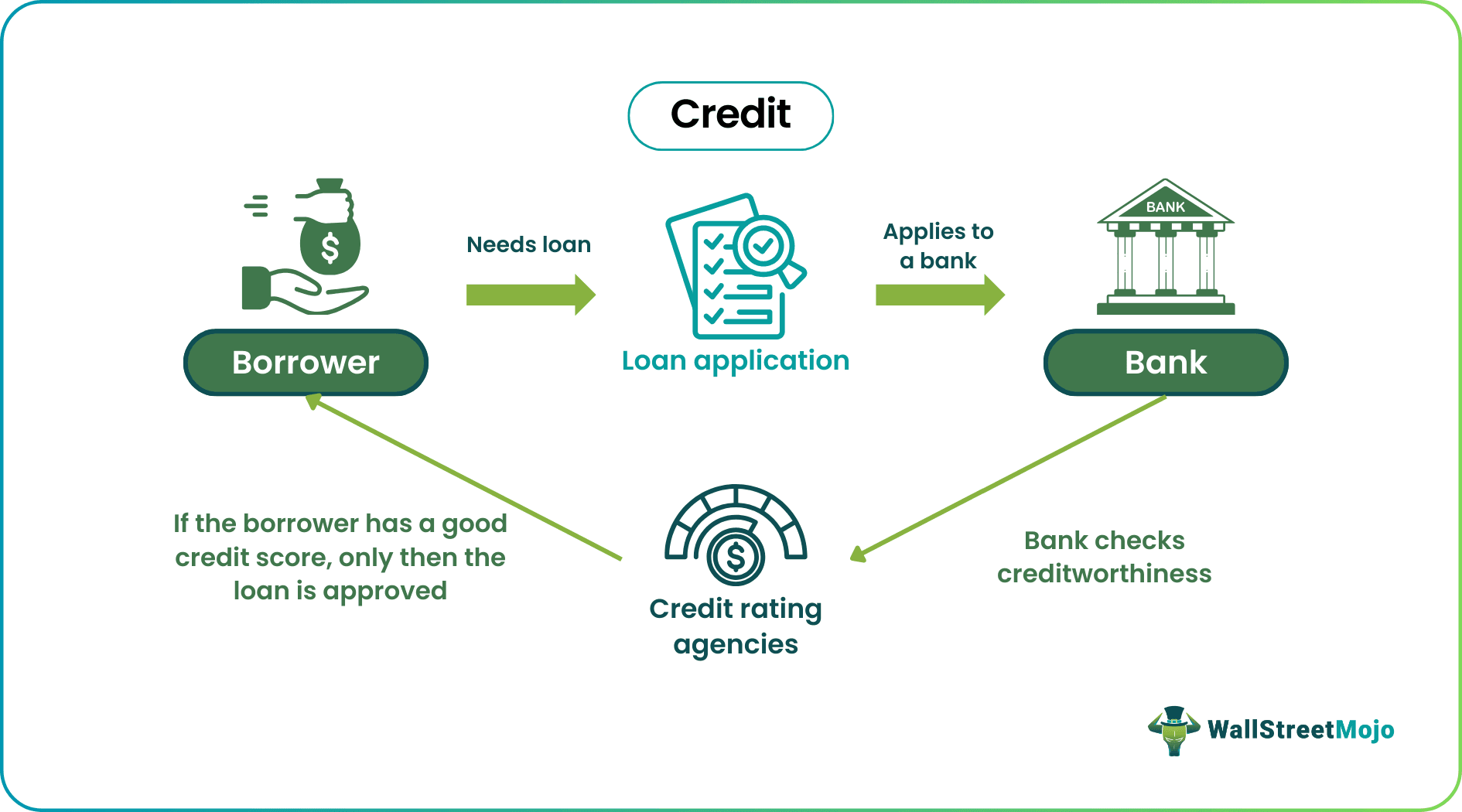

Before venturing further, let us first define credit. Credit refers to a lender agreeing to lend funds to a borrower. In return, lenders charge an interest rate, a fixed interest rate, or a floating interest rate.

It is important to note that most lenders demand collateral to mitigate credit risks. Some lenders lend without collateral, but such loans come with a higher interest. Using credit, customers fulfill their needs without paying the full amount. This could be a product, house, or education fee.

If borrowers default on their loans, their credit scores, and credit history get tarnished. This means the borrower would not be able to secure future loans. Lenders face massive risks. Therefore, lenders screen loan applicants thoroughly before sanctioning funds.

Lenders decide based on an applicant’s repayment ability and credit history. In addition, lenders use creditworthiness to prepare borrowers’ credit rating models. Also, individuals, firms, or organizations cannot start large-scale projects without bank credit.

When a business or an individual borrows money from a bank, they initiate a step-by-step written document—the loan agreement. This document records, especially, the terms and conditions. Signatures are required from both parties. Loan agreements are further classified into credit cards, overdrafts, business loans, and personal loans.

Consumer loan agreements are regulated by the Financial Services and Markets Act 2000 (FSMA 2000) and the Consumer Credit Act 1974 (CCA 1974). However, not all loans are regulated. For example, gas, water, electricity, personal mortgages, credit union borrowings, and employer-borrowed money are regulated loans.

Line of Credit (LOC) refers to an extended credit limit individuals receive for their creditworthiness. This amount is available for personal and business purposes at any time. The LOC is a revolving loan agreement that allows the party to borrow till they reach the credit limit. Then, the credit limit is extended once again if the borrower repays the loan.

The loan agreement also outlines the repayment schedule. If a borrower decides to repay too early, a penalty is imposed. Typically, lenders are not eager to close loan obligations too soon—they will lose earnings from interest. Therefore, prepayment is a hefty penalty, discouraging more borrowers from repaying too early.

At the other end of the spectrum, if a borrower is behind on payment, the lender sends an arrear notice along with the U.S. Financial Conduct Authority (FCA) arrears information sheet.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Examples

Let us look at some credit agreement examples to understand their practical application.

Example #1

Damon wishes to use a credit card. He visits the local bank immediately and applies for a credit card. He submits the relevant documents.

The bank explains legalities and documentation. Along with the benefits, the bank manager also explains the liabilities associated with a credit card. Before receiving the credit card, Damon gets a credit card agreement from the bank. The agreement contains detailed information pertaining to interest rates, penalties, charges, benefits, and usage. Damon signs the document.

The credit card agreement is a legal document. It is an agreement between Damon (borrower) and the lender (bank). Credit cards are considered a form of revolving loan.

Example #2

In November 2022, the International Money Express made relevant amendments to its credit agreement. It intends to replace LIBOR with the secured overnight financing rate set by the Federal Reserve Bank of New York.

It is commonly addressed as a money remittance services company. Recently, the platform decided to become more flexible with limited payment options. The company has tried various loan structures–revolving loans, SOFR, and index adjustments.

Sample

Now, let us look at a credit agreement sample:

(Source)

The main components of a loan agreement are annual interest rates, payment terms, associated fees, late payment consequences, penalties, loan duration, and standard terms and conditions.

Amended And Restated Credit Agreement

Loan agreements list amendments made over a period. The agreement outlines loan terms, covenants, warranties, definitions, and miscellaneous. Every single change is accounted for. The document becomes legally binding only when both parties agree and sign it.

Credit Agreement vs Promissory Note

Now, let us look at credit agreement vs promissory note comparisons to distinguish between the two.

- A credit agreement outlines the terms and conditions of a loan in detail. In contrast, a promissory note is a document legalizing a promise to pay a certain amount of money when produced at a particular time.

- The loan agreement is a lengthy and complex document. A promissory note, in contrast, is simple and succinct.

- The loan agreement has three sections—interpretation, credit type, and transaction details. On the contrary, promissory notes have four sections—loan amount, interest rate, maturity date, and late payment penalty.

- A letter of credit (loan agreement) expires only when both parties have fulfilled their obligations, and in most cases, the borrower receives a NOC from the lender. In contrast, a promissory note becomes invalid after a specified period.

- Loan agreements are less risky for the lender. However, a borrower can default on payments despite the promise to pay. Promissory notes. Therefore, they are risky for the lender.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

1. What is the purpose of a credit agreement?

The purpose of a loan agreement is as follows:

– It protects the rights of the lender and the borrower.

– It ensures clarity and transparency in the process.

– It is written documentation that acts as proof of credit.

2. Does credit agreement affect the credit score?

Yes, it does; lenders share loan agreements with credit rating agencies. But if a borrower has a reliable record in the past, a single default or delayed payment does not make a significant difference.

3. Can a credit agreement be withdrawn?

If a borrower decides to repay too early, a penalty is imposed. Typically, lenders are not eager to close loan obligations too soon—they will lose earnings from interest. Therefore, prepayment is a hefty penalty, discouraging more borrowers from repaying too early.

Recommended Articles

This article has been a guide to what is Credit Agreement. We explain its sample, examples, restated agreement, and comparison with the promissory note. You can learn more about it from the following articles –