Part of our Credit Concepts guide

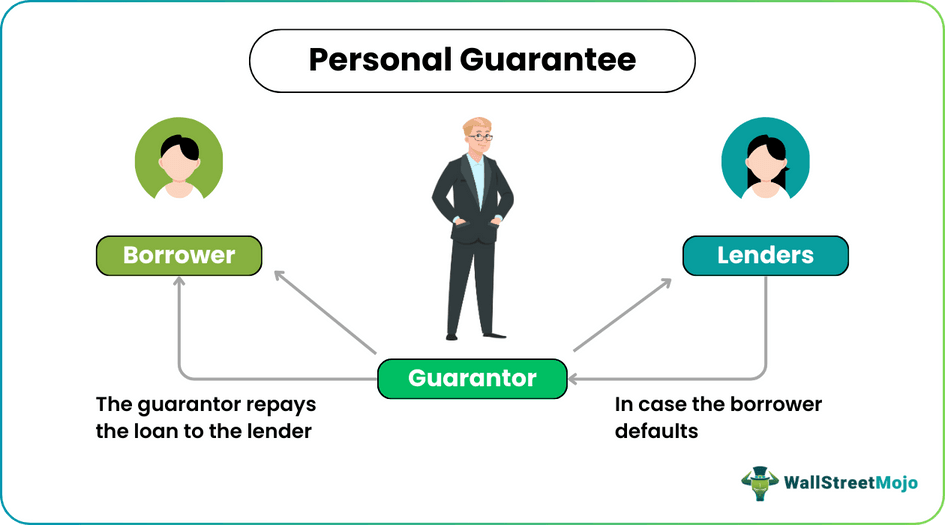

What Is A Personal Guarantee?

A personal guarantee is like an agreement between three parties – lender, borrower, and guarantor, whereby the guarantor agrees or promises, and has legal binding attached to him, to repay the lender and honor the loan agreement in case of default made by the borrower, irrespective of the fact that the person giving guarantee is or is not attached to the business for which the loan is taken.

Thus it is an agreement having a legal binding that if the borrower does not fulfill his obligations towards liabilities/dues, this guarantee shall be invoked, and the personal guarantor is liable to honor the agreement. It may be either limited or unlimited. Further, personal assets may also be attached for repayment if required.

- A personal Guarantee is a commitment given by someone to uphold the terms of the contract, accept and fulfill their obligations, and pay their fair share of any liabilities.

- In order to provide security for the amount being lent, lenders request a personal guarantee. Additionally, it gives them the assurance and comfort that the borrower will make the loan payment in full and on schedule.

- A personal guarantee increases a small business’s chances of obtaining a loan that might not have been otherwise possible.

How Does A Personal Guarantee Work?

In simple words, the personal guarantee on business loan means providing security.

- When talking about a personal guarantee, it refers to the promise made by a person to honor the agreement and accept and make the payment of the liability and obligations as agreed in the agreement. The guarantor’s assets may or may not be attached; the same may be decided when getting into the arrangement.

- The personal guarantor makes this legal promise to the lender to support the borrower to help him get the loan or debt.

- In the event of default by the borrower, the lender may claim the personal guarantor to make good the default.

Clause

Given below are the clauses of personal guarantee for loan.

- The lender should have tried all ways to recover the debt from the borrower first. Only then can he go to a personal guarantor.

- It’s a conditional promise, i.e., only if a borrower defaults, the lender may resort to recovering the dues from the borrower.

- There should be a balance of debt/liability which is pending repayment.

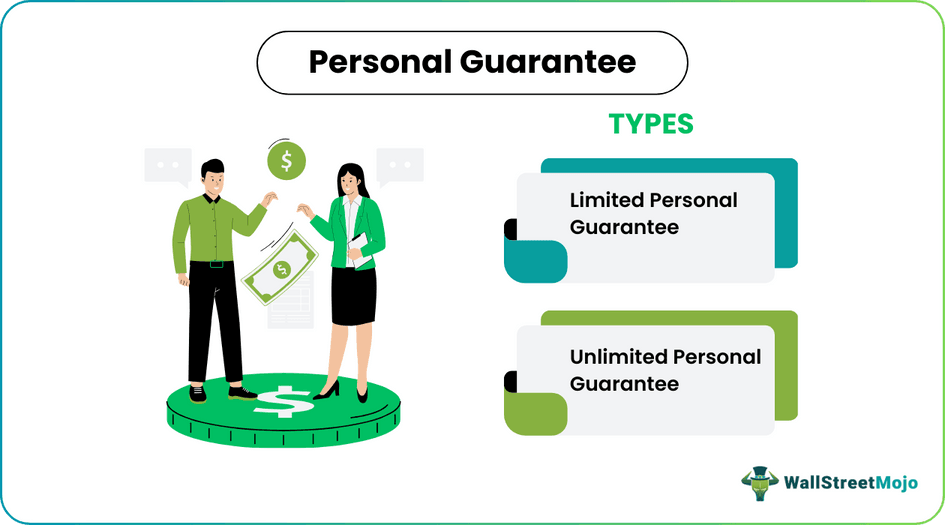

Forms

Let us look at some personal guarantee on business loan.

#1 – Limited Guarantee

- In an agreement with multiple owners/partners, each of them shall have a fixed percentage of holding in the business.

- Accordingly, each guarantor shall be obligated to honor only to the extent of such a fixed amount of liability in case the business defaults.

- Going deeper, a limited guarantee can be either (i) several guarantees or (ii) joint and several guarantees.

- Several guarantees mean that the obligation to repay the balance debt is restricted strictly to the extent mentioned in the loan agreement.

- A joint and several guarantees mean several guarantees (as explained above) but extended with the responsibility of fully repaying balance debt if an owner/partner does not pay up their required portion.

#2 – Unlimited Guarantee

As the title suggests, offering an unlimited personal guarantee means that the guarantor is fully responsible for making the repayment dues in case of default by the borrower, whether or not the borrower owes a guarantee of 100% repayment.

Thus, the above are the different types of personal guarantee for loan.

Reasons

The reasons for personal guarantee clause are given below:

- The main reason lenders ask for a personal guarantee is to ensure security to the amount being lent. Further, it also gives them an added assurance and comfort that the borrower shall pay the loan amount duly on time.

- It helps them make sure that the borrowers are committed to making the repayments and shall not take any undue advantage or utilize the loan amount in any unwanted and unnecessary ways.

- For the borrower, a personal guarantee clause may help businesses fetch loans that may not have been possible earlier or get a bigger loan amount sanctioned.

- This will assure the lender that the money shall be repaid in case of defaults and that his money is secured.

Example

Let us assume Joe needs funds to buy a car. He approached ABC Bank for a car loan. The bank agreed to give him the loan provided he has a guarantor against the loan. Thus, Joe requested his uncle Rick to become the guarantor. Rick agreed and ABC Bank approved Joe’s car loan. In this case, Rick acts as a personal guarantor for Joe’s loan.

Risks

- The biggest risk entails that once the same gets invoked, the guarantor are liable to fulfill the arrangement as there is a legal binding attached to it and make good the debt.

- It may be possible that the guarantor may have to use all the savings, kept aside for children, retirement, emergencies, etc., and pay the dues. They may have to use the assets to pay up in case of high loan amounts.

- In high-risk scenarios, bankruptcy is also possible.

- So before signing for any personal guarantee, it’s’ always safe to read and understand every term and liability.

Advantages

- The credit history and credit rating of the guarantor are considered along with the borrowers’ credit history and rating.

- Improved/better credit backing/availability for a loan.

- Improves chances of fetching a loan for a small business which may not have been otherwise possible.

- Gives an assurance to the lender that the loan shall be repaid.

Disadvantages

- If the business does not grow or fails to earn the required rate of return, and loan default, the personal guarantor may be required to help make the loan payments.

- Personal assets may get attached and utilized for repayment purposes.

- Credit rating may be affected when a personal guarantee agreement is invoked and required to pay.

Personal Guarantee Vs Collateral

A personal guarantee agreement is a promise from the guarantor to the lender to repay the loan if the borrower fails to do so, whereas a collateral is when an asset is used to secure a loan.

There is a third party in the former, whereas there is no third party in the latter.

The borrower does not have to pledge any asset for the former, whereas the borrower has to pledge an asset for the latter.

Frequently Asked Questions (FAQs)

What occurs when a personal guarantee is given?

If your business, a friend, or a family member fails on a loan, a personal guarantee enables the lender to pursue your personal assets.

Are personal guarantees upheld in court?

Without consideration, a personal guarantee is not enforceable. In actuality, a contract requires consideration to be upholdable. One kind of contract is a personal guarantee. A contract is a binding commitment.

What is the impact of a personal guarantee on creditworthiness?

Personal guarantees don’t directly affect your credit history, score, or business credit until you have financial difficulties.

Recommended Articles

This has been a guide to personal guarantee & its definition. Here we discuss the purpose of such guarantees, features, and types along with reasons, risks, advantages, and disadvantages. You can learn more about from the following articles –