What Is Credit Creation?

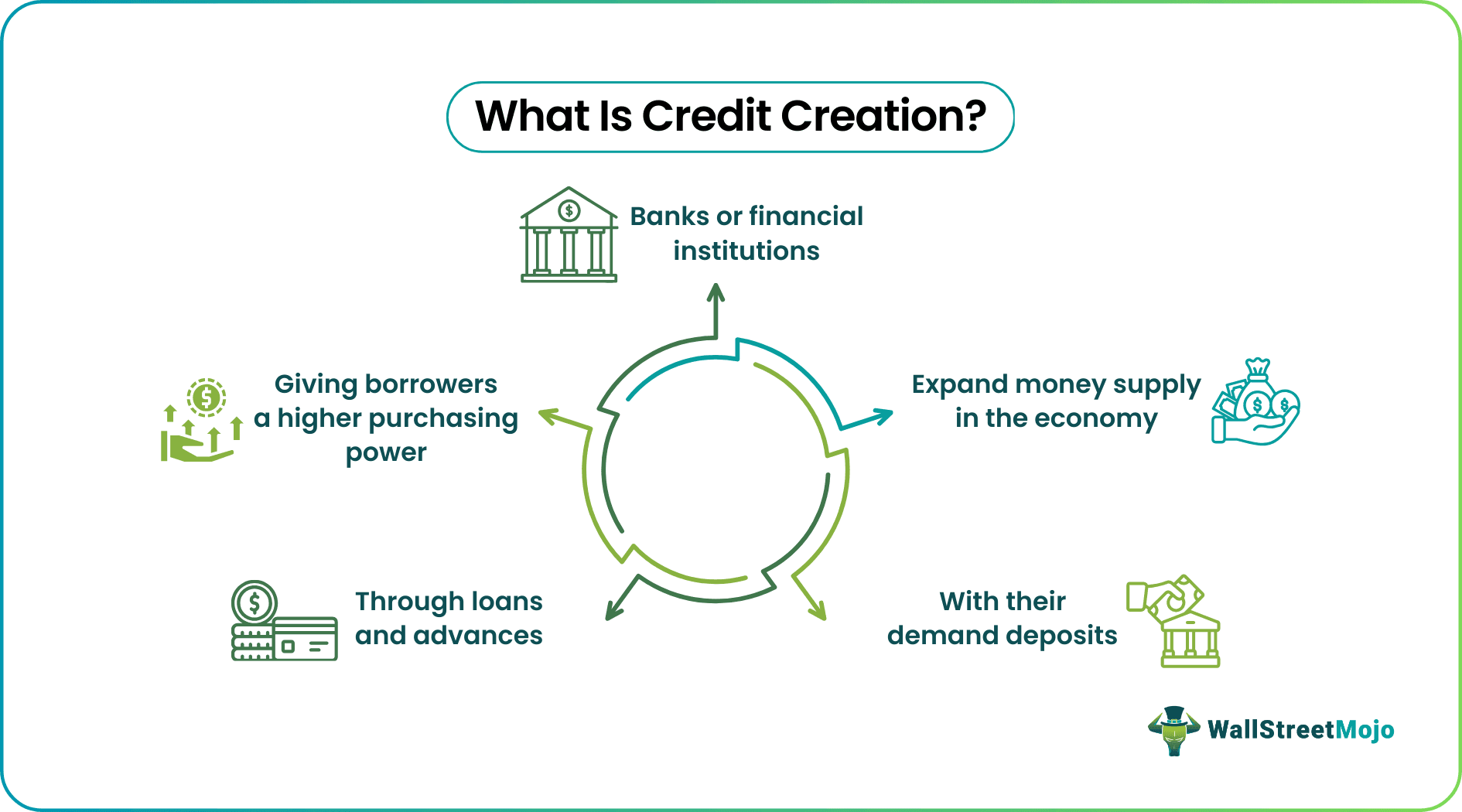

Credit creation refers to expanding the availability of money through the advancement of loans and credit by banks and financial institutions. These institutions use their demand deposits to provide loans to their customers, giving borrowers higher purchasing power and competitive interest rates.

In the process of credit creation, banks keep some share of their deposits as minimum reserves to meet the demand of their depositors. Thus, banks lend out the excess reserves for loans and investment purposes, and the interest earned becomes income for the banks. Therefore, the factors that drive the credit creation process are liquidity and profitability of the banks.

- Credit creation expands the availability of money in an economy through commercial banks and the country’s other financial institutions.

- A country’s central bank regulates credit creation by ensuring the maintenance of adequate reserves within the baking system and uses quantitative measures to control credit.

- The cash reserve ratio (CRR) defines legal reserves that banks shall maintain as a part of demand deposits while advancing loans and credit of the excess reserves. Additionally, the maintenance of reserves allows commercial banks to meet the cash withdrawal demands of their customers.

Credit Creation Process Explained

Financial institutions and systems of a country undertake the credit creation process for its economy. Additionally, the central bank regulates the commercial banks operating within the country in the credit creation process.

Demand deposits are those deposits with the banks that customers may withdraw without prior notice or lengthy waiting periods. Thus, these demand deposits are of two types – savings and current. Simultaneously, demand deposits with the banks assist them in advancing loans and credit to a wider public for economic activities such as consumption and investment purposes. This process of generating credit via demand deposits allows consumers, businesses, and governments to purchase, invest, and pay later in the future.

Simultaneously, , in the process of credit creation by commercial bank and central bank, every loan from the bank creates an equal amount of demand deposit in the bank. Therefore, facilitating credit in the economy shall expand bank deposits. So it is because a loan shall be credited to the borrower’s bank account, thereby creating an equivalent bank deposit.

Liquidity and profitability are two required methods of credit creation that lubricate and oil the banks’ ability to generate credit. Firstly, the banks must maintain certain reserves from their total demand deposits to pay for the cash demands of their depositors.

Secondly, the profitability of banks makes the credit cycle sustainable as it ensures banks are in a healthy position. At the same time, it indicates that banks are generating higher revenues from their interest earnings than what they are paying their customers on their demand deposits.

However, an important precondition for credit creation theory by commercial banks is that even when there is a demand for cash deposits, only a small section of the depositors would withdraw as they also maintain time deposits. Thus, the bank assumes not all its depositors would turn up at the same time at once to withdraw their deposits.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Formula

Let us try to understand and analyse the formula of credit creation by commercial bank and central banks, as give below:

Total Credit Creation = Initial deposits x 1/r (Equation 1)

where,

- ‘r’ = the cash reserve ratio (CRR) or legal reserve ratio (LRR)

Thus, the formula explains credit creation by commercial banks through the multiplier effect. Commercial banks must maintain legal or cash reserve ratios per the Central Bank’s guidelines. At the same time, excess deposits are available to the banks for loans and advances.

The money multiplier means the ratio by which the remaining deposits will increase or generate credit as a multiple of the initial deposits. Thus, the function of the money multiplier is the inverse of LRR or CRR. These reserves are maintained for emergencies when a bank faces poor financial conditions is important.

- Credit Multiplier Coefficient or Money Multiplier = 1/r (Equation 2)

Therefore, from equations (1) and (2), it can be concluded that the smaller the legal reserve ratio for commercial banks, the greater the money multiplier effect and credit creation. In contrast, a higher CRR or LRR will reduce the money multiplier effect and decrease the credit creation capability of commercial banks. For example, banks cannot create credit when the legal or cash reserve ratio is 100%.

How To Calculate?

For instance, an individual deposits $10,000 with a bank, and the legal reserve ratio that the bank shall maintain is 15%. Thus, the calculation for credit creation will be,

- Total Credit Creation = Initial deposits x 1/r

- Credit Multiplier/ Money Multiplier coefficient = 1/r

Here, ‘r’ = 15%

Money Multiplier Coefficient = 1/15% = 1/0.15 = 6.66

Total Credit Creation = $10,000 x 6.66 = $66,600

Thus, the bank will provide advances and loans to its customers worth $66,600. As a result, when the bank lends $66,600 to a borrower, he might take this amount and deposit it in another bank. As a result, this amount of $66,600 will become demand deposits for the next bank and is liable to LRR charges again.

Example

Let us comprehensively understand the credit creation meaning with an example of the calculation below,

| Banks | Initial Deposit | CRR or LRR | Remaining Deposits | Credit Creation | |

| Rick | The U.S Bank | $ 10,000 | 20% | $ 8,000 | $ 8,000 |

| Morty | California Bank | $ 8,000 | 20% | $ 6,400 | $ 6,400 |

| Sam | Chicago Bank | $ 6,400 | 20% | $ 5,120 | $ 5,120 |

| Raven | NYC Bank | $ 5,120 | 20% | $ 4,096 | $ 4,096 |

| Total | $23,616 |

Let us assume that four people at random borrow from one another from a bank and deposit the amount in their respective banks post borrowing. So, firstly Rick opens a bank account in the U.S Bank and deposits $10,000, and let us assume the LRR or CRR is 20%. Thus, post deducting the reserve ratio, the banks go ahead with lending the remaining deposit of $8,000.

Next, Morty borrows from the U.S Bank and deposits $8,000 in his checking account in California Bank. However, the California Bank deducts the 20% CRR from the initial deposit, i.e., $8,000. As a result, they advance the remaining $6,400 for loans to other customers as credit.

Similarly, when Sam deposits the borrowed amount from California Bank into her checking account in Chicago Bank, which will also deduct 20% and provide $5,120 for credit advances.

This credit creation cycle and money multiplier effect continue until the initial deposit is close to or equal to the CRR. Thus, in this example, an initial deposit worth $10,000 with a 20% CRR can create additional deposits worth $40,000.

Thus, in the above credit creation process, the total deposits made were worth $50,000. Therefore, the credit multiplier here is five, i.e., the inverse of CRR (20%), and the credit creation, i.e., $40,000, is five times the initial excess reserves, i.e., $8,000.

Advantages

The advantages of credit creation for an economy are similar to money being available to people as a medium of exchange. Thus, these include,

- Enable efficient monetary policy

- Stabilize the economy along with a mandatory reserve system

- Mitigates inflation

- Makes credit available to poorer sections of society, leading to inclusive growth.

- Wider access to consumer goods and investment opportunities.

Limitations

The credit creation theory has some limitations, which may limit credit creation due to various macroeconomic factors,

- The inverse relationship between CRR and the credit multiplier. Thus, a very high CRR will limit credit creation by commercial banks.

- Central banks’ role as lender of last resort and their responsibility to maintain inflation and ensure economic growth simultaneously poses certain restrictions on commercial banks. Additionally, central banks use quantitative measures to control credit and money supply.

- Situations like natural calamities or pandemics severely limit the credit-generating capacity of the banks. It is because people are not willing to take loans.

- Deposits form the basis for credit creation by central bank and commercial banks. Thus, a bank with a low base of deposits will generate less credit.

- People who do not have potential security as collateral cannot avail of credit.

It is essential to understand the advantages and limitations of such economic and financial concepts so that they can be implemented in a logical and production manner to achieve the objective.

Credit Creation Vs Credit Control

Both the above concepts are closely related to banking and economics, and they play a very crucial role in influencing the financial health of an economy as a whole. Let us understand the differences between them.

- The credit creation by central bank refers to the process of creating monetary flow in the economy through lending whereas the latter refers to the measures taken by central banks to influence the cost and credit availability.

- The former is implemented with the aim of increasing the money creation and circulation whereas the latter is control inflation, and promote economic growth and economic stability.

- The former is essentially related to the lending and borrowing and the latter is related to various macroeconomic objective.

Thus, at explained above both are widely used by the central bank to regulate money supply and create a stable economic condition. However it is important for the banks and financial institutions to be able to achieve a proper balance in the entire process. For this purpose, there is a requirement of continuous monitoring with the help of various economic indicators and take useful and informed decisions.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

1.What are the types of credit creation?

The process of generating credit in an economy takes place at two levels, one at the level of a single bank and another within the entire banking system. One bank creates deposits and clear checks as an individual unit. While in the country’s banking system, lending by one bank to a borrower becomes the demand deposit for another bank. Thus, both these types facilitate credit creation in the economy.

2.What are the assumptions of credit creation?

The most basic assumption for generating credit and loans in the economy is that banks assume not all their customers will demand cash or withdraw their deposits altogether. Thus, it can maintain legal reserves and facilitate loans and advances from the excess reserves.

3.What are the importance of credit creation?

Generating credit in an economy is as important as the function of money in an economy. As money plays multiple roles, similarly, generating credit allows an economy to achieve growth and development through more consumption, increasing demand, greater investment, and thus an increase in employment and economic activities.

Recommended Articles

This article is a guide to what is Credit Creation. We explain its limitations along with formula, advantages, example and differences with credit control. You can also go through our recommended articles on corporate finance –