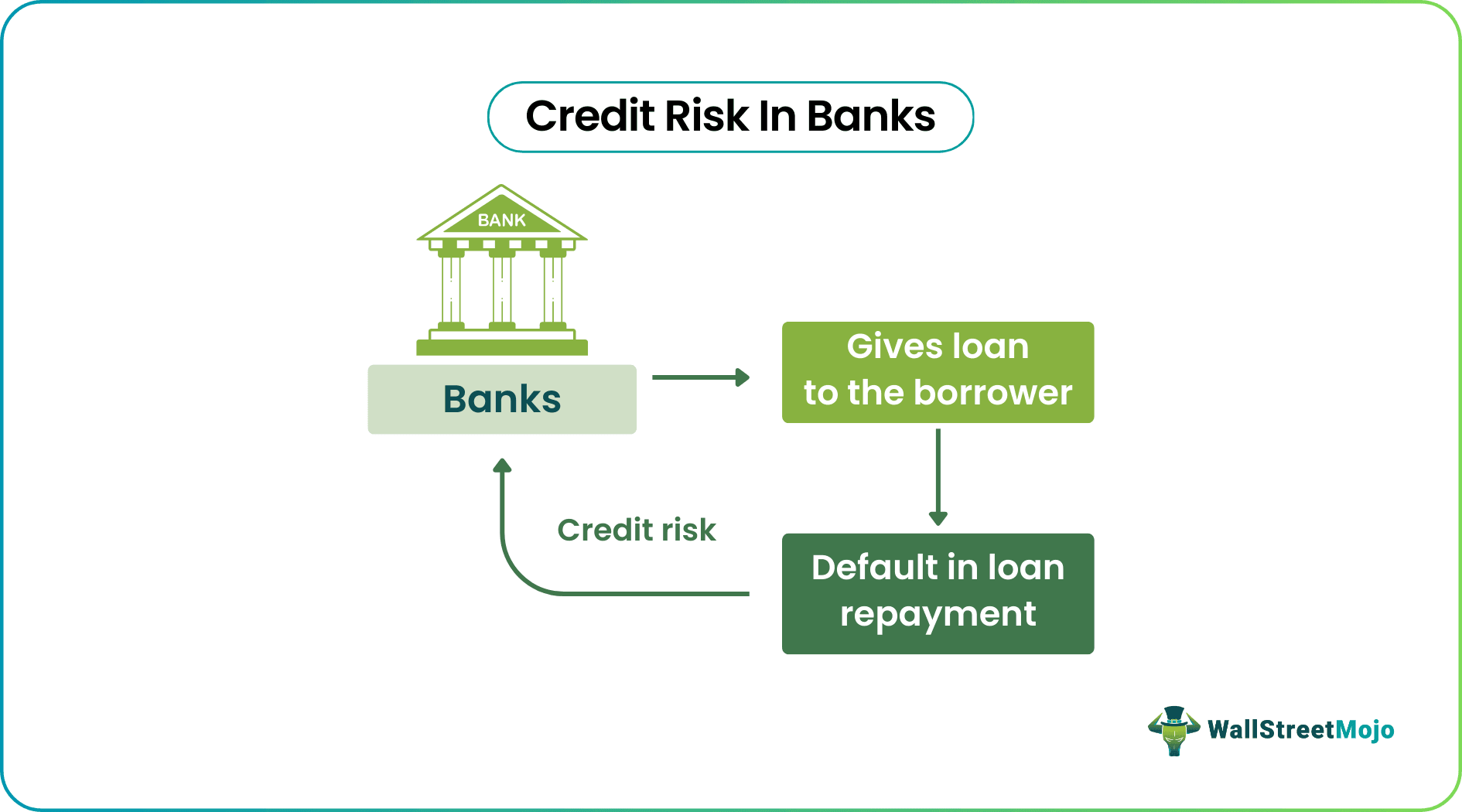

What Is Credit Risk In Banks?

Credit risk refers to the risk of default or non-payment, or non-adherence to contractual obligations by a borrower. Banks face credit risks from financial instruments such as acceptances, interbank transactions, trade financing, foreign exchange transactions, futures, swaps, bonds, options, settlement of transactions, and others.

Banks’ revenue comes primarily from interest on loans; accordingly, loans form a major source of credit risk. As of May 2019, credit card losses in the USA outpaced other forms of individual loans. There has been a huge spike in lending to riskier borrowers, resulting in larger bank charge offs.

- Credit risk in banks is the possibility that a borrower may fail to meet debt obligations, resulting in default or a breach of contract.

- Various financial instruments expose banks to credit risks, including acceptances, interbank transactions, trade finance, foreign currency transactions, futures, swaps, bonds, options, and transaction settlement.

- Credit card losses in the USA exceeded those from other types of personal loans by May 2019, reflecting a trend driven by increased lending to higher-risk borrowers. This has led to more substantial bank charge-offs due to the elevated credit risk associated with these loans.

Credit Risk In Banks Explained

Credit risk is the situation in which there is a risk that banks will not be able to recover the amount they have given to borrowers. This risk arises due to reasons like fall or loss of income of the borrower, change in market conditions, loan given out to borrowers without proper assessment of the borrower’s creditworthiness or history, sudden rise in interest rates, etc.

Credit risk management for banks are inherent to the lending function. They cannot be avoided wholly; however, their impact can be minimized with proper evaluation and controls. Banks are more prone to incur higher risks due to their high lending functions. It is important that they identify the causes of major credit problems and implement a sound risk management system to maximize their returns while minimizing the risks.

Thus, credit risk management in banking sector will remain as long as banks continue to extend loan, issue credit cards, provide any type of guarantee against loans or engage in any other activity related to credit functions.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Types

The credit risk situations that banks usually face can be of various types, as given below:

- Default Risk – This type of risk involves the situation where the borrower fails to make the repayment of principle or interest on loan or any kind of debt instrument, as per the terms and conditions of the contract. Default can be due to the fall in credit repayment capacity of the individual or external disturbances like change in market conditions or economic system.

- Concentration Risk – Banks might heavily invest in a single industry, geographic area or a borrower. Thus concentration of portfolio is very risky because if there are any adverse conditions in that sector, region or the individual borrower, the loan may not be repaid. This will affect the credit quality of banks in a negative way.

- Counterparty Risk – Banks often engage in transactions with other parties or financial institutions for regarding derivative contracts, interbank lending or any kind or trade financing. During such cases also the parties may fail to honor the contract and may default on the repayment.

- Sovereign Risk – Some banks purchase government bonds. They may also have exposure to foreign governments. Those governments may default on repayment of debt obligations due to political or economic instability, This will lead to credit risks.

Thus, the above are some important types of risk that banks face related to the credit that they give out to borrowers.

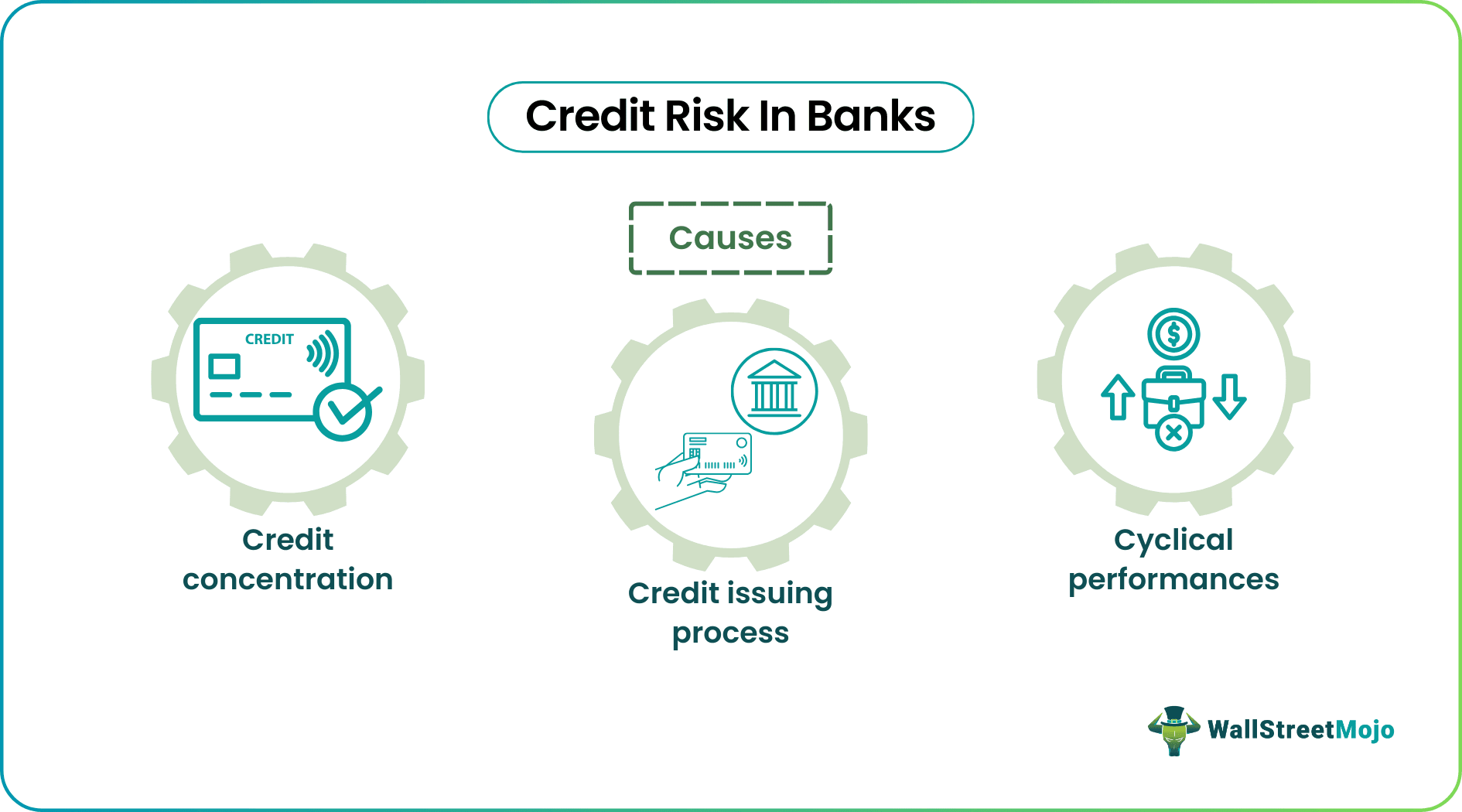

Causes

Although credit risk management for banks is inherent in lending, various measures can be taken to minimize the risk. Poor lending practices result in higher credit risk and related losses. The following are some banking practices that result in higher credit risk for the bank:

Cause #1 – Credit Concentration

Where a majority of the banks’ lending is concentrated on specific borrower/borrowers or specific sectors, it causes a credit concentration. The conventional form of credit concentration includes lending to single borrowers, a group of connected borrowers, or a particular sector or industry.

Therefore, to ensure that the credit risk is kept at a lower rate, lending practices must be distributed amongst a wide range of borrowers and sectors.

Cause #2 – Credit Issuing Process

This includes flaws in the banks’ credit granting and monitoring processes. Although credit risk is inherent in lending, it can be kept at a minimum with sound credit practices.

The following are instances wherein flaws in the credit processes of the bank result in major credit problems –

#1 – Incomplete Credit Assessment

To evaluate the creditworthiness of any borrower, the bank needs to check for (1) the credit history of the borrower, (2) capacity to repay, (3) capital, (4) loan conditions, and (5) collateral. The borrower’s creditworthiness cannot be evaluated accurately without the above information. In such a case, the bank must exercise caution while lending.

#2 – Subjective Decision Making

This is a common practice in many banks and other institutions wherein the senior management is given free rein in making decisions. Where the senior management is allowed to make decisions independent of the company policies, which are not subject to any approvals, there could be instances where loans are granted to related parties with no credit evaluations being done. Accordingly, the risk of default also increases.

#3 – Inadequate monitoring

Where the lending is for the long term, they are almost always secured against assets. However, the value of assets may deteriorate over time. Therefore, it is not only important to monitor the performance of the borrowers but also to monitor the value of assets. If there is any deterioration in their value, additional collateral may help reduce credit problems for the bank. Also, another issue could be the instances of fraud relating to collateral. Banks need to verify the existence and value of collateral before lending to minimize the risk of any fraud.

- Example A – Company P borrowed $250,000 from a bank against the value of its offices. If the bank regularly monitors the value of the asset, in the event of any diminution in its value, it would be in a position to ask for additional collateral from the Company; however, if there is no regular monitoring mechanism, where both the value of the asset decreases and company P defaults in its loan, the bank stands to lose, which could have been avoided with a sound monitoring practice.

Cause #3 – Cyclical Performances

Almost all industries go through a depression and a boom period. During the boom period, the evaluations may result in the good creditworthiness of the borrower. However, the cyclical performance of the industry must also be taken into account to arrive at the results of credit evaluations more accurately.

Example – Company Z obtains a loan of $500,000 from a bank. It is engaged in the business of real estate. The bank must not always go by current trends but must also provide for any future slumps in the industry performance. If it borrows during a boom period, the bank must also consider its performance during any subsequent depression.

Examples

Let us understand the concept of credit risk management in banking sector with the help of some suitable examples.

Example #1

A major bank focuses on lending only to Company A and its group entities. If the group incurs major losses, the bank would also lose a major portion of its lending. Therefore, the bank should not restrict its lending to a particular group of companies alone to minimize risk.

Example #2

A bank lends only to borrowers in the real estate sector. If the whole sector faces a slump, the bank would automatically be at a loss as it cannot recover the monies lent. In this scenario, although the lending is not restricted to one company or a related group of companies if all the borrowers are from a specific sector, there still exists a high level of credit risk.

Example #3

In the absence of strict guidelines, Mr. K, a director of a major bank, will be more likely to advance a loan to a company headed by his relative or close associate without performing adequate credit evaluations. If the loan had been advanced to a third-party company with no associations with Mr. K, there would have been a thorough credit check, and the credit risk would be lower. Therefore, senior management mustn’t be given free rein in lending decisions.

Example #4

Another credit risk example in banks can be assumed, where company X wants to borrow $100,000, but it does not furnish sufficient information to perform a thorough credit evaluation. Therefore it is a higher credit risk and will be eligible for a loan only at a higher interest rate than companies with lower credit risk. In such a scenario, if a bank agrees to lend money to Company X to earn higher interest, it stands to lose both interests as well as the principal as Company X poses a higher credit risk, and it may default at any stage during repayment.

Example #5

Let us consider the same example – Company P borrowed $250,000 from a bank against the value of its offices. There could be instances of fraud wherein loans are taken against fictitious assets. Before lending, it is important that the bank verifies the existence of the asset and its value and not go simply by the paperwork submitted.

Example #6

Company P borrows $100,000 with no collateral based on its performance. Performing credit evaluation before lending is not sufficient. The Bank must regularly monitor the performance of Company P to ensure that it is in a position to repay the loan. In case of poor performance, the bank may request that collateral be provided, reducing the credit risk impact.

Thus, the above credit risk example in banks prove the various situations that may give rise to credit related risks for banks. The examples also highlight the various steps that the banks can and should try to implement in order to keep a control on such risks.

Impact

This kind of risk has a very significant effect on the profit levels, the financial condition and the overall market reputation of the banks. Let us analyse the impact.

- Rise in loan loss provision – Banks need to put aside some fund in anticipation of credit default from borrowers. If there is a heavy loan default, this provision will increase and it will bring down the profitability and capital available for lending. Increase in provision will put restriction on te bank’s ability to give loans.

- Financial loss – Defaut on loan will result in losses because the banks are not getting the amount that they were suppose to get. This will affect their ability to meet the regulatory requirements.

- Strain on liquidity – A large number or loan default will put a strain on the liquidity available. This will result decrease of funds to meet short term obligations and may trigger othe liquidity crisis.

- Damage of reputation – A heavy loan default, will definitely lead to loss of reputation, because customer will feel that the management is not competent enough to handle the business efficiently.

- High borrowing cost – High credit risk will lead to higher cost of borrowing for the banks from interbank market because they will have to face more stringent term of borrowing to compensate for the risk.

Thus credit risk has serious consequences in case of banks impacting their growth, market reputation and financial conditions. Proper steps should be taken to monitor and mitigate such risks as far as possible.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

1. Why is credit risk important for banks?

Credit risk is crucial for banks because it represents the potential for borrowers to default on loans, affecting their financial health and profitability. Managing credit risk helps banks make informed lending decisions, safeguard their capital, and ensure overall stability in the financial system.

2. How does regulatory compliance influence credit risk management in banks?

Regulatory bodies often set guidelines and standards for how banks should assess, manage, and report credit risk. Compliance with these regulations is crucial to maintaining the stability of the financial system and preventing excessive risk-taking.

3. How does credit risk impact a bank’s profitability and stability?

Credit risk directly affects a bank’s profitability and stability. High levels of credit risk can lead to increased default rates, losses on loans, and reduced profits. It can also impact a bank’s capital adequacy and overall financial health.

4. How does an economic downturn affect credit risk for banks?

Economic downturns can increase credit risk as borrowers’ financial conditions deteriorate, leading to higher default rates. In such scenarios, banks may see a rise in NPLs, necessitating more stringent risk management practices.

Recommended Articles

This has been a guide to what is Credit Risks In Bank. We explain it along with its various types, its impact and some suitable examples. You can learn more about finance from the following articles –