Part of our Accounting Concepts guide

What is Bond Accounting?

Bond Accounting means accounting for cash received from the buyer upon issuance of the bond in the balance sheet and its effects on the assets and liabilities side when the bonds are issued at par, premium, or discount. For example, when a bond is issued at par, the cash received is recorded on the asset side, whereas an equal amount is reported on the liabilities side as Bonds payable.

There are three types of bonds.

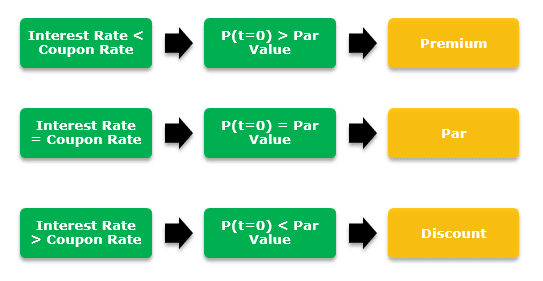

- Bond Issued at Par Value – If the market interest rate is equal to the coupon rate, then the bond issue is at Par

- Bond Issued at Premium – If the market interest rate is less than that of the coupon rate, then the bond issue is at Premium

- Bond Issued at Discount – If the market interest rate is more than that of the coupon rate, then the bond issues are at a Discount

#1 – Bond Accounting – Par Value Bonds

→ Explore all 63 Bonds articles

Here we will take a basic example to understand bond accounting of par value bonds.

Four-year bonds were issued at a face value of $100,000 on January 1, 2008. The coupon rate is 8%. Calculate the bond’s issue price, assuming the market price is 8%.

Calculate the Present Value of the Face Value of $100,000.

You can use the PV Formula to calculate the present value.

Calculate the present value of the Coupon Payments of the Bond.

Calculate the Issue Price of the Bond.

– This is the sum total of Present value of Principal + Present value of Interest = 73,503 + 26,497 = 100,000

– In this case, the bond carrying value is equal to the Bonds Payable.Calculate the ending balance sheet amount of bonds payable for the first year.

– Bond Cash Payment = Face Value of the Bonds * Coupon Rate = $100,000 x 8% = 8,000

– Interest Expense (income statement) = Bond Issue Price x Interest Rate = $100,000 x 8% = 8,000

– Please note that the Interest expense reported in the Income Statement and the Bond coupon payments here are same.

Complete the Bond Accounting table

– Calculate the ending balance sheet amount of Bonds payable for each year.

– We note that the ending bond’s payable balance sheet amount is the same as $100,000 each year as a par value bond.

#2 – Premium Bonds

Let us take the same example for bond accounting of premium bonds. The only change in the market interest rate is 7%.

Four-year bonds were issued at a face value of $100,000 on January 1, 2008. The coupon rate is 8%. Calculate the issue price of the bond, assuming the market interest rate is 7%

Step 1 – Calculate the Present Value of the Face Value of $100,000.

Step 2 – Calculate the present value of the Coupon Payments of the Bond.

Step 3 – Calculate the Issue Price of the Bond.

- This is the sum total of Present value of Principal + Present value of Interest = 76,290 + 27,098 = 103,387

- Here, the carrying value of a bond is not equal to the bonds payable, as this bond is issued at a premium.

The carrying value is found through the following formula:

- Carrying Value = Bonds Payable + Unamortized Premium

- Carrying Value = 100,000 + 3,387 = 103,387

Step 4 – Calculate the Interest Expense and Coupon Payments of the Bond

- Bond Cash Payment = Face Value of the Bonds * Coupon Rate = $100,000 x 8% = 8,000

- Interest Expense (income statement) = Bond Issue Price x Interest Rate = $103,387 x 7% = $7,237

- Please note that the Interest expense reported in the Income Statement and the Bond coupon payments here are different.

- Also, each year the interest expense changes with the ending amount of bonds payable on the balance sheet.

Step 5 – Calculate the ending Balance Sheet amount of Bonds Payable

- Calculate the ending Balance Sheet amount = Beginning Book Value – Coupon payments + Interest Expense

- Ending Balance Sheet (2008) = 103,387 – 8000 + $7,237 = 102,624

- Likewise, the 2009 Beginning book value will be equal to the ending balance sheet bonds payable amount.

Step 6 – Complete the Bond Accounting table

As we note from the table below, the ending balance amount moves towards the face value of the bond at maturity.

#3 – Bond Accounting – Discount Bonds Payable

Let us take the same example of bonds accounting for discount bond with a market interest rate of 9%.

Four-year bonds were issued at a face value of $100,000 on January 1, 2008. The coupon rate is 8%. Calculate the bond’s issue price, assuming the market price is 9%.

Step 1 – Calculate the Present Value of the Face Value of $100,000.

Step 2 – Calculate the present value of the Coupon Payments of the Bond.

Step 3 – Calculate the Issue Price of the Bond.

- This is the sum total of Present value of Principal + Present value of Interest = 70,843 + 25,918 = 96,760

- Here, the carrying value of a bond is not equal to the bonds payable, as this bond is issued at a discount

The carrying value is found through the following formula:

- Carrying Value = Bonds Payable + Unamortized Discount

- Carrying Value = 100,000 – 3,240 = 96,760

Step 4 – Calculate the Interest Expense and Coupon Payments of the Bond

- Bond Cash Payment = Face Value of the Bonds * Coupon Rate = $100,000 x 8% = 8,000 Interest Expense (income statement) = Bond Issue Price x Interest Rate = $96,760 x 9% = 8,708

- Please note that the Interest expense reported in the Income Statement and the Bond coupon payments here are different.

- Also, each year the interest expense changes with the ending amount of bonds payable on the balance sheet.

Step 5 – Calculate the ending balance sheet amount of bonds payable of the first year.

- Calculate the ending Balance Sheet amount = Beginning Book Value – Coupon payments + Interest Expense

- Ending Balance Sheet (2008) = 103,387 – 8000 + $8,708 = 97,469

- Likewise, the 2009 Beginning book value will be equal to the ending balance sheet bonds payable amount.

Step 6 – Complete the Bond Accounting table

As we note from the table below, the ending balance amount moves towards the face value of the bond at maturity.

Recommended Articles

This has been a guide to Bond Accounting. Here we discuss how to account for bonds issued at Par, Discount, and Premium and how it affects the balance sheet, income statement, and cash flows. You may learn more about accounting from the following articles –