Part of our Accounting Concepts guide

What is Accounting for Joint Ventures?

Accounting for joint ventures is accounting done when two or more parties or entities combine their resources, within specific conditions or bound by some agreement, for business or transaction purposes. It can be carried out broadly based on whether a separate set of books is kept or not.

Characteristics

- Sharing of Gains and Losses: Accounting methods for the joint ventures, irrespective of the type of arrangement or venture, mainly include sharing incomes and expenditures, gains, and losses.

- Agreement: Joint ventures are always formed on the agreement of collaboration that is binding under most circumstances. The agreement enlists all clauses and aspects regarding the venture.

- Duration of Venture: The agreement most necessarily includes terms on the period the businesses have come together for a joint venture. This inclusion is made at the beginning and may be subject to changes on mutual consent.

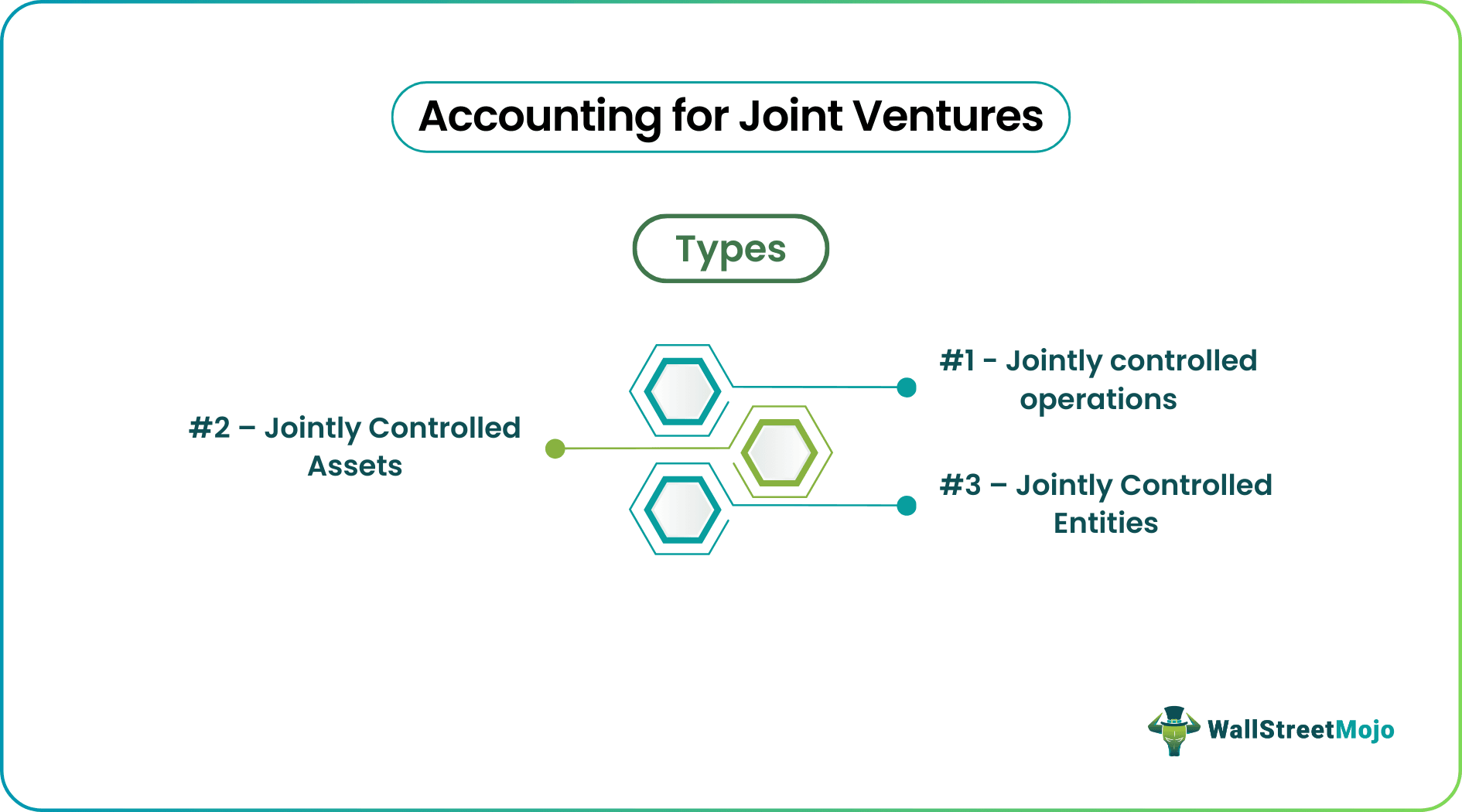

Types of Accounting for Joint Ventures

Joint Ventures are mainly based on three different characteristics:

#1 – Jointly Controlled Operations

These are Joint ventures, where the two separate entities use assets and inventories rather than collaborate. The ventures share the revenue streams and expenses incurred in such an arrangement.

Example

Two businesses can jointly venture by combining their expertise to develop specific products, say software.

#2 – Jointly Controlled Assets

Some joint ventures go on to the extent of collaborating with their assets. The agreement proceedings are complex and vary on a case-to-case basis. The joint venture’s business is recorded as a separate reporting unit, and the corresponding reporting of gains and losses is enlisted.

Example

The oil sector, particularly upstream business, because of the heavy equipment use, has pipelines carrying crude oil or oil mooring systems are some assets that companies share most often. Industries like telecommunications, mining and processing, transport, and logistics departments also share assets.

#3 – Jointly Controlled Entities

In a jointly controlled entity structure, the participating businesses may stretch controlling interests beyond operations, revenues, and assets. The controlling entity may exercise control to the extent that the financial and investing activities of the controlled entity are under the former’s authority.

Example

Telecommunication industry players have ventured into global markets by establishing jointly controlled entities to gain control and make sufficient ground for acquiring regional business insights from a controlled entity.

Accounting for Joint Ventures Journal Entries

→ Explore all 30 Journal Entries articles

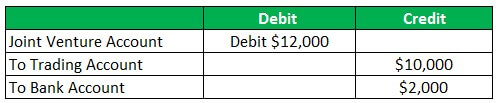

Assume that company X provided furniture to company Y worth $10,000. Company Y sold this stock at the same price, with $2,000 incurred in expenses related to transportation and marketing.

Journal entry in the books of company X:

At the same time, company Y will record this in books as:

Methods to Record Joint Ventures Accounting Transactions

Let’s discuss the following methods.

#1 – Equity Method

The equity method comes into the picture when a company has a significant stakeholding in other companies or companies. If this is the case, let’s say that company X has a 50% controlling interest in company Y. If company Y has annual net earnings of $10 million. The controlling company X will record $5 million in income in its statements. Then, company X will use the equity method to record gains or losses in its financial statements other than its business income.

#2 – Proportional Consolidation Method

This method records the controlled entity’s assets and liabilities on the controlling entity’s financial statements in the proportion of interest held. Thus, if company X has a 50% controlling interest in company Y, then we will see company X recording in its statements 50% of the assets and liabilities of company Y. Note that it will also record the revenues and expenses of company Y proportionally.

Benefits of Accounting for Joint Ventures

- Joint ventures bring in economies of scale as shared assets, machinery, and expertise help in the capacity ramp-up.

- Economies of scale provide for low-cost production.

- Access to different geographies and newer markets.

Limitations

- The disadvantage of commonness in objectives and values.

- Joint ventures may restrict flexibility and innovation.

- Unfavorable impacts from the sharing of culture and human resources.

Conclusion

Accounting for Joint ventures is a popular and beneficial method to expand businesses. Businesses that want to tap newer markets and explore geographies rely on a joint venture. It can be successful in any industry but can fail as well. Technology transfer is a significant benefit that can arise out of joint ventures. Accounting in joint ventures varies due to global accounting standards and business needs, with reliance on the equity method more common these days.

Recommended Articles

This has been a guide to Accounting for Joint Ventures. Here we discuss types and examples of accounting for joint ventures along with its characteristics and detailed explanation. You may learn more about accounting from the following articles –