Part of our Types of Bonds guide

What are Corporate Bonds?

→ Explore all 63 Bonds articles

Corporate bonds are debt securities that public and private companies issue to raise funds and serve their various business purposes. Investors who purchase these bonds become the lending entity for these firms, which pay them interest on the principal amount and return the same once the bond matures.

Key Takeaways

- Corporate bonds are debt securities that companies offer to interested investors, who purchase them in exchange for money, which the former uses to buy resources and grow its business.

- These bonds are classified into various categories based on maturity, credit rating, and interest payments.

- High credit quality, high liquidity, security against risks, and a wide range of options are some of the features of these bonds.

- Even in the event of bankruptcy, companies are legally bound to prioritize paying the interest and principal to the bondholders.

How Do Corporate Bonds Work?

Corporate bonds are considered one of the major components of the U.S. bond market. A firm issues these bonds, which the investors purchase in exchange for an amount. This amount becomes the fund raised by the company to meet its various business requirements. In short, the investors lend a sum of money to creditworthy companies against these bonds.

The companies, in turn, keep paying investors the interest on the principal amount until the bond matures, and repay the full amount to the latter on bond maturity. In the process, however, the investors neither own equity in the company nor do they have any share in the profits it makes.

Investors consider purchasing these bonds only if they find a firm capable of repaying what is lent to them. They, therefore, assess the creditworthiness of the companies based on their ability to perform and generate profit. If the investors are convinced, they hold the bond. In some instances, the companies need to have their physical assets ready as collateral to back the bonds.

As soon as the companies decide to issue bonds, the issuer’s creditworthiness is reviewed first. The S&P Global Ratings, Fitch Ratings, and Moody’s Investor Services are the three U.S. rating agencies that help in assessing the same based on their individual ranking pattern. The ones that have the highest rating are classified as Triple-A bonds. Conversely, the ones with the lowest rating are called junk bonds, or high-yield bonds, as the interest is higher, given the higher associated risk.

Investors look forward to investing in Triple-A bonds for guaranteed timely payments. In addition, retirees also prefer spending on such bonds to supplement their post-retirement earnings.

Types

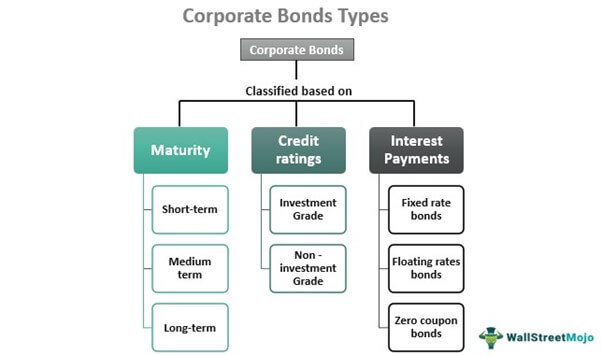

When investors decide to buy corporate bonds, they come across their wide varieties. Such bonds are classified into different categories based on multiple parameters. Let us look at the classifications below:

Maturity-based classification

As the name implies, these bonds are categorized based on their maturity period. They are segmented as:

- Short-term – These bonds mature in fewer than three years.

- Medium-term – These bonds mature in four to 10 years.

- Long-term – Such bonds take more than ten years to mature.

Credit rating-based classification

The credit rating agencies review the issuer and provide a rating to the bonds based on their risks. Based on how trustworthy an issuer is with the payment of interest and principal, these bonds are classified as:

- Investment-grade bonds – These bonds ensure timely payments and repayments and have a lesser risk associated.

- Non-investment grade bonds – These are high yielding corporate bonds with a higher risk of defaults, and hence, the interest rates are higher to compensate for the expected risk.

Interest payment-based classification

Depending on the interest that the companies pay to investors/ bondholders, these bonds are classified into the following categories:

- Fixed-rate bonds – There is a fixed interest rate for these bonds throughout the term. The payments, therefore, are not affected by the market fluctuations in any manner.

- Floating rate bonds – The fluctuations in the market affect the corporate bonds rates and hence, they keep changing. The rates, in this case, are determined based on a bond index or other parameters.

- Zero-coupon bonds – As the name suggests, there is no interest payment for these bonds. The bondholders receive a one-time repayment as soon as the bond matures.

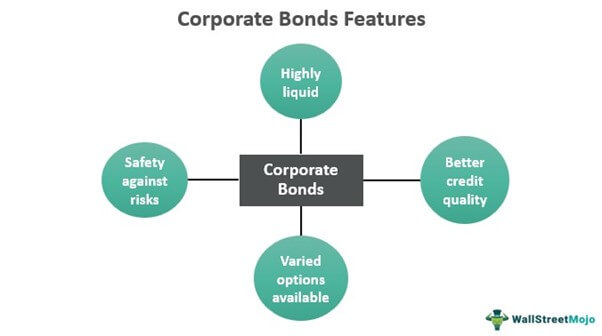

Features

These bonds exhibit multiple characteristics that make them the best debt securities in and across the globe. Some of the common features that make these bonds highly preferred are as follows:

High Credit Quality

When individuals or entities invest in corporate bonds, they spend on a high-quality component. Therefore, such bonds ensure higher return on investment. The bondholders receive the interest on the principal until the firms repay the complete amount after the bond matures.

Highly Liquid

These bonds trade frequently, allowing investors to keep the investment safe for the desired period. It means the investors can invest for two to three years at once and keep enjoying the interest on the same for the desired period and then get the full amount repaid after maturity.

Risk-resistant

Such bonds are less riskier than others. It is because the investors invest after they assess the issuer’s creditworthiness. Hence, they know they will surely get back their lent amount. In addition, these bonds become collateral-backed if the bondholders have any doubts relating to timely payment or repayment.

Varied Options

Corporate bonds are classified based on credit quality, interest payments, and maturity periods. As a result, investors get a wide range of alternatives while choosing which bond to invest in as per their convenience and requirements.

Examples

Let us consider the following corporate bonds examples to understand the concept better:

Example #1

Company A decided to start a separate venture with a different name – X, for which it preferred not using the resources of the parent company. As a result, it issued corporate bonds in the name of company X. As investors knew that parent company A is a trustworthy market entity, they invested in the bonds for two to three years.

On the other hand, Company X used the funds to grow its business while paying the interest timely. Finally, it repaid the bondholders, respectively, after two and three years.

Example #2

Recently, the Federal Reserve raised the interest rates for the corporate bonds first time since 2018, given the rise of 7.9% in annual inflation in February 2022. As a result, the 10-year bond worth $1,000, which paid a 3% interest rate, witnessed a price drop, and the bond’s value fell to $925, the coupon rate remaining the same, i.e., 3%.

In such a scenario, if the coupon or interest rate is increased to 4% for the new bond with a fallen price, the initial 3% rate would appear less attractive. This, in turn, will make investors prefer selling their originally owned bonds and purchasing the ones promising higher yields, leading to the heavy sale of bonds and a further drop in the prices.

Risks

Though the corporate bonds yields are secure enough for investors/bondholders, there is a slight risk. There are times when companies, no matter how reputed and financially strong they are, tend to face financial difficulties. Even in such scenarios, these bonds make the interest and principal payment a legal obligation for the issuers.

In bankruptcy, the companies have to repay the bondholders first, even before the shareholders. It is because defaulting on the payment and repayment adversely affects the company’s goodwill and creditworthiness. As a result, no investor chooses to invest in the same company’s bonds in the future.

Frequently Asked Questions (FAQs)

What are corporate bonds?

Corporate bonds are debt securities that companies issue intending to raise funds to fulfill their business requirements. Before these bonds are bought, the credit rating agencies review the issuer’s creditworthiness. Based on the ratings, the investors decide whether to purchase the bonds issued by a particular firm. In this case, the investors become the lenders, who keep receiving the interest payment regularly and the full amount when the bond matures.

Where to buy corporate bonds?

One can purchase corporate bonds from the primary market. A brokerage firm, bank, broker, or trader can help buy bonds with higher liquidity and high credit quality.

How are corporate bonds quoted?

These bonds are normally priced as a percentage of their face value or in dollars. It is expressed as a fraction. The corporate bond is quoted in 1/8th increments.

Recommended Articles

This is a guide to Corporate Bonds and their meaning. Here we explain how corporate bonds work along with their types, features, risks, and proven examples. You can learn more about accounting from the following articles –