Part of our Accounting Concepts guide

What Are Available For Sale Securities?

Available for Sale Securities are those debt or equity securities investments by the company that are expected to sell in the short run and therefore will not be held to maturity. These are reported on the balance sheet at fair value.

Any unrealized gains and losses arising from such securities are not recognized in the income statement but are reported in other comprehensive income as a part of shareholders’ equity. Any dividend received on such securities, interest income and actual gains and losses when the securities are sold are recognized in the income statement.

- Available for Sale Securities are the company’s debt or equity securities investments forecasted to sell in the short run. Therefore, it cannot be held to maturity and recorded on the balance sheet at fair value. Nevertheless, any unrealized gains and losses from such securities are not recorded in the Income Statement but in other comprehensive income as a shareholders’ equity part.

- The dividend received on securities, interest income, and actual gains and losses when the stakes are sold are considered in the Income Statement.

- Bank and Financial Institutions have widely classified it under the Banking or Trading Books.

Available for Sale Securities Explained

Available for Sale Securities is an important category of an investment portfolio held in the books of accounts of Banks/FI. By classifying these under the AFS Securities category when fair value is down, the unrealized loss can be reported in Other Comprehensive Income without impacting the income statement. The intent of the management decides the classification of Available for Sale investment.

They are broadly classified by Bank and Financial Institutions under the Banking Book or the trading book.

- Banking Book refers to assets on a Bank’s balance sheet that is expected to be held to maturity. Banks and Financial Institutions are not required to mark these assets on a mark-to-market (MTM) basis, and such assets are usually held at historical cost in the books of accounts of the company. The popular category includes assets under the Held to Maturity (HTM) category.

- A trading Book refers to assets held by a Bank which are available for sale and are traded regularly. These assets are acquired with the intent not to be held till maturity but to profit from them over the near term. Banks and Financial Institutions are required to mark these assets on a mark to market (MTM) daily, and such assets are recorded at fair value, also known as mark to market accounting. The popular category includes assets held under the Held for Trading (HFT) category and the Available for Sale (AFS) category.

Available For Sale Securities Explained in Video

Example

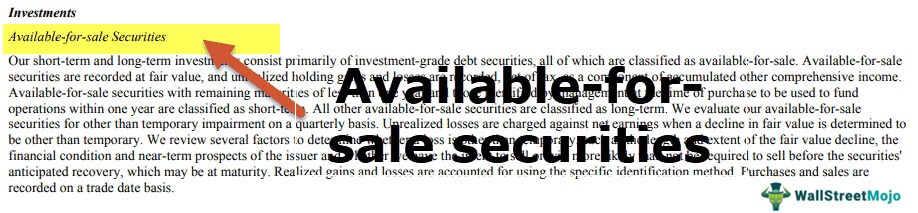

Let us consider the following available for sale securities example:

source: Starbucks SEC Filings

Available for sale investments for Starbucks included Agency Obligations, Commercial Paper, Corporate Debt Securities, Foreign government obligations, US treasury securities, Mortgage, and other ABS, and Certificate of Deposits.

The total fair value of such securities was $151.7 million in 2017.

Journal Entry

The following scenario shows the records of available for sale securities are maintained on the balance sheet:

ABC Bank bought $100000 in equity Securities of Divine Limited on 01.01.2016, classified as AFS in its books of accounts. At the end of the accounting year, ABC Bank realized that the value of the Available for Sale investment had declined to $95000 by the end of the period. At the end of the second-year investment, the value increased to $110000, and ABC Bank sold the same.

#1 – Purchase of Securities

While accounting for available for sale securities to record the purchase of $100000 equity securities of Divine Limited is mentioned as follows:

| Date | Particulars | Debit | Credit |

|---|---|---|---|

| 01.01.2016 | Available for Sale Investment | $100,000 | |

| To Bank Account | $100,000 | ||

| (Journal Entry on the Purchase of Equity Securities of Divine Limited) |

#2 – Decline of Value

Let us check the journal entry to record the decline in the value of equity securities at the end of the year:

| Date | Particulars | Debit | Credit |

|---|---|---|---|

| 01.01.2017 | Loss on Available for Sale Securities (Recorded in Other Comprehensive Income) | $5,000 | |

| To Available for Sale Investment | $5,000 | ||

| (Journal Entry to record decline in the value of equity investment of Divine Limited) |

#2 – Increase in Value

| Date | Particulars | Debit | Credit |

|---|---|---|---|

| 01.01.2018 | Available for Sale Investment | $15,000 | |

| To Loss on Available for Sale Securities (recorded in other comprehensive income) | $5,000 | ||

| To Gain on Available for Sale Securities (recorded in other comprehensive income) | $10,000 | ||

| (Journal Entry to record increase in the value of equity investment of Divine Limited) |

Below is the journal entry to record the increase in the value of equity securities at the end of the second year, as well as the sale of an investment:

| Date | Particulars | Debit | Credit |

|---|---|---|---|

| 01.01.2018 | Bank Account | $110,000 | |

| To Available for Sale investment | $100,000 | ||

| (Journal Entry on sale of equity securities of Divine Limited) |

Thus, when an available for sale investment is classified under the AFS category, any unrealized gain or loss is reported in the other comprehensive income, as shown above in the case of ABC Bank. Once the same is realized the sale of such securities is reported in the Income Statement.

Available for Sale Securities Vs Trading Securities Vs Held to Maturity Securities

| Basis for Comparison | Available for Sale (AFS) | Held for Trading (HFT) | Held to Maturity (HTM) |

|---|---|---|---|

| Meaning | It includes debt and equity securities, which are not expected to be held to maturity or traded in the near term. It includes all securities that are not part of HFT and HTM. | HFT includes debt and equity securities, which are acquired with the intent to profit over the near term. | It includes debt securities, which are acquired with the intent to be held until maturity. |

| Measurement | Recorded in the books of accounts at Fair Value; | Recorded in the books of accounts at Fair Value; | Recorded in the books of accounts at Amortized cost; (Amortized cost is equal to the original price minus any principal payment plus any amortized discount or minus any amortized premium, minus any impairment loss. |

| Treatment of Unrealized gain/losses | Any unrealized gain or loss is reported under Other Comprehensive Income. | Any unrealized gain or loss is reported under Income Statement. | Such securities are reported as current assets (if maturity is less than or equal to one year) or long-term assets (if maturity is more than one year). |

| Trading Book/Banking Book | Classified under the Trading Book of the Bank/FI | Classified under the Trading Book of the Bank/FI | Classified under the Banking Book of the Bank/FI |

Frequently Asked Questions (FAQs)

Are Available for Sale Securities current assets?

On the balance sheet, Available for Sale Securities are classified as current assets when they are to be liquidated in a year or as long-term assets if they are held longer.

Are Available for Sale Securities cash equivalents?

Cash equivalents involve bank accounts and marketable securities. They are debt securities with less than 90 days’ maturities. Still, cash equivalents frequently do not include equity or stock holdings since they may go up and down in value.

Where are Available for Sale Securities on the balance sheet?

Available-for-Sale Securities are recorded at fair value. The changes in value between accounting periods are incorporated in accumulated other comprehensive income in the balance sheet’s equity section.

Recommended Articles

This article has been a guide to what are Available for Sale Securities . Here, we explain their journal entry along with another example, and vs trading securities. You may also learn more from the following accounting articles –

- Long-Term Debt in Balance Sheet

- Tangible vs. Intangible Assets Differences

- Marketable Securities on the Balance Sheet

- What are Asset-Backed Securities?

- Capital Reserve and Revenue Reserve

Recommended Articles

Continue with these closely related articles from the same guide.