Part of our Accounting Concepts guide

What is Held to Maturity Securities?

Held to Maturity securities are the debt securities acquired with the intent to keep them until maturity. This type of security is recorded as an amortized cost on a company’s financial statements. It is usually recorded in the form of debt security with a particular maturity date. The temporary price changes are not reported in the corporate accounting statements. However, interest income is reported in the income statement.

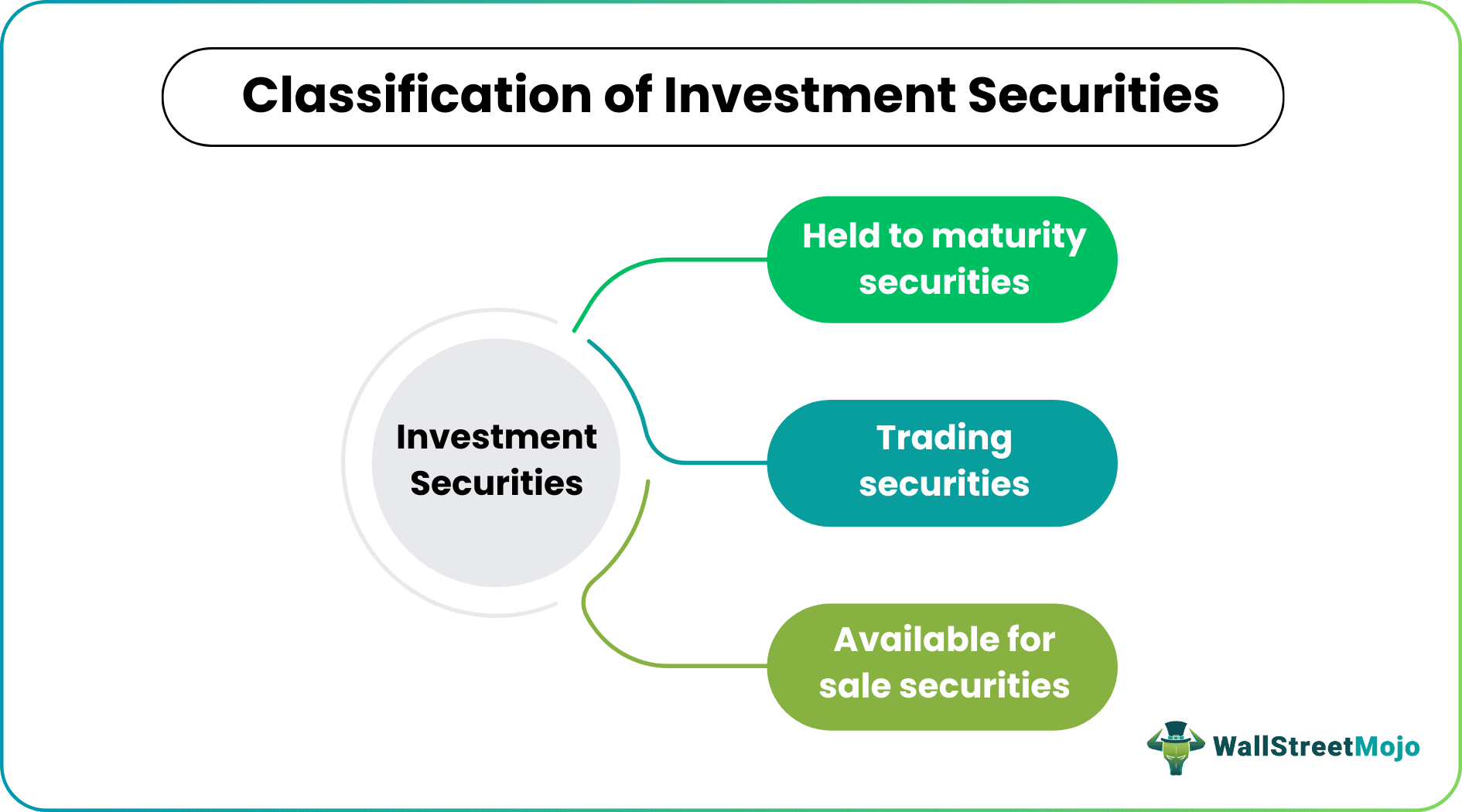

Classification of Investment Securities

One of the major categories of classifying investments by a corporation in debt or equity securities is held to maturity securities. The classification consists of the following categories:

| Historical Cost | Amortized Cost | Fair Value |

|---|---|---|

| Unlisted Equity Investments | Held to Maturity Securities | Trading Securities |

| Loans and Receivables | Available for Sale Securities | |

| Derivatives |

The commonest form of held to maturity securities bonds. We all know that stocks and shares of a company do not have any specific maturity date; they do not come under these securities. This classification of securities is mainly done for accounting purposes as each type of security has its characteristics and is treated differently regarding changes in held to maturity investment values, related gains, and losses in the books of the company’s financials. For example, these securities are considered a current asset if the maturity date is one year or less. But if the maturity date is of a longer period, they are considered long-term assets and are recorded in the balance sheet of a company as the amortized cost. In stark contrast, held to maturity investment held for trade or available for sale comes under fair value.

Held to Maturity Securities Example

Suppose an investor decides to buy debt securities such as bonds. Then the investor has two options- either to hold this security until it reaches its maturity date or to sell it at a premium when there is a decline in the interest rate. This debt security is called held-to-maturity if the holder chooses to hold it for the entire term till the maturity date. So if the holder purchases a 10-year treasury bond and makes the choice of holding it till it matures in the tenth year, then the Treasury bond comes under held-to-maturity.

Jet Blue Example

source: Jet Blue SEC Filings

We note that Jet Blue’s Held to Maturity Securities include Treasury Notes and Corporate Bonds. It had a total of $256 million HTM securities.

Advantages

- The held-to-maturity securities are very predictable as they have a predetermined return, which is locked at the time of buying, and market fluctuations have no impact on their value.

- These securities are very safe and have no risk attached as they are predictable and predetermined. So even if the market value fluctuates, the return will stay the same since the holder will hold the bond until maturity.

- These investments help the investors make long-term financial plans as the purchaser already has confirmed details about when they will receive the return and the amount of return they will get on maturity.

Disadvantages

- Investing in these securities is not a good option if the investors plan to liquidate assets in a short period or for those who prefer investments, which gives the option of cashing in whenever necessary.

- Since held to maturity, investment has already determined returns, which are fixed, so there is no possibility of getting higher returns even if there is a considerable increase in the market and favorable conditions exist in the market.

Difference Between Held-to-Maturity Trading and Available for Sale Securities

- Held to maturity securities are the debt securities, i.e., bonds that the holder intends and can hold until maturity. These are recorded and reported at amortized cost. Subsequent changes in market value are ignored since the return is predetermined.

- Trading securities are debt and equity securities acquired with the intent to profit over the near term. Trading securities are reported on the balance sheet at fair value. The unrealized gains and losses (changes in market value before the securities are sold) are recognized in the income statement. Unrealized gains and losses are also known as holding period gains and losses. Derivative instruments are considered and treated in the same manner as trading securities.

- Available for sale securities are debt and equity securities that are not expected to be held to maturity or traded in the near term. Available for sale securities are reported on the balance sheet at the fair value like trading securities. But any unrealized gains and losses are not recognized in the income statement but are reported in other comprehensive income as a part of shareholders’ equity.

Held to Maturity Securities Video

Recommended Articles

This article has been a guide to what is Held to maturity securities. Here we discuss the HTM securities example along with its advantages and disadvantages. We also look at differences between Held to Maturity Securities vs. Available for Sale Securities. You may learn more about basic accounting from the following articles –