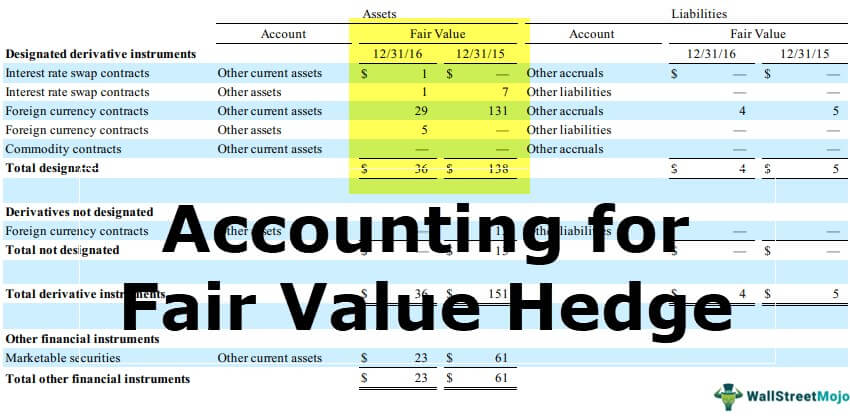

Accounting for Fair Value Hedges

A fair value hedge is a hedge of the exposure to changes in the fair value of an asset or liability or any such item that is attributable to a particular risk and can result in either profit or loss. A fair value hedge relates to a fixed value item.

Fair value hedge pertains to a fixed value item. The necessary steps involved accounting for fair value hedges are as follows:

- Determine the fair value of both the hedged item and the hedging instrument used on the date of reporting financial statements.

- If there is a change in the fair value of the hedged instrument, recognize the profit/loss in the books of accounts.

- Lastly, recognize the hedging gain or loss on the hedged item in its carrying amount.

Accounting for Fair Value Hedges Video Explanation

Accounting for Fair Value Hedge Example

Company Fair has an asset with a current fair value of $ 2000, and the management is concerned that the fair value of the hedge will go down to $ 1900. This will result in a loss to the company.

To offset this loss, the company enters into an offsetting position through a derivative contract, which also has a fair value of $ 2000. Since this is an offsetting position, its fair value will move in the opposite direction as that of the hedged item.

At the time of the closure of books, the following scenarios are possible:

Case #1 – Decrease in the fair value of the hedged item and a simultaneous increase in the fair value of the offsetting hedged instrument

| Sl. No. | Position on reporting date | Value of Hedged Item | Gain / Loss on Hedged Item | Value of Hedged Instrument | Gain / Loss on Hedged Instrument | Net Gain / Loss |

|---|---|---|---|---|---|---|

| 1 | Net Loss | $ 1,920.00 | ($80.00) | $ 2,060.00 | $60.00 | ($20.00) |

| 2 | Net Gain | $ 1,970.00 | ($30.00) | $ 2,040.00 | $40.00 | $10.00 |

| 3 | No Loss / No Gain | $ 1,950.00 | ($50.00) | $ 2,050.00 | $50.00 | Neither loss nor gain |

Case #2 – Increase in the fair value of the hedged item and a simultaneous decrease in the fair value of the offsetting hedged instrument

| Sl. No. | Position on reporting date | Value of Hedged Item | Gain / Loss on Hedged Item | Value of Hedged Instrument | Gain / Loss on Hedged Instrument | Net Gain / Loss |

|---|---|---|---|---|---|---|

| 4 | Net Loss | $ 2,040.00 | $ 40.00 | $ 1,950.00 | ($50.00) | ($10.00) |

| 5 | Net Gain | $ 2,050.00 | $ 50.00 | $ 1,970.00 | ($30.00) | $20.00 |

| 6 | No Loss / No Gain | $ 2,050.00 | $ 50.00 | $ 1,950.00 | ($50.00) | Neither loss nor gain |

Accounting for Fair Value Hedges – Journal Entries

| What will be Debited? | What will be Credited? | |

|---|---|---|

| In the case of the Hedged Item | ||

| a) Loss on the hedging item on the reporting date | Debit the loss to Loss on the Hedged Item A/c This will have an effect on the Profit & Loss A/c and reduce the profit of the company. | Credit the Hedged item. Since this is an asset, the value of the asset will go down, and this will affect the Financial Position i.e., Balance Sheet of the company. |

| b) Gain on the hedging item on the reporting date | Debit the Hedged item. Since this is an asset, the value of the asset will go up, and this will affect the Financial Position i.e., Balance Sheet of the company. | Credit the gain to Gain on the Hedged Item A/c This will have an effect on the Profit & Loss A/c and increase the profit of the company. |

| In the case of the Hedging Instrument | ||

| a) Loss on the hedging instrument on the reporting date | Debit the loss to Loss on the Hedged Instrument A/c This will have an effect on the Profit & Loss A/c and reduce the profit of the company. | Credit the Hedged Instrument. Since this is an asset, the value of the asset will go down, and this will affect the Financial Position i.e., Balance Sheet of the company |

| b) Gain on the hedging instrument on the reporting date | Credit the Hedged item. Since this is an asset, the value of the asset will go up, and this will affect the Financial Position, i.e., Balance Sheet of the company. | Credit the gain to Gain on the Hedged Instrument A/c This will have an effect on the Profit & Loss A/c and increase the profit of the company. |

| Net effect of both the Hedging Item and the Hedging Instrument | ||

| Net loss on the date of reporting | Net loss will decrease the overall profit of the company. | Net reduction in the Net Assets of the company |

| Net gain on the date of reporting | Net increase in the Net Assets of the company | Net gain will increase the overall profit of the company. |

Recommended Articles

This has been a guide to Accounting for Fair Value Hedges. Here we discuss fair value hedge journal entries along with practical examples. You may learn more about accounting from the following articles –