Part of our Income Statement guide

What is the Statement of Comprehensive Income?

Statement of Comprehensive Income refers to the statement which contains the details of the revenue, income, expenses, or loss of the company that is not realized when a company prepares the financial statements of the accounting period, and the same is presented after net income on the company’s income statement.

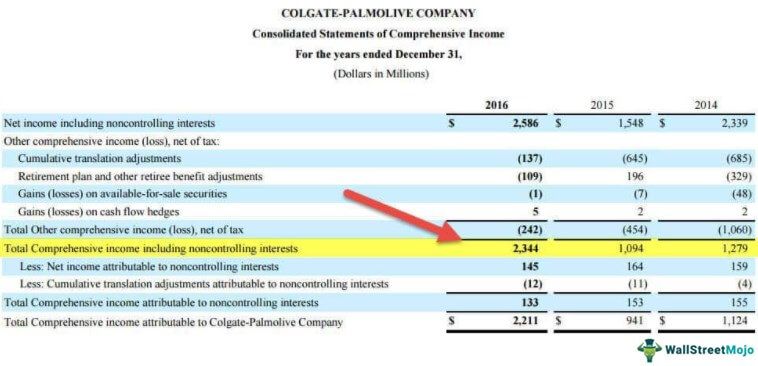

We note above that Colgate Reported a Net Income of $2,596 million in 2016. However, its total Comprehensive Income, including noncontrolling interests, was $2,344 million in 2016.

How to Interpret the Statement of Comprehensive Income (with Examples)?

To understand this, we must first pay heed to the opposite of comprehensive income. The opposite of comprehensive income is narrowed-down income or income from its main operation.

Below is the snapshot of the Consolidated Income Statement of Colgate.

source: Colgate SEC Filings

We note that Colgate’s Net income, including noncontrolling interests, is $2,586 million. As we see above, the Income Statement contains the revenues and expenditures related to the business’s main operations.

What about those items (gains/losses) that are excluded from the Income Statement? Where do they get adjusted?

Let us understand this concept with the help of a basic statement of comprehensive income example.

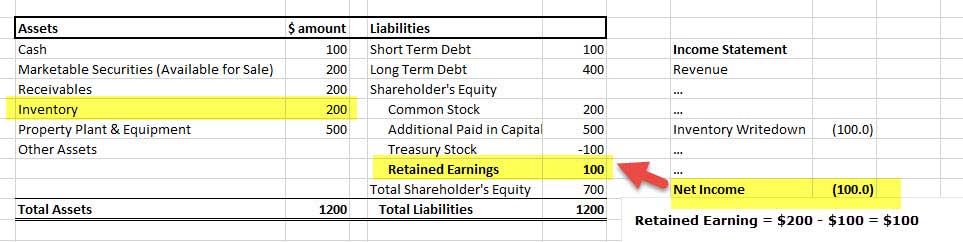

Given below is the balance sheet of Company XYZ.

Total Assets = Total Liabilities = $1300

#1 – Inventory Writedown from $300 to $200

- If the inventory value decreases from $300 to $200, then the Total Assets amount on the balance sheet will decrease to $1200.

- How does the Total Liabilities figure get adjusted? Answer: Through the Income Statement -> Retained Earnings

- The inventory write-down of $100 ($300 – $200) will flow from the Income Statement.

In this example, we have assumed taxes to be zero. The above case is for gains and losses flowing through the income statement.

Let’s take a different case where such gains and losses do not flow through the Income Statement.

#2 – If the Marketable Securities (Available for Sale) decrease to $100

- If the value of the Available for Sale Marketable Securities reduces from $200 to $100, then the Total Assets amount in the balance sheet will decrease to $1200

- However, the Total Liabilities are still at $1300. Accounting rules don’t allow us to adjust this unrealized loss on Available for Sale securities from the Income Statement. Instead, they are adjusted directly in the Shareholder’s Equity Section through “accumulated other comprehensive income.”

Two takeaways from the above statement of comprehensive income examples –

- Gains and Losses on items that are not allowed to flow from the income statement are included in the Statement of Comprehensive Income.

- Other Comprehensive Income for the period gets added to the Accumulated Other Comprehensive Income in the Shareholder’s Equity Section.

Statement of Comprehensive Income Explained in Video

Format for Statement of Comprehensive Income

Comprehensive income connotes the detailed income statement, where we will also include income from other sources and the income from the main function of the business.

source: Colgate SEC Filings

As seen from the above statement, we have to consider two primary components –

- Net income or loss from the income statement of the company &

- Other Comprehensive Income (net of taxes)

Here’s a simple list of items included in the “Statement of Comprehensive Income.”

#1 – Translation Adjustments

Foreign currency translation gains or losses do not flow through the income statement; therefore, they are included. As we see below, the cumulative foreign currency translation adjustment for Colgate is – $97 million (pre-tax) and – $125 million (net of taxes)

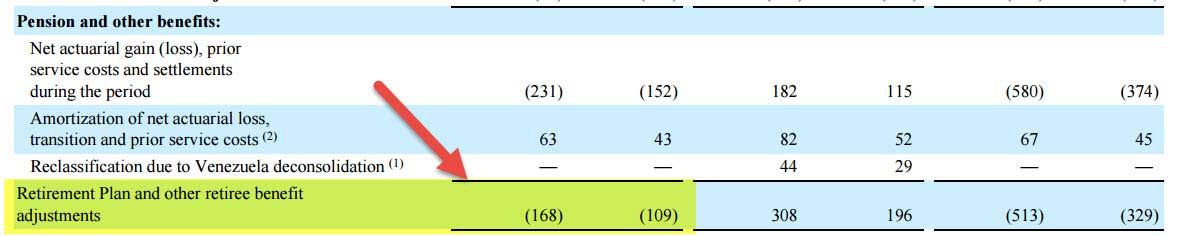

# 2 – Pension & Other Benefits

Following Pension related gains or losses are included –

- Pension or post-retirement benefit plan gains or losses

- Pension or post-retirement benefit plan prior service costs or credits

- Pension or post-retirement benefit plan transition assets or obligations that are not recognized as a component of the net periodic benefit or cost

We note in Colgate that the Retirement Plan and other retiree benefits adjustments are – $168 million (pre-tax) and – 109 million (post-tax).

#3 – Available for Sale Securities

Available for sale securities are securities that are available for sale (literally!) and have a readily available market price. At the end of each financial year, companies need to value the available for sale securities. Any gains/losses due to the change in valuation are not included in the Income Statement but are reflected in the Statement of Comprehensive Income.

Colgate’s Gains (losses) on available for sale securities is – $1 million (post-tax).

#4 – Cash Flow Hedges

Like the list above, unrealized gains and losses from cash flow hedges flow through the Statement of comprehensive income. Colgate Gains (losses) on cash flow hedges included in other comprehensive income are $7 million (pre-tax) and $5 million (post-tax).

Consolidated Statement of Comprehensive Income format

Here’s a snapshot of how you need to format your consolidated statement of comprehensive income.

| Particulars | Year 1 | Year 2 |

|---|---|---|

| Net Income | ****** | ****** |

| Other Comprehensive Income/Loss: | ||

| Change in Foreign Currency Translation Adjustment | ||

| Available for Sale Investments | ||

| Cash Flow Hedge | ||

| Other Comprehensive Income/Loss (if any) | ||

| Comprehensive Income | ****** | ****** |

Why Report Statement of Comprehensive Income every Quarter?

Now you may ask why the publicly traded companies must prepare a consolidated statement of comprehensiveness every quarter?

Here’s the explanation.

- First of all, these reports are important because they are compared with the last quarter’s report and last year’s same quarter so that the SEC can understand whether any discrepancy lies in the statement.

- Second, the ultimate aim of these reports is to help the investors to know better so that they can make more informed decisions about which company they should invest in and which company they should avoid investing in completely.

Things you need to know as an investor

Even after looking at the consolidated comprehensive income statement, you should consider a few things as an investor. Here are they –

- First of all, no single document can tell you the whole thing about a company. To be sure, you need to get your hands on an annual report of the company (to shareholders), the annual report (under 10K), and the consolidated income & comprehensive income statement (under 10Q). Also, checkout SEC Filings Types.

- If you appreciate the complexities and technicalities of finance, you will enjoy the detailed approach thoroughly by looking at all the documents. But, if you are starting as an investor, it’s better to learn from someone or hire someone to help you with these statements.

- Instead of relying only on statements, it is recommended that you also go for ratio analysis to get a firm grip on how the firm is performing. You can start with the cash conversion cycle, turnover ratios, DSCR, Interest Coverage Ratios, ROIC, etc.

In the final analysis

A statement of comprehensive income is the overall income statement that consolidates the standard income statement, which gives details about the repetitive operations of the company, and other comprehensive income, which gives details about the non-operational transactions such as the sale of assets, patents, etc. But don’t depend solely on it. Look for other statements to get an inner view of the firm, go through their last ten years of statements, and try to see a trend coming forward. It will help you understand the risk-return ratio even before investing in the organization.

Recommended Articles

For more on Income Statement, explore these related articles from our Income Statement guide.