Carrying Amount Meaning

The carrying amount, also known as the book value of an asset, is the cost of tangible assets, intangible assets, or liability recorded in the financial statements, net of accumulated depreciation/amortization, or any impairments or repayments. This carrying cost may differ from the current market value of such asset or liability as the market value of any asset or liability depending upon the demand and supply market conditions.

A gross carrying amount is defined as the value that the shareholders will get in the event of liquidation of the company. This value is generally determined by keeping in mind the GAAP or IFRS accounting principles when accounted for.

- It can be described as the value received by the shareholders in the case of a firm liquidation. Usually, when accounting for this value, the GAAP or IFRS accounting principles are considered.

- The market value of an item, which is also frequently referred to as its fair value, is the amount for which it can be sold on the open market. It is the price at which an asset can be exchanged on a free market.

- There are several instances, particularly with start-up businesses, where the assets’ market value is much lower than indicated in the books of accounts.

- This figure is crucial for fundamental and value growth investors since a firm with a high market value compared to its book value represents a potential investment opportunity.

Carrying Amount Explained

A carrying amount is a company’s fundamental value, which can be easily defined as how much the net assets of the company are worth. For fundamental and value growth investors, this value is important because for a company having a high market value from its book value is a good opportunity for investing. The price to book value ratio is a good indicative ratio to measure the carrying amount of the company. The ratio indicates whether you’re paying too much for what would remain if the company is approaching bankruptcy.

To know what a carrying amount is, let us check what its value conveys:

When Fair Value Is Less Than Carrying Value

When the company’s market value of the shares and its share is lower than the carrying amount, it indicates that the market and the shareholders have lost confidence in its fundamentals. The future earnings are not enough to pay its debt and liabilities. There are many cases, especially with start-up companies, in which their book value and market value differ significantly, and the assets are worth much less in the market than is shown in the books of accounts. Ideally, the company should be sold off when its market value becomes less than its book value.

When a Fair Value is greater than the Carrying Value

When the company’s market value exceeds the book value of the company, the market is positive about the future earnings prospects and increased investments. As a result, it increases profits, which will increase the market value of the company and, in turn, higher returns on the stock. A company that has consistently higher profits and increased profits will have a market value greater than the book values of the company.

However, sometimes significantly higher market values indicate overvalued stocks and are most likely to experience a steep fall in the market prices of the stocks as investors have been too positive about the stock, and the market needs to be corrected.

When a Fair Value is equal to the Carrying Value

It is seldom that the investor will think and think that the company’s carrying amount is equal to that of the market. However, in that case, the company can be called a perfectly valued company.

Formula

The carrying amount formula is derived based on the following scenarios:

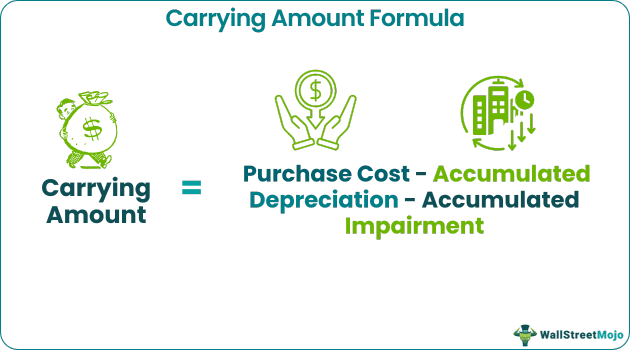

- If the company has purchased some patent or any other intangible asset on its balance sheet, the formula to calculate the asset’s carrying amount will be (Original purchase cost – Amortization Expense).

- On the other hand, the formula for physical assets calculation, such as machinery or building, will be (Original purchase cost- depreciation).

Below is the overall formula

Carrying Amount Formula = Purchase Cost – Accumulated Depreciation – Accumulated Impairment

How to Calculate?

Company XYZ purchased machinery for $20,000 on Oct-18. It uses Straight-line depreciation on the asset @ 10%. Accounting for the asset will be done as follows.

For the year ending Dec-18. The asset depreciation amount will be $20,000*10/100*3/12 = $500.

Since the asset was purchased in the month of October, the depreciation amount on the asset will only be charged for 3 months, i.e., $500 for that year. Hence on thebalance sheet for the yearending 31-Dec-18, the asset’s carrying amount will be $20,000- $500 = $15,000.

Full depreciation will be charged on the asset until the scrap value becomes zero for the next year.

Impairment Test

The carrying amount of an asset plays an important role in asset impairment testing and analysis. The International Accounting Standards Board (IASB) adopted IAS 36 in April 2001, which was initially developed by the International Accounting Standards Committee in 1998.

Through this impairment test, the recoverability of an asset is examined. To determine this, however, the recoverable amount and carrying amount of the asset is studied against each other. If the carrying amount exceeds the amount to be recovered, the asset is considered impaired.

Carrying Amount Vs Fair Value

The asset’s market value, which is also often referred to as the fair value of an asset, means how much an asset can sell in the market. It is the value for which an asset can be sold in the open market. For example, Company XYZ has total assets of $10,000 with total liabilities of $80,000. Therefore, the company’s book value will be $20,000, which is the value of the assets less the value of liabilities.

The market value often differs due to the following factors: –

- A difference in the depreciation methods which is used by the company and other evaluators

- The forces of supply and demand factors make the market value of an asset vary over time depending upon the availability of the asset, which can result in substantial variance in the values.

- Market Value is very subjective in nature, whereas this value is based on accounting principles and can be traced back to the purchase receipt of an asset.

- The market value of an asset is not related to the company’sfinancial statements. In contrast, this value of an asset is related to the profit and loss and balance sheet item.

For example, the company purchases equipment for $200,000 each month. The company depreciates the asset for $5,000 for four months and then decides to sell the asset. The asset is sold for $150,000. Since the asset is sold for only $150,000 the market value of the asset is $150,000 but the carrying amount of the asset will be ($200,000 – $20,000) = $180,000. Hence the company will book $30,000 in the profit and loss statement.

Frequently Asked Questions (FAQs)

Are carrying value and net assets the same thing?

Analysts use a company’s balance statement to determine value. It is generally the same as the company’s net book value (or net asset value), although these definitions aren’t generally used interchangeably. In addition, it indicates the company’s equity.

What happens if the carrying amount exceeds the fair value?

The difference between an asset’s carrying value and its recoverable value is known as an impairment loss. The higher an asset’s fair value fewer costs of disposal, and its value in use is the recoverable amount for that asset or cash-generating unit.

Can carrying value actually decrease?

Negative carry can occur with any investment that incurs higher holding costs than it generates in payments. For example, a holding in securities (such as bonds, stocks, futures, or currency) or a business might be considered a negative carry investment.

Recommended Articles

This article has been a guide to Carrying Amount and its meaning. We explain its formula, vs fair value, the steps on how to calculate it & its role in impairment tests. You can learn more about accounting from the following articles –