What Is The Amortization of Intangible Assets?

Amortization of Intangible Assets refers to the method under which the cost of the different intangible assets of the company (assets which do not have any physical existence, cannot be felt and touched like trademark, goodwill, patents, etc.) are expensed over the specific period.

The term “intangible assets” refers to those not physical assets. These can be assets such as trademarks, copyrights, patents, etc. In simple words, it refers to the expensive cost of a firm’s intangible assets of a firm over its total lifetime.

Amortization of intangible assets is similar to depreciation, which is the spreading out the cost of the firm’s assets for its lifetime. The main difference between amortization and depreciation is that the prior is used in the case of intangible assets, and the other one is used in the case of tangible assets.

Amortization Examples

Example #1

- Let us consider the case of a business organization, say Company ABC, which buys a patent for $ 15,000 for 15 years. So the company can utilize the patent for its benefit for 15 years, and the total value of the patent, which is $ 15,000, is amortized over the time of 15 years.

- So the Company ABC will amortize an expense of $ 1,000 each year and deduct that value from the value of the patent on its balance sheet every year.

- In this manner, the total value of the patent is expensed by the amortization method during the patent’s useful life.

Example # 2 (Patent becomes worthless after some years)

- There can be cases where the useful life of the patent owned for 15 years does not count up to 15 years.

- Let us consider that the patent became worthless after five years for Company ABC. So the useful life of the intangible asset, namely the patent, is reduced from 15 to 5 years.

- So, for only five years, the asset’s cost can be amortized, and it is expensed by only $ 1,000 each year.

- In this case, the remaining cost, which is $ 10,000, which is unamortized, is to be expensed together, and the patent value is reduced to $ 0 on the firm’s balance sheet.

Example # 3 (Additional costs)

- Another case is when there comes an excess of the expenses in terms of the patent, maybe because of a break in terms of a third party. In such a case, the firm needs to hire a lawyer.

- So let us say the firm hired a lawyer, who charged the company with a cost of $ 10,000 and successfully defended the patent. In such a case, the amount spent by the lawyer, which is $ 10,000, is added to the patent’s value and amortized over the remaining useful life of the patent.

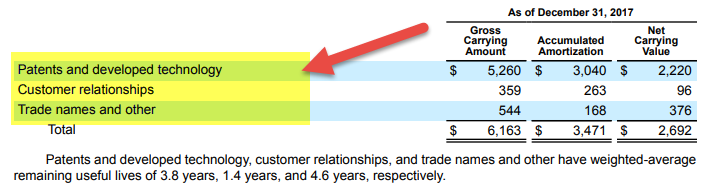

Google’s Amortization of Intangible Assets

source: Google 10K

Patents and developed technology

- Net Carrying Value = $2,220 mn

- The remaining useful life is 3.8 years.

- Amortized expense related to Patents and developed technology in 2018 will be = $2,220/3.8 = $584.21 mn

Customer Relationships

- Net Carrying Value = $96 mn

- The remaining useful life is 1.7 years.

- Amortized expense related to Patents and developed technology in 2018 will be = $96/1.4 = $68.57 mn

Patents and developed technology

- Net Carrying Value = $376 mn

- Remaining Useful life is 4.6 years;

- Amortized expense related to Patents and developed technology in 2018 will be = $376/4.6 = $81.7 mn

Uses of Amortization of Intangible Assets

Amortization of intangible assets can be used for two purposes, the first for accounting purposes and the second for tax deferment purposes.

The amortization methods used for these two purposes are different from each other. When used for tax purposes, the actual lifespan of the assets is not considered, and only the base cost is amortized over a specific number of years. Intangible assets are not physical, and finding an actual value for them is not as easy as in the case of tangible assets. Some regulations group certain assets under intangible assets and give them particular value.

Video Explanation of Amortization of Intangible Assets

Amortization of Intangibles Assets – Infinite useful life

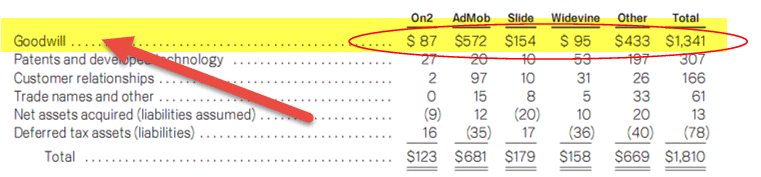

Intangible assets without a finite useful life, i.e., with an indefinite useful life, are not amortized but are reviewed for impairment whenever changes in events or circumstances indicate that the carrying amount of an asset may not be recoverable.

For example, Goodwill. Below is the Google Inc purchase price allocation of all the acquisitions taken from its 10-K Report.

Under U.S. GAAP SFAS 142, goodwill is not amortized but is tested annually for impairment Goodwill impairment for each reporting unit should be tested in a two-step process at least once a year.

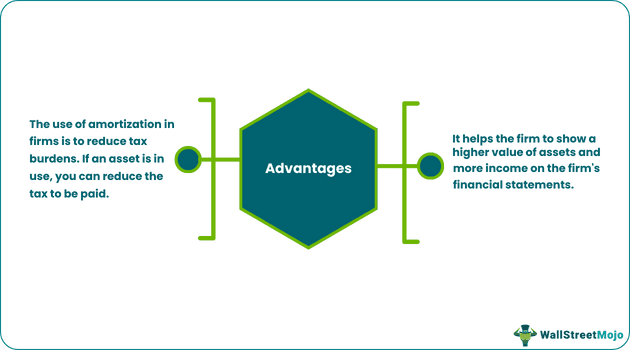

Advantages

- Primarily, the use of amortization in firms is to reduce tax burdens. As long as an asset is in use, you can reduce the tax to be paid.

- It helps the firm show a higher value of assets and more income on firm’s financial statements.

Conclusion

The use of the amortization of intangible assets is beneficial for the firm. It helps in assessing the value of the amortized asset with ease. At the same time, it helps assess the benefits of owning it. It, moreover, helps the firm by reducing the tax burden they possess. The amortization of capital expenses helps the firm always possess minimum financial security.

Recommended Articles

This article has been a guide to the Amortization of Intangible Assets and its definition. Here we discuss how to calculate amortization and practical examples of Google Inc. Here we also discuss the uses and advantages of the amortization of intangible assets. You may also have a look at the following articles on accounting –