What is Negative Goodwill?

The negative goodwill arises in the financial statement of the company purchasing another company when the fair value of net identifiable assets is greater than the purchasing price paid to acquire the company.

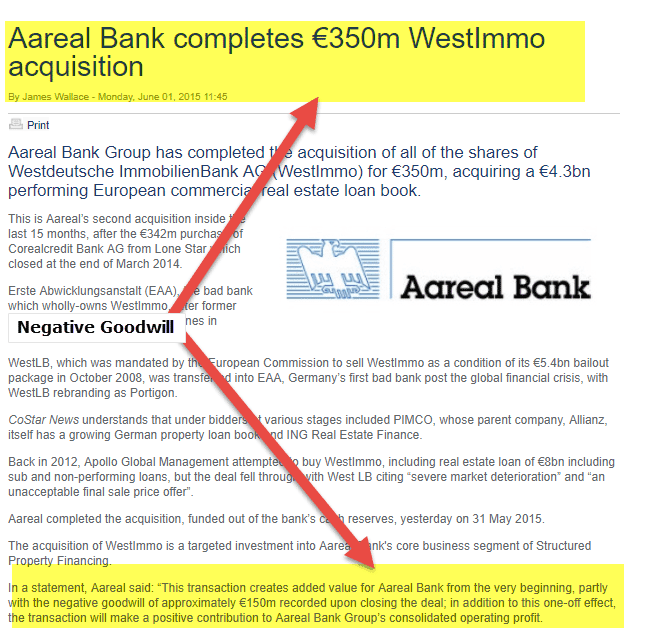

We note from above that, Aareal Bank completed the acquisition of Westlmmo for Euros 350 million, acquiring a Euro 4.3 billion performing European commercial real estate loan book. This transaction added value to Aareal Banks as Euro 150 million was recorded as Negative Goodwill upon closing the deal.

How to Interpret Negative Goodwill?

Negative Goodwill is a term coined in the context of one company taking over another. It’s again occurring to the former when the consideration paid for an acquisition is less than the fair market value of its net tangible assets. In literal terms, Negative Goodwill implies a bargain purchase.

The critical aspect to ponder here is why would someone be willing to sell the entity’s assets below its fair market value? Any wise person would think the assets can be disposed of at their fair market price, then why does the question of Negative Goodwill arise in the first place.

Well, let’s look into this. There may be a circumstance that may force such a situation, namely:

- Forced or distress sale

- Recognition or measurement exceptions for particular items discussed under IFRS 3

- Errors in the valuation of assets and controlling or non-controlling interest in any entity

Negative Goodwill is again for the acquirer entity and should be recognized as its books. Before that, the acquirer must review the calculations to ensure that everything is arithmetically correct. There is no mistake in calculating various elements as Negative Goodwill does not arise normally. After all, buying a business costlier than the market price and believing that we have acquired the same at a profit is not a wise idea.

Once it is confirmed that the net result is again on the acquisition, the resulting gain should be recognized in the books (Profit & Loss Account) of the acquirer company.

For any change in the management or control of the company, a valuation of the assets must be performed according to generally accepted accounting standards. This exercise is commonly referred to as a purchase price allocation. It is called so because the purchase price of the acquired company is allocated across all tangible and intangible assets acquired. Generally, the acquired company’s value is greater than the value of the acquired assets. It may also be understood as the whole company is greater than the sum of its parts. That additional value of the whole company over and above is referred to as Goodwill. There are certain transactions in which the total value of the parts put together (individual assets) acquired in a transaction exceeds the price paid for the entire company. It is commonly known as “bargain purchase.”

Negative Goodwill Video

Positive Goodwill Example

To understand Negative Goodwill, it’s helpful to understand Positive Goodwill beforehand. In a typical acquisition scenario, tangible assets include accounts receivable, inventory, and fixed assets, i.e., machinery, plant, equipment, etc. There may be several intangible assets and tangible assets that form a part of the acquisition and are seen as value drivers. These intangible assets can be a brand name, patents, or a certain technology, licenses, positive customer relationships, and an additional business pull. To pass the allocation test, it is mandatory to have a legal and enforceable contract to use these assets in favor of the Acquirer Company. After allocating value to all of these assets, any excess amount left is considered Positive Goodwill.

The following example will show the purchase price allocation for a $ 5 million acquisition:

| Tangible Asset: | Fair Value of Assets |

|---|---|

| Receivables | $ 1,500,000 |

| Plant & Machinery | $ 1,000,000 |

| Land & Building | $ 100,000 |

| Intangible Assets: | |

| Patents | $ 500,000 |

| Trade Names | $ 1,100,000 |

| Unallocated Intangible Assets: | |

| Goodwill | $ 800,000 |

| Purchase consideration | $ 5,000,000 |

As can be seen from the above example, the fair value of the assets taken over is USD 4.2 million. It effectively means that the price paid over and above the fair value of the assets is Positive Goodwill, i.e., USD 0.8 million.

Also, have a look at Impairment of Assets | Goodwill Impairment

Negative Goodwill Example

While most of the time, business acquisition transactions happening would result in Positive Goodwill, there may be instances where the fair value of the assets taken over is more than the price paid for the acquisition. This scenario typically results in Negative Goodwill and is generally termed “Bargain Purchase.” Using the same example used earlier, if the purchase price/deal price is USD 4 million instead of USD 5 million, the purchase allocation would be as follows:

| Tangible Asset: | Fair Value of Assets |

|---|---|

| Receivables | $ 1,500,000 |

| Plant & Machinery | $ 1,000,000 |

| Land & Building | $ 100,000 |

| Intangible Assets: | |

| Patents | $ 500,000 |

| Trade Names | $ 1,100,000 |

| Unallocated Intangible Assets: | |

| Goodwill | $ (200,000) |

| Purchase consideration | $ 4,000,000 |

This type of scenario calls for additional analysis, which we will look into shortly.

Signs of Negative Goodwill

Several indications suggest that a transaction may be a bargain purchase. Some indicative signs of bargain purchases include:

- The acquired company has incurred financial losses in the recent past or has been being in debt and is not able to service its debt.

- The netbook value of the assets taken over is more than the purchase price paid for the acquisition.

- The transaction has been carried out secretly, and a possibility of higher value has not been explored.

- A single bidder has taken advantage of the situation and the absence of other bidders.

- The deal was finalized in haste and within a brief period.

- The seller was compelled to sell the business against his will or in a desperate situation.

- The existence of a very fact that the acquirer has more knowledge of the acquired business.

There should be a very strong reason why a transaction is a bargain transaction, and the same should be documented properly as to why a bargain purchase represents the fair market value of assets taken over. Suppose the purchase price allocation cannot be articulated precisely why the purchase price allocation should have Negative Goodwill. In that case, this will call for a re-evaluation of the fair value of every asset. In the absence of the above, it may be concluded that the fair value of the overall business is more than the purchase price.

It would simply mean that the transaction did not happen at a fair value. In such a situation, the concluded fair value is the amount allocated to the acquired assets. Any excess amount over and above the business’s fair value would be treated as extraordinary gains.

Conclusion

The prime implication of a bargain purchase is the gain to the buyer if it is a purchase below the fair value of the acquired assets. A bargain purchase gain should be recognized at the time of acquisition and recorded as an extraordinary income at the date of acquisition. However, it is essential to note that this is again to account only. It would not be included in the calculation of income subject to taxes.

Recommended Articles

This article has been a guide to what negative goodwill is, and its meaning. Here we discuss how to interpret negative Goodwill and its example and sign. You may learn more about financing from the following articles –