Part of our Fixed Assets and Depreciation guide

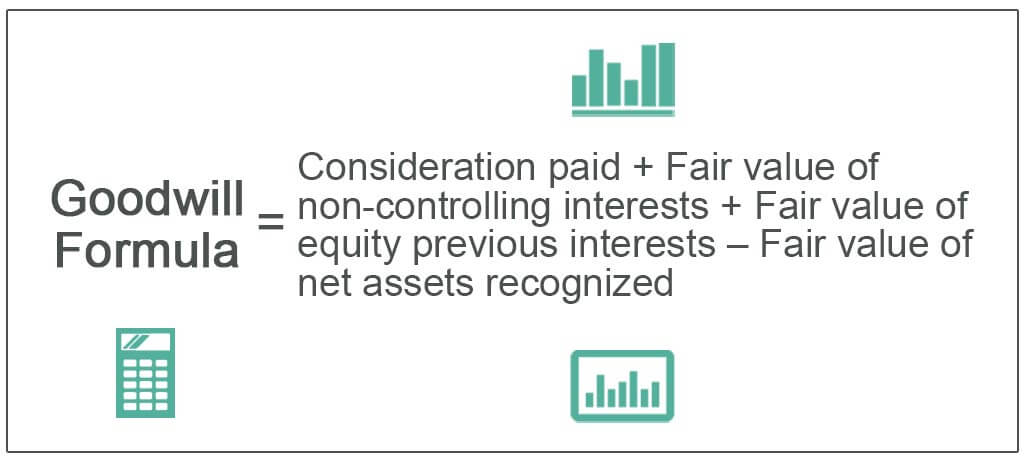

What is the Goodwill Formula?

The term “goodwill” refers to that intangible asset that comes into play only when a company is planning to acquire another company and is willing to pay a price that is significantly higher than the fair market value of the company’s net assets. In short, goodwill can be seen as the difference between the purchase price and the fair market value of a company’s identifiable assets and liabilities.

The calculation of the goodwill equation is done by adding the consideration paid, the fair value of non-controlling interests, and the fair value of previous equity interests and then deducting the fair value of net assets of the company.

The goodwill calculation method is represented as,

Goodwill Formula = Consideration paid + Fair value of non-controlling interests + Fair value of equity previous interests – Fair value of net assets recognized.

Steps / Method to Calculate Goodwill

The goodwill can be calculated by using the following five simple steps:

Firstly, determine the consideration paid by the acquirer to the seller, and it will be available as part of the deal contract. The consideration may be paid in stocks, cash, or cash-in-kind. The consideration is valued either by an appropriate valuation method or the share-based payment method.

Next, determine the fair value of the non-controlling interest in the acquired company. The portion of equity ownership in a subsidiary is not attributable to the parent company.

Next, determine the fair value of equity in previous interests.

Next, figure out the fair value of the net assets recognized in the acquired company. It is the net of the fair value of assets and the fair value of liabilities. It is easily available on the balance sheet.

- Finally, the goodwill equation is calculated by adding the consideration paid (step 1), non-controlling interests (step 2), and the fair value of previous equity interests (step 3) and then deducting the net assets of the company (step 4) as shown below.

Goodwill Formula = Consideration paid + Fair value of non-controlling interests + Fair value of equity previous interests u2013 Fair value of net assets recognized

Goodwill Explained in Video

Examples of Goodwill Calculation Method (with Excel Template)

Let us look at some simple to advance examples of the Goodwill Formula and calculate it to understand it better.

Goodwill Calculation – Example#1

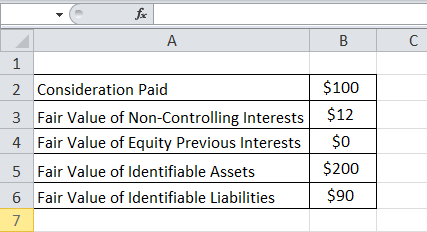

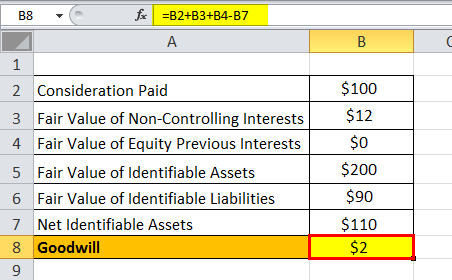

Let us take the example of company ABC Ltd which has agreed to acquire company XYZ Ltd. The purchase consideration is $100 million to obtain a 95% stake in XYZ Ltd. As per an esteemed valuation company, the fair value of the non-controlling interest is $12 million. It is also estimated that the fair value of identifiable assets and liabilities to be acquired is $200 million and $90 million, respectively. There are no equity interests. Calculate the goodwill based on the given information.

Given,

- Consideration paid = $100 million

- Fair value of non-controlling interests = $12 million

- The fair value of equity previous interests = $0

Below is given data for calculation of goodwill of company ABC Ltd

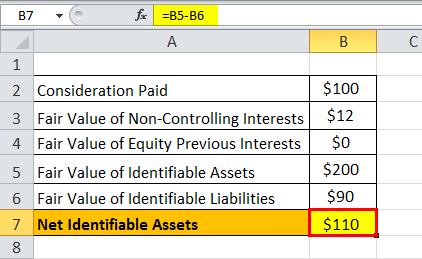

First, we need to calculate Net identifiable assets of company ABC Ltd

Therefore, Net identifiable assets = Fair value of identifiable assets – Fair value of identifiable liabilities

= $200 million – $90 million

Net Identifiable Assets = $110 million

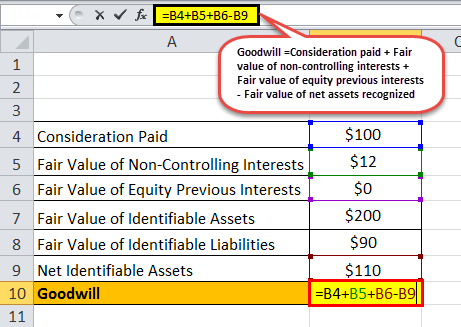

Therefore, the method to calculate goodwill will be as follows,

Goodwill Equation = Consideration paid + Fair value of non-controlling interests + Fair value of equity previous interests – Fair value of net assets recognized

Goodwill formula = $100 million + $12 million + $0 – $110 million

= $2 million

Therefore, the goodwill generated in the transaction is $2 million.

Goodwill Calculation – Example#2

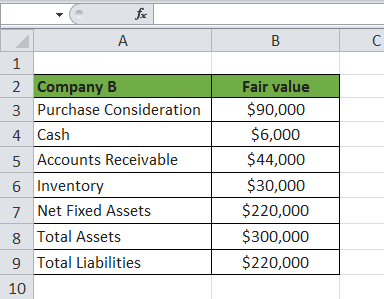

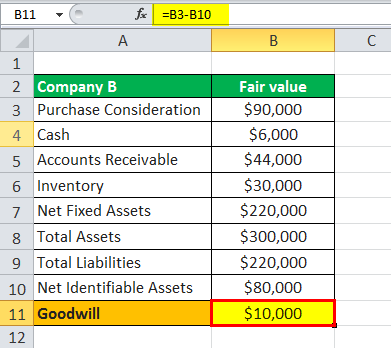

Let us take another example of Company A, which plans to acquire Company B. The acquisition consideration is agreed at $90,000. The following information is available concerning the Company.

Given,

- Consideration paid = $90,000

- Fair value of non-controlling interests = $0

- The fair value of equity previous interests = $0

Below given table shows data for calculation of goodwill of Company A

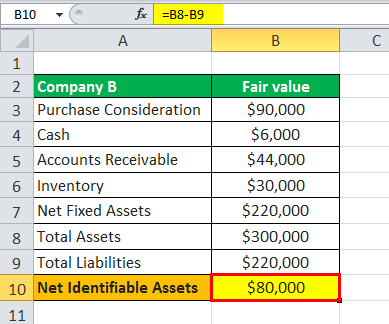

Therefore, Net Identifiable Assets of Company A can be calculated as,

Net Identifiable Assets = Fair value of identifiable assets – Fair value of identifiable liabilities

= $300,000 – $220,000

Net Identifiable Assets = $80,000

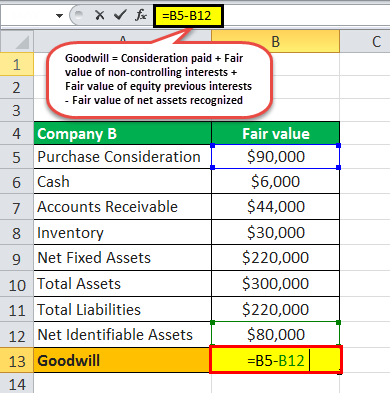

Therefore, the calculation of Goodwill will be as follows,

Goodwill = Consideration paid + Fair value of non-controlling interests + Fair value of equity previous interests – Fair value of net assets recognized

Goodwill calculation = $90,000 + $0 + $0 – $80,000

= $10,000

Therefore, the goodwill generated in the transaction is $10,000

Relevance and Uses of Goodwill Formula

It is very important to understand the concept of goodwill because it is the metric that encapsulates the value of a company’s reputation built over a significant period. The different factors aiding the goodwill include (not exhaustive) the company’s brand name, extensive customer base, good customer relations, any proprietary patents or technology, and excellent employee relations.

This brand value ensures that future profits can be expected to be over and above normal profits. Nevertheless, goodwill is an intangible asset that can neither be seen nor be felt, although it exists in reality and can be purchased and sold. In case of a distress sale i.e., when a company is acquired for less than its tangible net worth, the target company is said to have ‘negative goodwill.’ The appropriate pricing for goodwill is extremely difficult, but it does make a commercial enterprise more valuable.

Under IFRS and US GAAP standards, goodwill is considered as an intangible asset with an indefinite life, and as such, there is no requirement to amortize the value. However, it should be evaluated every year for impairment loss. Most companies prefer to amortize goodwill over 10 years.

Recommended Articles

This article has been a guide to Goodwill Formula. Here we discuss the Goodwill Calculation Method using practical examples and downloadable excel templates. You may learn more about Financial Analysis from the following articles –