Part of our Fixed Assets and Depreciation guide

What is Straight Line Amortization?

Straight-line amortization is one of the methods used for the amortization of the cost of the intangible assets or allocating the interest expenses which are associated with the issue of the bond by the company equally in each of the accounting period of the company until the end of the life of the intangible asset or until maturity of bond respectively in the income statement of the company.

Types of Straight-Line Amortization

The following are the main situation in case of which the method of Straight Line Amortization is used:

#1 – Allocation of the Interest on the Bonds

Under this situation, the company allocates the interest on the bond issued by it equally over the asset’s life. This interest arises when the company issues the bonds at a discount, but the interest is payable on the face value. So, the company must amortize the bond discount given, i.e., the difference between the face value and the value received over the remaining period of maturity of the bond.

#2 – Charging off Cost of Intangible Asset

Under this method, the cost of intangible assets such as patents, goodwill or intellectual property, etc., is charged over the useful life of that intangible asset in equal yearly amounts.

#3 – Monthly Installment of Loan

When the loan is to be repaid in equal installment, it is also referred to as Straight-line amortization.

Straight Line Amortization Formula

The formula for the calculation of the Straight Line Amortization is as follows:

#1 – Allocation of the Interest on the Bonds

Where,

- Total Interest amount = difference between the face value and the value received over the remaining period of maturity of the bond

- The number of periods in the life of Bond= Remaining period of the bond until maturity.

#2 – Charging off Cost of Intangible Asset

Where,

- Cost of the intangible assets= amount paid for the intangible asset minus the salvage value of that intangible asset.

- The useful life of the intangible assets = number of years of Useful remaining life remaining of that intangible asset;

Examples

Example #1 – Allocation of the Interest on the Bonds

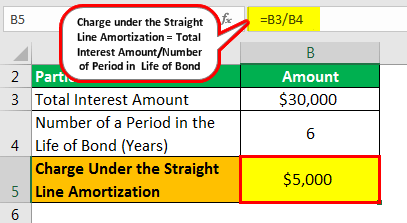

For Example, Company A ltd. issued the 1000 bonds in the market having a face value of $1,000 each at $970 each. The period for which the bond is issued in the market is six years. Calculate the charge of interest every year in the company’s income statement using the Straight Line method.

Solution

In the present case, the face value of each of the bonds issued is $1,000, and the issue price is $ 970. So the discount issued per bond comes to $30 ($1,000- $970). So the total discount given for all the bonds comes to $30,000 (discount per bond * number of bonds issued = $30* 1,000).

A company needs to amortize this discount because a discount arises when the company issues the bonds at a value less than its face value. Still, the interest is payable on the face value and not on the discounted issue price. Now, by using a method of the straight line, bond discount will be written off by the company in the equal amounts over a bond’s life as follows:

- Total Interest Amount = $ 30,000

- Number of a Period in the life of Bond = 6 years

Calculation of Straight-Line Amortization

- = $ 30,000 / 6

- = $5,000

Thus every year, $5,000 will be charged to the company’s income statement for the next six years.

Example #2 – Charging off the Cost of Intangible Asset

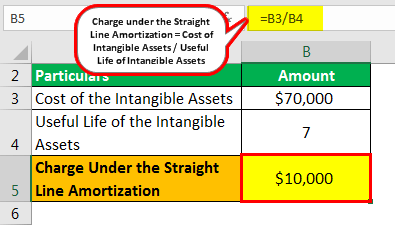

For Example, Company A ltd buys goodwill for $70,000, having an estimated useful life of seven years with no salvage value at the end. Calculate the yearly charge using the straight-line amortization method.

Solution

- Cost of the intangible assets=$ 70,000.

- The useful life of the intangible assets= 7 years

Calculation of Straight-Line Amortization

- = $ 70,000 / 7

- = $10,000

Thus every year, $10,000 will be charged in the income statement of the company for the next seven years.

Advantages

The different advantages are as follows:

- It is a simple and less time-consuming method as every year; an equal amount is to be charged to the income statement of the company.

- The straight-line amortization method is one of the very useful accounting principles because using this, the expenses or interest is calculated quickly.

Disadvantages

The different disadvantages are as follows:

- Generally, all the intangible assets do not perform each year uniformly, so the Straight-line amortization method does not account for these variations.

- In cases where functional life span cannot be estimated properly, this method will not be useful.

Important Points

The different important points are as follows:

- Estimating the functional lifespan or the maturity of intangible assets or bonds and loans is required.

- It systematically leads to the same amount movement in every accounting period from the balance sheet account of the company to the income statement account.

Conclusion

Straight-line amortization equally charges the cost of assets or interest in each of the company’s accounting periods until the end of the life of the intangible asset or until the maturity of the bond, respectively, in the company’s income statement.

It is a simple and less time-consuming method as every year; an equal amount is to be charged to the company’s income statement. However, in cases where functional life span cannot be estimated properly, this method will not be useful.

Recommended Articles

This article is a guide to Straight-Line Amortization. Here we discuss the types, formula for calculating straight-line amortization, and examples, advantages, and disadvantages. You can learn more about accounting from the following articles-