What is Attribute Sampling?

Attribute sampling refers to a statistical sampling tool used by the auditors to analyze the features of a particular population and determine whether the internal controls placed by the management are working effectively or not. In this sampling, a particular activity is chosen as a sample and internal controls for the same are tested.

Explanation

An audit is a time-consuming process, and it is not possible for the auditors to conduct a test for 100% transactions. It is due to this reason that sampling tools are used by the auditors. One such sampling process is attribute sampling in which the audit chooses a particular control area and applies sampling to check the attributes of the control area so as to ensure whether controls placed are working efficiently or not. Once a process is chosen, the same is checked for the accuracy of internal controls.

How Does it Work?

In attribute sampling, an item is taken as a testing base, and the aim to verify whether the same possess certain features or not. For verifying the same, the auditor carries out a test on a particular number of records and determine how many times a given feature shows up in the population. The auditor thus determines out of the selected population how many records contain an error. This gives the percentage of population error. The auditors also have determined in advance, the tolerance limit within with errors is to be ignored. Based on the tolerance limit, the auditor decides whether the item selected has proper internal controls or not.

As stated above, the purpose is to test the effectiveness of internal controls in a business.

If you want to learn more about Auditing, you may also consider taking courses offered by Coursera –

Examples of Attribute Sampling

Suppose, as per the internal controls laid by the management of the company, the expense invoices exceeding $100 are to be supported by purchase order. The auditor here will check whether the invoices are backed by purchase order or not i.e., purchase order is the attribute which is tested by the order. The auditor selects 100 invoices as the sample.

Now, after verifying, the auditor finds that four invoices aren’t supported by purchase order. In this case, population error comes out to be 4%. There are some other details that you need to consider:

- Tolerable error rate: 7%

- Sampling risk: 2%

- Expected Deviation Rate: 5%

Now, Rate of upper deviation = Population error + Sampling risk = 4% + 2% = 6%

Here, sampling risk is the risk that the sample might not reflect the characteristics of the total population. The risk, in this case, if of 2%. This also means that the confidence level is 98% since the auditor believes that out of 100 records, two records will not reflect the attributes of the population.

Rate of upper deviation < Tolerable error rate.

Here, the auditor will be satisfied since the rate of upper deviation falls within the tolerable error rate of 7%.

Attribute Sampling Table

| Particulars | Description | Values |

|---|---|---|

| Confidence Level | 98% | |

| In the above example, the auditor believes that the sampling risk is 2%. Thus, the confidence level is 98% (100%-2%). | ||

| Expected Deviation Rate | 5% | |

| This rate represents the auditor’s estimate of the actual error in the population. | ||

| Tolerable Error Rate | 7% | |

| This represents the maximum limit within which the non-compliance in the internal control can be accepted. | ||

| Rate of Upper Deviation | 6% | |

| This is calculated as the sum of actual population error and sampling risk. It represents the actual rate of deviation from the internal controls. The auditor compares this against the tolerable error rate and makes audit conclusions. |

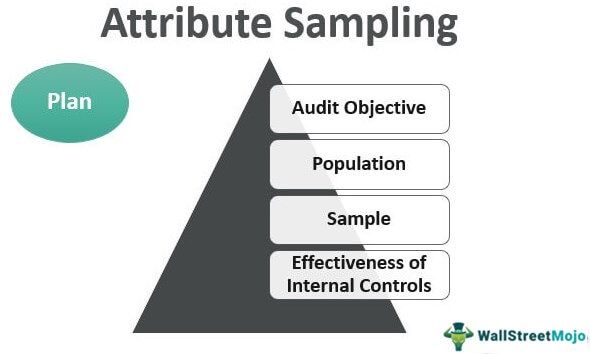

Attribute Sampling Plan

An attribute sampling plan refers to the plan that the auditor develops for testing the effectiveness of internal controls in an organization. The results of the exercise help an auditor to decide whether the controls are functioning properly or not i.e., whether there is compliance or non-compliance.

The auditor defines the audit objective, population, sample, and control item that is being checked.

Uses

The auditors use attribute sampling for testing the internal controls in an organization. Based on this, the auditor is able to conclude the compliance or non-compliance of internal controls. It is important the internal controls laid down by the management are working effectively, and the same forms an important part of the audit process.

Advantages

- It helps an auditor to test the presence and working of internal controls.

- The deficiencies found in the internal controls are communicated to the management, which can take steps for the improvement in the controls.

Disadvantages

- The process of attribute sampling also incurs the limitation of sampling that the sample may not be representing the entire population. If the estimate of the sampling risk is not correct, it may affect the results.

- It doesn’t give any quantitative conclusion.

Recommended Articles

This has been a guide to what is Attribute Sampling in Audit. Here we discuss how does it work along with examples, advantages, and disadvantages. You may learn more about financing from the following articles –