What are Audit Assertions?

Audit assertions are the inherent claims made by the company’s management concerning the recognition and presentation of the different elements of the company’s financial statements, which are used for the audit of those financial statements.

They involve procedures usually used by the auditors to test a company’s guidelines, policies, internal controls, and financial reporting processes. These assertions are the explicit or implicit representations and claims made by the management of a company during the preparation of their company’s financial statements.

The audit assertions are primarily regarding the correctness of the different elements of the financial statements and a company’s disclosures. Audit Assertions are also referred to as Financial Statement Assertions and Management Assertions.

Different Categories of Assertions

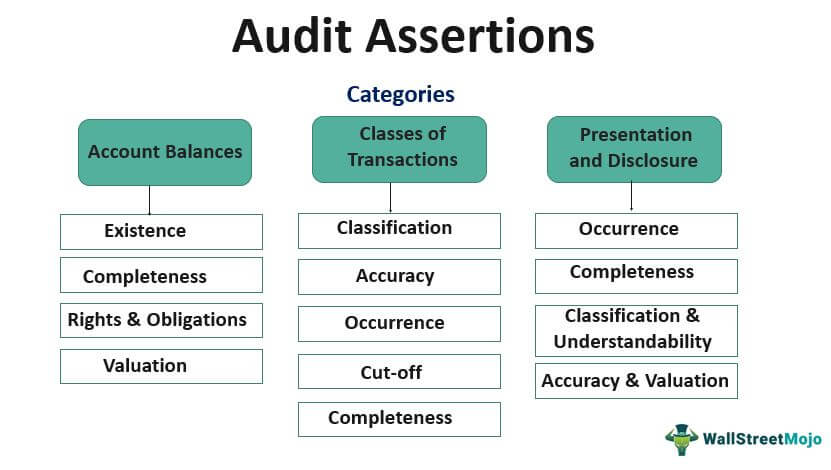

Audit assertions can be broadly listed into three general categories, which are listed below:

- Account Balances – These assertions are generally about the end-of-period balance sheet accounts such as assets, liabilities, and equity balances.

- Classes of Transactions – Income statement accounts usually use these assertions.

- Presentation and Disclosure – These assertions deal with presenting and disclosing different accounts in the financial statements.

If you want to learn more about Auditing, you may also consider taking courses offered by Coursera –

List of Audit Assertions Related to Account Balances

#1 – Existence

It refers to the fact that the assets, liabilities, and equity balances mentioned in the books exist at the end of the accounting period. This assertion is critical for the asset accounts because it reflects the strength of the company.

#2 – Completeness

It refers to the fact that the assets, liabilities, and equity balances, which need to be recognized, have been recorded in financial statements. You need to note that leaving out any of the aspects of an account can lead to a false representation of the company’s financial health.

#3 – Rights & Obligations

It pertains to the confirmation that the entity has the right to ownership of the assets and obligations for the liabilities recorded in the financial statements.

#4 – Valuation

Valuation of the balance sheet items must be correct as overvalued or undervalued accounts will result in a false representation of the financial facts. This type of assertion is related to the proper valuation of the assets, the liabilities, and the equity balances. You must perform the valuation properly to reflect an accurate and fair position of the company’s financial position.

List of Audit Assertions Related to Classes of Transactions

#1 – Occurrence

It refers to all the transactions recorded in the financial statements that are related to the stated entity.

#2 – Completeness

It is about the fact that all the transactions which were supposed to be recognized have been recorded in the financial statements entirely and comprehensively.

#3 – Accuracy

It refers to the fact that all the transactions have been recognized accurately at their correct amounts. For instance, any adjustments required have been correctly reconciled and accounted for in the statements.

#4 – Cut-off

It refers to all the transactions that have been recorded in the appropriate accounting period. Transactions like prepaid and accrued expenses must be recognized correctly in the financial statements.

#5 – Classification

This type of assertion confirms that all the transactions have been classified and presented properly in the financial statements.

List of Audit Assertions Related to Presentation and Disclosure

#1 – Occurrence

It refers to the presentation of all the transactions and the disclosure of all the events in the financial statements and confirms that they have occurred and are related to the entity.

#2 – Completeness

It is about all transactions, events, balances, and other matters that should be disclosed in the financial statements and confirms their appropriate disclosure.

#3 – Classification & Understandability

This type is related to the comprehensiveness of the disclosed events, balances, transactions, and other financial matters. It confirms that all have been classified correctly and presented clearly in such a manner that helps understand the information contained in the financial statements.

#4 – Accuracy & Valuation

This assertion confirms that the transactions, balances, events, and other similar financial matters have been correctly disclosed at their appropriate amounts.

Relevance and Uses of Audit Assertions

Understanding the audit assertions is very important from an investor’s viewpoint because almost every financial metric used to evaluate a company’s stock is verified through these assertions. The audit assertions are carried out to verify the financial figures computed using data from the company’s financial statements. If the figures are inaccurate, that will result in a misrepresentation of the financial metrics, including the price-to-book value ratio (P/B) or earnings per share (EPS).

These are a few of the financial metrics which analysts and investors commonly use to evaluate the company stocks. During an audit of a company’s financial statements, the main idea of an auditor is to check and confirm the reliability of the facts and the figures recognized in the financial statements and capture the facts truly and fairly in the audit assertions.

Recommended Articles

This article has been a guide to what is Audit Assertions and their definition. Here we discuss the list of audit assertions and their categories (Account balances, classes of transactions, presentation, and disclosure). You may learn more about our articles below on accounting –