Interim Audit Meaning

Interim audit refers to the examination of books of accounts to check the recording of transactions correctly and the company’s work in the manner legally acceptable before the conduct of any statutory audit. It is an audit conducted between two financial years, and its main objective is early identification of threats and taking corrective measures at an early stage.

Key Takeaways

- An interim audit s an audit conducted during the fiscal year rather than at the end of the year. This audit aims to review the company’s financial statements and internal controls to provide assurance on the financial information.

- Interim audits are carried out to ensure that the proper controls are in place to avoid fraud and help find any significant misstatements in the financial statements.

- A company’s financial status can be evaluated, problem areas can be found, and interim audits can provide suggestions for future audits.

Objectives of Interim Audit

- It is conducted to determine the profit of the period and determine whether the company could pay an interim dividend or not, as interim dividend payment by the company results in the value addition of the business in the mind of investors and shareholders.

- To identify and early detection of fraud and improve the employees’ efficiency as it thoroughly examines the work done by the employees.

Characteristics

- It is conducted between two periods; it sometimes may also be called a half-yearly audit.

- It is an in-depth analysis of all the transactions entered into or transacted with the business over a defined period.

- It is sometimes conducted to determine the book value of a company’s share.

- The organization whose interim audit is conducted is considered more reliable than those whose interim audit is not conducted.

If you want to learn more about Auditing, you may also consider taking courses offered by Coursera –

The procedure of Interim Audit

The procedure of internal audit varies from business to business and depends on the working of the business enterprise and the voluminous transactions; some of the essential outlay points are as follows:

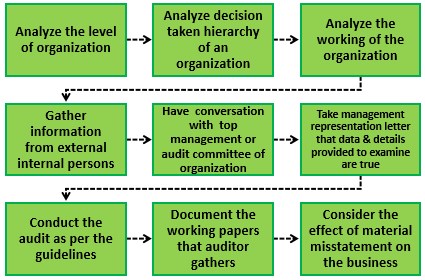

- Analyze the level of organization.

- Analyze the decision taken hierarchy of an organization.

- Analyze the organization’s work and the industry in which the entity operates.

- Gather information from the external and internal persons about the business.

- Have a conversation with the top management or the organization’s audit committee.

- After that, take the management representation letter that the data and details provided to examine are true and full in all aspects.

- Conduct the audit as per the guidelines lay upon by the auditing standards committee.

- Document the working papers that the auditor gathers while conducting the audit.

- If they are materially misstated, consider the effect of material misstatement on the business, then issue a qualified audit report or vice versa.

Applications

- The concept is used to determine the amount of dividend that the management is planning to declare as a part of profits earned by the company.

- To check where there is robust internal control of the management on the business activities and on which the administration and the external auditor could rely upon it.

Benefits

- It helps increase the efficiency and effectiveness of the management functioning concerning the accounting and financial part of the business.

- It is less expensive than other audits that are required to be conducted, and it helps in the easy finalization of final accounts.

- As the employees are well aware that some other person checks their work, the efficiency and correctness in employees’ work tend to rise.

- As the books of accounts are finalized on the date by the professional possessing the necessary skills, the company may easily borrow funds from the financial institutions based on the same.

- As the books of accounts prepared are to be analyzed in-depth, the risk of fraud will significantly fall.

Limitations

- It is only to be used by management, and it does not have any connection with investors or lenders, etc.

- It only covers the financial part of the organization, but the business has several other aspects being reviewed for better results.

- It increases the burden and mental pressure on the working staff as their work is checked by some outside person.

- The risk of data manipulation rises to hide the things from being reported or detected.

- Sometimes due to errors in determining profits accurately to shareholders, the company’s funds may arbitrarily decrease.

Conclusion

‘Interim Audit’ is how the management itself checks whether they are complying with the regulatory requirements or not. This audit is the preliminary step to gathering information on the business conduct and considers an integral part of the statutory audit or final audit. Such an audit is conducted sometimes at the request of the business entrepreneur or sometimes on account of the ease of the work to be done by the statutory auditor at the time of the final audit. Sometimes some legal requirements need to be complied with and lay upon some entities to conduct an interim audit at the end of every quarter.

Frequently Asked Questions (FAQs)

Is interim audit compulsory?

No, an interim audit is not compulsory or required by the law. Instead, the frequency and timing of these audits are determined by the company’s internal policies, contractual obligations, or regulatory requirements.

How is an interim audit different from a final audit?

An interim audit is conducted at a specific time, usually between the end of the fiscal year and the date of the final audit. A final audit, on the other hand, is conducted at the end of the fiscal year and covers the entire financial year.

Who performs an interim audit?

Interim audits are typically performed by external auditors who the company hires to conduct the audit. The auditors may also work closely with the company’s internal audit team to ensure that all relevant information is considered during the audit process.

Recommended Articles

This article is a guide to the Interim Audit and its Meaning. We discuss interim audit objectives, characteristics, and procedures and their benefits and limitations. You can learn more about financing from the following articles –