What Are Audit Test of Controls?

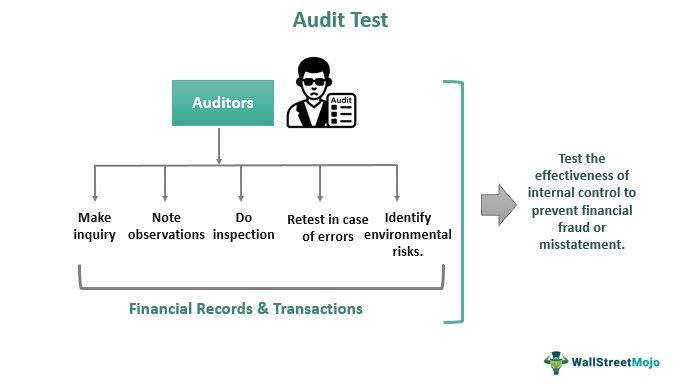

An audit test in terms is a set of control procedures or processes carried out by the auditors, being internal or external, which involves taking a sample of a group of similar transactions to gauge the accuracy and fairness with which the financial statements of an individual or an organization.

Such an audit is done before going ahead with the finalization of financial statements that will be presented to the stakeholders. This audit process helps to understand whether the company’s internal functions are strong enough to identify and prevent fraud related to the company’s financial data. In case of errors, the sample size is expanded.

- Audit test of control is the process where auditors examine and confirm the efficacy of a company’s controls to record its financial transactions.

- It tests the financial accounts and finds any errors, omissions, or significant inaccuracies. In case some error is detected, the sample size is increased to get more clarity.

- It focuses on the general ledgers’ ultimate balances, carried forward to the balance sheet, the company’s financial picture for the general public.

- A process used by auditors to determine the accuracy with which transactions are recorded by performing an audit test on a sample of a similar group of transactions.

Audit Test of Controls Explained

Audit test of control is the method of testing whether the financial reporting process is efficient enough to detect and avert any fraud. This will ensure the shareholders get a true and fair picture of the company’s financial condition. It is a procedure adopted by an auditor to test a sample of a similar group of transactions to conclude the fairness with which the transactions are recorded.

The main purpose of internal audit test of controls is to check and verify the level of effectiveness of controls followed by an organization while recording its financial transactions. It ensures that it tests and detects any error, omission, or material misstatements in the financial statements. Once an auditor carries out test of controls in audit, based on results, he may decide to further take some samples for testing or rely on clients’ internal controls. However, this audit process is extremely important for any organization, to reduce material misstatement risks and misuse of the same.

Types

Internal audit test of controls involves undertaking tests in five ways to arrive at a wholesome picture of the effectiveness of internal controls and whether there are any errors, omissions, or material misstatements while preparing the organization’s financial statements. The list given below will explain what are test of controls in auditing.

#1 – Risk Assessment

Undertaken to identify and understand risks, the company entails considering the environment within which it operates.

#2 – Test of Control

It aims to test the effectiveness of internal controls carried out by the company. The auditor undertakes a detailed examination of controls.

#3 – Substantive Test – Transactions

The main aim of this test is to identify whether any fraud, error, or material misstatement exists in the organization.

#4 – Substantive Test – Procedures

It is similar to the test discussed above; however, this one aims at evaluating the financial statements by carrying out a detailed study of the relationship of actually recorded amounts with the expected. It involves financial as well as non-financial data.

#5 – Test of Balances

It focuses on the end balances of the general ledgers, which are eventually carried forward to the balance sheet, which is the face of the company financials.

Example

Let take audit test of controls examples to understand the concept .

AM Inc., a US-based company, is engaged in manufacturing and producing certain antique pieces. Now, apart from this main objective, the company deals in accepting security deposits from various vendors, customers, and the common public for an interest in return.

For people from whom the company has accepted deposits in any year, the average ranges from 10,000 to 12,000 at any given time. During the audit, the auditor decides to undertake the audit of the security deposit on a sample basis and selects a sample of all deposit holders having a deposit of more than $10,000 at any given point in the year. Based on such a test, the auditor may give his opinion on the aspect of security deposits. Thus, from the audit test of controls examples, it is clear how the control system is monitored and tested for effectiveness.

Advantages

- It helps an audit select a few samples from a large group of transactions. Thus, it reduces the volume of work involved.

- Saves a lot of time;

- Eventually saves the workforce and labor employed.

- Saves on cost on account of lesser time involved and low workforce associated;

- From the auditors’ point of view, it will ensure more clients.

- Improves efficiency, as auditing similar voluminous transactions can be tiring.

- The testing sample will give comfort about the overall control over systems in an organization because of proper understanding about what are test of controls in auditing for the organization.

- Samples are selected randomly, and thus, there is no control by management board of directors accounting staff, or any other person. Thus they remain alert and careful while posting financial transactions at each stage.

- It can help the auditor assess the fairness of the preparation of the financial statements.

Disadvantages

- The audit test selects sample transactions for testing, and it is very well possible that any transaction about fraud may get left out.

- The auditor’s responsibility increases who has to be sure that the sample covers all the aspects of transactions being carried out by the organization, and should leave no stone unturned to check on any undetected errors or frauds.

- Audit Testing may work where the volume of transactions is very high. It will make no sense to follow audit testing from organizations operating on a small scale.

- It is possible that since the management, board, and accounting staff knows’ that audit shall be done using a sample testing method, they may remain careless in the hopes that any fraud or error may not get caught by the auditor.

- The auditor may leave complicated transactions out of its sample and only focus on simpler transactions to ease work.

- Risky in case there are no or weak internal controls.

Audit Test Of Control Vs Substantive Audit Procedure

Audit test of control states whether the internal procedure is strong enough to prevent of financial misstatement, whereas substantive audit is process where auditors identify financial misstatements. However, the differences between them are as follows:

| Audit test of control | Substantive Audit Procedure |

| It is a test of the controls to prevent financial misstatement. | It is the process of identifying financial misstatement. |

| It ensures that the financial record keeping system is effective in preventing fraud. | It ensure the company presents a true and fair picture of the company’s financial condition to shareholders. |

| It is designed to put a strong comtrol system to prevent fraud. | It is designed to make the accounting system accurate and valid. |

| Control system should be there before substantive audit. | Substantive audit is dependent on control system. |

Frequently Asked Questions (FAQs)

1. What kinds of audit tests are there?

Inquiry, observation, examination, re-performance, and computer-assisted audit techniques (CAAT), which entail testing massive amounts of data using computer algorithms, are the five test methods that auditors may utilize.

2. How is an audit test carried out?

The service organization uses five key approaches to go through and test each control that is in place. These techniques are ranked from least complex to most complex: investigation, observation, scrutiny of the evidence, repeat performance, and computer-assisted auditing (CAAT).

3. Why are audit tests crucial?

Audit testing’s primary goal is to examine and confirm the efficacy of a company’s controls to record its financial transactions. It tests the financial accounts and finds any errors, omissions, or significant inaccuracies.

Recommended Articles

This article has been a guide to what are Audit Test Of Controls. We explain if difference with substantive audit procedure, with examples, types and advantages. You can learn more about accounting from the following articles –