Table Of Contents

What Is Other Comprehensive Income?

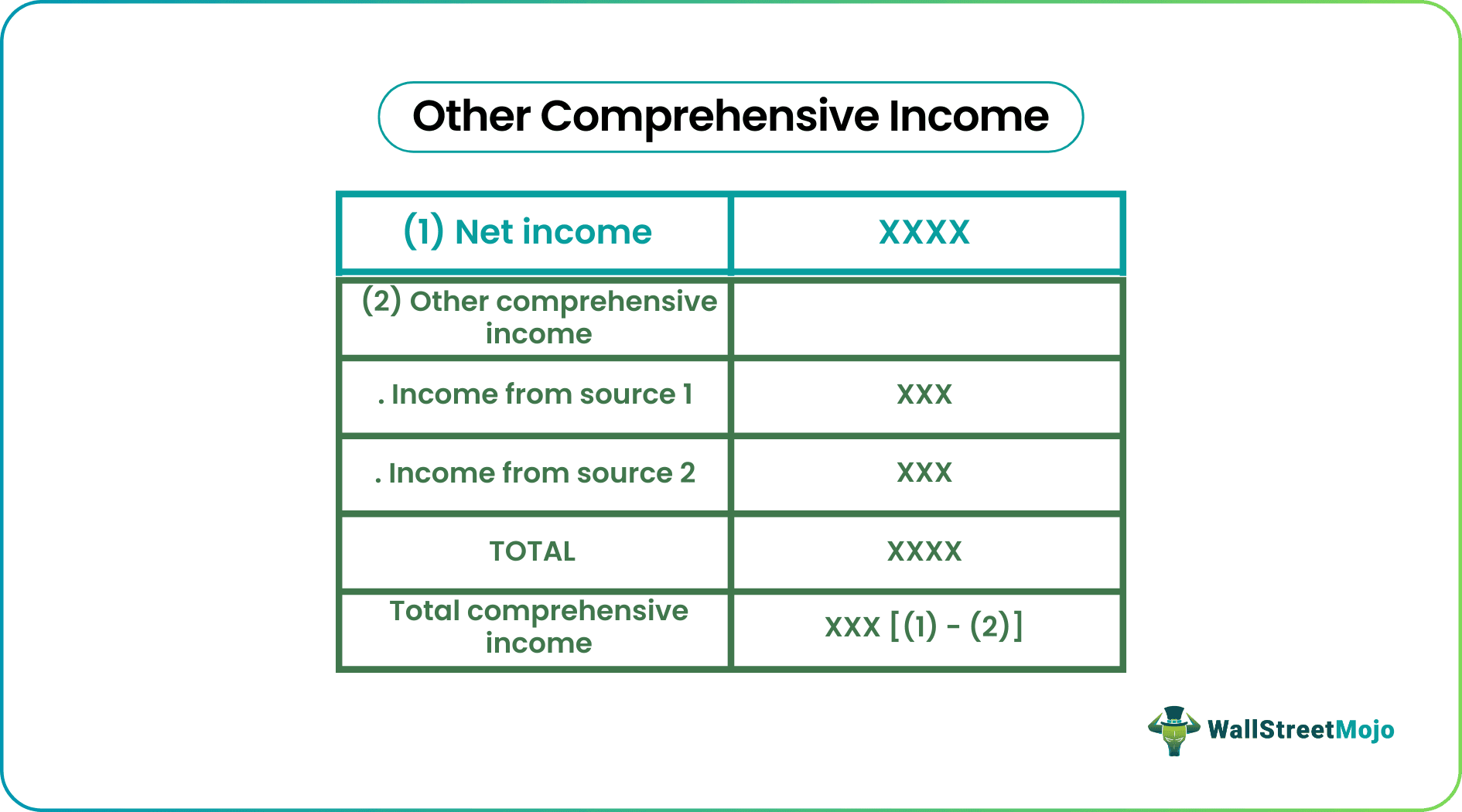

Other Comprehensive Income refers to that income, expenses, revenue, or loss in the company which has not been realized at the time of preparation of the financial statements of the company during an accounting period and are thus excluded from the net income and shown after the net income on the income statement of the company.

It consists of only those revenues, expenses, gains, and losses that have not been realized yet and hence is not included in the net income on the Profit & Loss statement. It is recorded on the liabilities side of the balance sheet under the Shareholders Equities head.

Table of contents

Other Comprehensive Income Explained

The other comprehensive income statement is the profit or loss that the business entity generates but are not shown in the profit and loss statement. They are reported in a separate part of the financial statement known as statement of comprehensive income.

They usually include items like the unrealized gain or loss from available -for-sale securities. Such type of securities are held by the entity but are not actively traded and are reported until they are sold by the company. They also include the foreign currency translation adjustment in which the company translates the financial statements of its branches operating in different countries into the home currency and report the gains or losses.

Companies sometimes hedge their finances from inflation or changes in interest rates by using derivative contacts. Any gain or loss from such hedging are reported as other comprehensive income. Even plant or property revaluation resulting in gain or loss is reported and this kind of income. This income provides an overview of the financial condition of the entity and help investors and analysts take investment decisions based on risk assessment and uncertainties. It does not affect the earnings per share of the company because it is not a part of the net income.

Statement of Comprehensive Income Explained in Video

Components

Given below are the main components of other comprehensive income.

How Is Other Comprehensive Income Reported?

As per the accounting standards, this income is recorded under shareholder’s equity on the liability side of the balance sheet.

source: Facebook SEC Filings

- A company may purchase equipment, machinery, or property while conducting business operations. While accounting for the same, the company is required to determine the carrying amount of the asset, which essentially means that the accumulated depreciation and the accumulated impairment loss has to be deducted from the acquisition cost of the asset. The revalued cost hence attained, is the fair value of the asset as on the specific date. The unrealized gain or loss on revaluation is included. For example, if the carrying amount of the asset increases due to the revaluation, the increase will be recorded as other comprehensive income on the liabilities side in the Equity under the Revaluation surplus category.

- As mentioned earlier, only unrealized items can be categorized as other comprehensive income. However, the asset may be realized at a later date. It means that the company may decide to sell the asset in the subsequent years. In that scenario, the realized gain or loss associated with the asset gets removed from this category and is recorded in the income statement.

- It is also essential to state that the components of other comprehensive income may be reported either net of related tax effects or before related tax effects with a single aggregate income tax expense.

Examples

Let us look at some other comprehensive income examples to understand the concept better.

Example #1

The XYZ Ltd. purchased equipment for Rs.35,65,000 on 10th July 2017. The company decided to undertake the revaluation process for the equipment on 30th September 2017. Revaluation is when the company brings the fixed market value of the fixed asset into the books of accounts. The revaluation of the equipment took place at Rs.40,85,000.

Record: The difference of Rs.5,20,000 will be shown as a component of the other comprehensive income in the Balance sheet under Equity in Revaluation surplus.

On 31st October 2018, the company decided to again revalue the asset. The revalued amount was Rs.25,10,000. The decrease in the amount of Rs.10,55,000 will be recorded as:

Record: The amount of Rs.5,20,000, which was recorded in the balance sheet, will be reduced from the revaluation surplus, and Rs.5,35,000 will be shown in the income statement.

Example #2

Company ABC Ltd. has recorded the following -

Thus the above are some useful other comprehensive income examples.

Importance

We need to look at not only the realized gains and losses listed in the income statement but also note the unrealized income and losses mentioned as other comprehensive income accounting. Some of the other factors that highlight its relevance are as follows:

#1 - Accounting for the Pension Plans

A pension or post-retirement benefit plan related adjustments are an essential part of the other comprehensive income. An individual can study the impact of the pension and corporate retirement plans. For example, an employer would plan for pension payment to employees who retire later. If the assets required for the plan are not adequate, the pension plan liability of the firm will increase. The company needs to plan accordingly.

#2 - Understand the Unrealized Gains and Losses from Bonds and Shares

An analyst can understand the unrealized gains and losses on bonds and shares while going through the components of the other comprehensive income. For example, if a share has been purchased at $50 and the fair market value is $70, the unrealized gain is $20. An analyst can understand the fair value of a company's investments by reading about the other comprehensive income components. We must also learn about the unrealized gains or losses on the investments categorized as available for sale by the firm.

#3 - Accounting for Foreign Currency Exchange Gains or Losses Adjustments

A company may hedge against the fluctuations in the currencies while transacting business activities. The analyst will understand the impact of fluctuations in the currency rate and foreign currency exchange gains or losses adjustments made in the process.

Other Comprehensive Income Vs Comprehensive Income

Even though they may sound similar the two concepts given above has a distinct difference as detailed below:

- The former includes those type of income that do not form a part of the net income whereas the latter is a part of the net income.

- The former includes only the gain or loss from foreign currency translation or available-for-sale securities but the latter include these and additionally the items of net income.

- Comprehensive income is the overall company equity change whereas the other complete income accounting is not.

Recommended Articles

This article has guided to what is Other Comprehensive Income. We explain it with example, its various components and how it is reported. You can learn more about accounting from the following articles –