Written byHarsh KataraHarsh KataraFreelance WriterHarsh, an associate at JP Morgan and Chase in Corporate Finance, blends expertise in equity research, financial modeling, and accounting. Chartered Accountant and CFA Level III holder with versatile ERP experience. At WallStreetMojo, Harsh works as Freelance Writer.Chartered Accountant, CFA Level III holderFinanceView Full Profile

Reviewed byDheeraj Vaidya, CFA, FRMDheeraj Vaidya, CFA, FRMContent Reviewer & Course DirectorDheeraj is a former J.P. Morgan and CLSA Equity Analyst with nearly two decades of experience in financial modeling, valuation, equity research, and corporate finance. He specializes in helping students and professionals develop practical and in-demand finance skills through structured and AI-powered,20+ Years of experienceCFA, FRM, IIT Delhi, IIM LucknowFinancial ModelingView Full Profile

Change in the net working capital is the difference between available funds and outstanding payments of the company in an accounting period when compared with other accounting periods, which is calculated to make sure that sufficient working capital is maintained by the company in every accounting period so that there should not be any shortage or underutilization of funds.

The essence of the concept is that if a company has a positive working capital, it means they have funds in surplus. The inverse of having a negative working capital indicates that the company owes more than it has in its cash flow. It acts as the company’s metric for liquidity.

Change in net working capital refers to the difference in a company’s net working capital between two accounting periods.

It is assessed to ensure that the company has sufficient working capital to sustain its operations in the future.

If the increase in current assets and liabilities is proportional, then there will be no change in net working capital.

A positive net working capital change occurs when current liabilities increase more than current assets, while a negative net working capital change occurs when current assets increase more than current liabilities.

Change in Net Working Capital Explained

Change in net working capital refers to the differences in the liquidity of the company. As in, it is a measure of if the company will be able to pay off its current liabilities with the assets in hand.

If the Net Working capital increases, we can conclude that the company’s liquidity is increasing. It could indicate that the company can utilize its existing resources better. Some companies have negative working capital, and some have positive, as we have seen in the above two examples of Microsoft and Walmart. Generally, companies like Walmart, which have to maintain a large inventory, have negative working capital.

Software companies generally tend to have a positive change in working capital cash flow because they do not have to maintain an inventory before selling the product. It means that it can generate revenue without increasing current liabilities. Cash flow cannot increase with only a change in working capital. But if it is not sufficient, the company’s efficiency is greatly reduced.

If the current assets and current liabilities have increased by the same amount, there would be no change in net working capital.

If the change is positive, then the change in current liabilities has increased more than the current assets.

If the change is negative, the change in the current assets has increased more than the current liabilities.

Changes in Net Working Capital in Video

Formula

Let us understand the formula that shall act as a basis for us to understand the intricacies of the concept and its related factors.

Changes in Net Working Capital = Working Capital (Current Year) – Working Capital (Previous Year)

Or

Change in a Net Working Capital = Change in Current Assets – Change in Current Liabilities.

How to Calculate?

Now that we understand the basics and the formula of the concept, let us understand how to calculate the changes in net working capital cash flow through the step-by-step explanation below.

Find the Current Assets for the current year and previous year.

From the point of the current asset of view, we consider the below:InventoryAccounts ReceivablePrepaid Expenses

Find the Current Liability for the Current Year and Previous Year.

From the current liabilities, we consider the below:Accounts PayableAccrued ExpensesInterest PayableDeferred Revenue

Find Working Capital for the Current Year and Previous Year

Working Capital (Current Year) = Current Assets (current year) – Current Liabilities (current year)Working Capital (Current Year) = Current Assets (current year) – Current Liabilities (current year)

Calculate Changes in Net Working Capital using the formula below:

Changes in Net Working Capital Formula = Working Capital (Current Year) – Working Capital (Previous Year);

Calculation (Colgate)

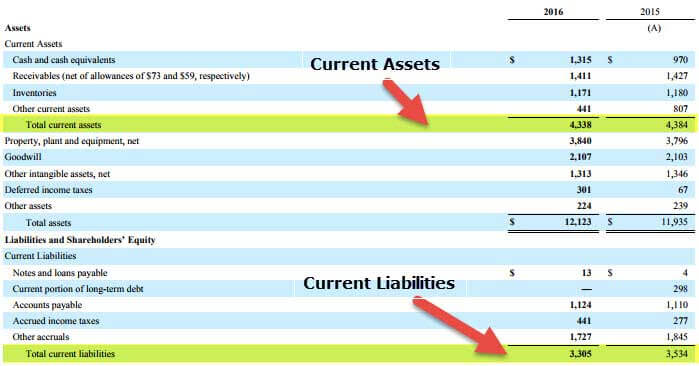

Below is the Snapshot of Colgate’s 2016 and 2015 balance sheets. This example shall give us a practical outlook of the concept and its ebbs and flows.

Let us calculate the Working Capital for Colgate.

Working Capital (2016)

Current Assets (2016) = 4,338

Current Liabilities (2016) = 3,305

Working Capital (2016) = 4,338 – 3,305 = $ 1,033 million

Working Capital (2015)

Current Assets (2015) = 4,384

Current Liabilities (2015) = 3,534

Working Capital (2015) = 4,384 – 3,534 = $850 million

Net change in Working Capital = 1033 – 850 = $183 million (cash outflow)

Analysis

Change in Working capital cash flow means an actual change in value year over year, i.e., the change in current assets minus the change in current liabilities. With the change in value, we will understand why the working capital has increased or decreased.

Below are a number of actions that will cause a change in Net Working capital:

If the company does not allow outstanding credit, the account receivables will get reduced. But sales may have a declining effect. Below are several actions that will cause a change in Net Working capital:

Inventory planning also impacts the change in working capital. An increase in inventory increases the usage of cash.

Stretching accounts payable impacts the change in working capital.

If the company’s growth rate is high, it uses the cash more to buy inventories and increase account receivables. Cash will be heavily used for it then.

It is an indicator of operating cash flow, and it is recorded on the statement of cash flows. And the cash flow is one of the important factors to be considered when we value a company. It indicates whether the short-term assets increase or decrease concerning the short-term liabilities from one year to the next.

Frequently Asked Questions (FAQs)

1. How does a change in net working capital impact a company’s financial health?

Changes in net working capital can have significant implications for a company’s financial health. For example, if a company experiences a positive change, it may have more funds to invest in growth opportunities, repay debt, or distribute to shareholders. Conversely, a negative change may signal that a company struggles to meet its short-term obligations.

2. How does a company’s growth rate affect its change in net working capital requirements?

A company’s growth rate can affect its change in net working capital requirements. As the company grows, it may need to invest more in its working capital to support increased production or inventory levels, resulting in a higher net working capital requirement. Conversely, if a company is not growing, it may not need as much working capital and may experience a decrease in net working capital requirements.

3. What is the difference between gross working capital and change in net working capital?

Gross working capital refers to the total current assets a company has on hand to conduct its business operations, such as cash, inventory, and accounts receivable. On the other hand, the change in net working capital measures the change in a company’s working capital over a period.

Recommended Articles

This has been a guide to what is Changes in Net Working Capital. Here we explain its meaning, formula, and how to calculate along with examples. You may also have a look at the related articles: