Part of our Efficiency Ratios guide

What Are Days Working Capital?

Days working capital is a vital ratio considered for fundamental analysis of the company, which indicates the number of days (lower the better) a company requires to convert its working capital into sales revenue. One may derive it from working capital and the annual turnover.

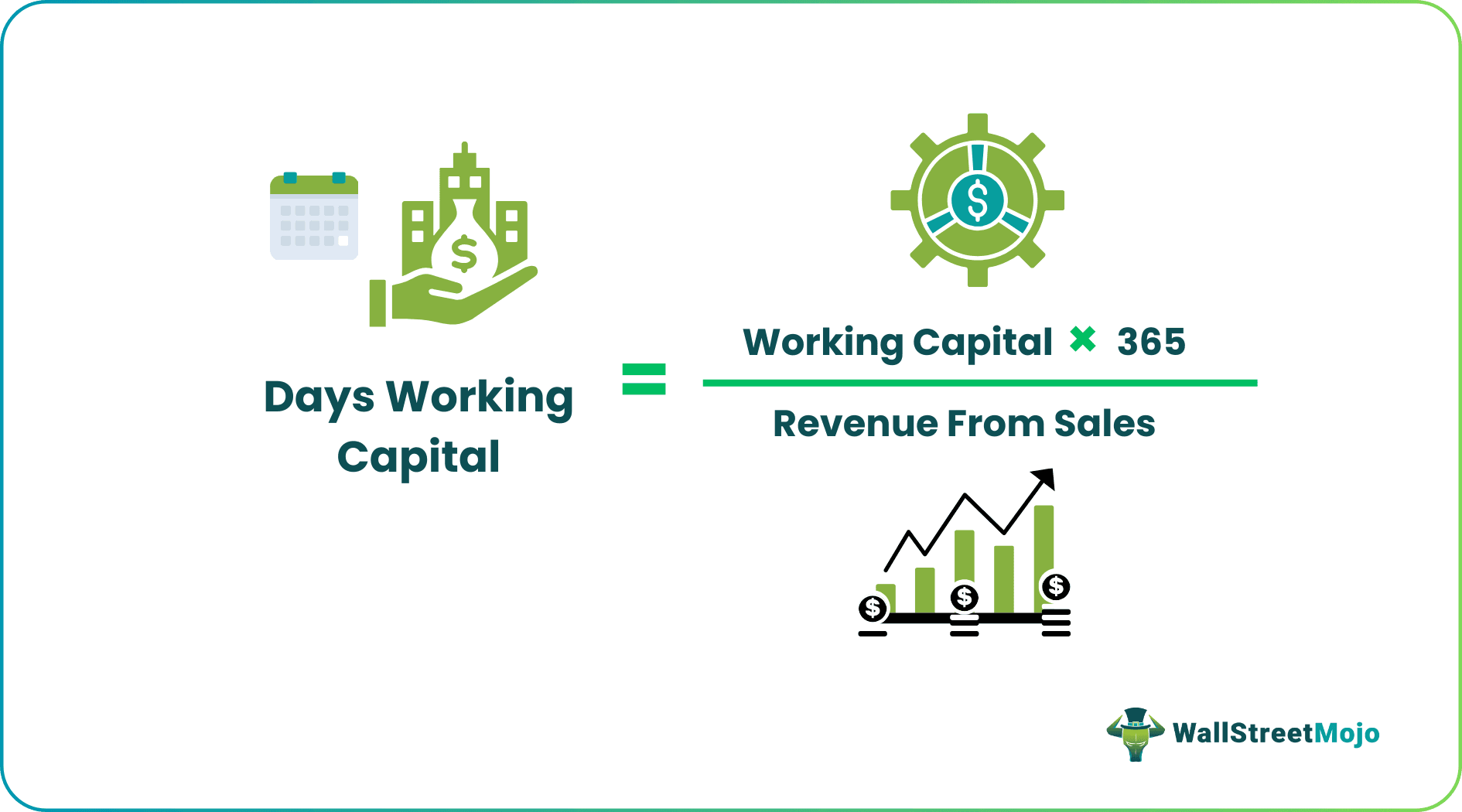

The formula is as follows:-

Days Working Capital Formula = (Working Capital * 365) / Revenue from Sales.

Key Takeaways

- The day’s working capital is essential in evaluating a company’s performance. It shows how many days, ideally fewer, a company needs to turn its working capital into revenue.

- The time to earn back investments in working capital through sales revenue is a crucial measure of operational efficiency. It indicates strong fund management and helps analysts assess company health.

- It would help if one considered all its assets and liabilities to predict a company’s direction. Relying on only a few indicators could be misleading.

Important Definitions

- Working Capital: The difference between the company’s current assets and current liabilities of the company is known as working capital. The formula for working capital is as follows: –

Working Capital = Current Assets – Current Liabilities

- Current Assets: Assets that could be realized, used, or extinguished in a normal operating cycle are considered current assets. e.g., inventories, cash and cash equivalents, trade receivables, prepaid expenses, etc.

- Current Liabilities: The liabilities due for payment in one operating cycle are known as current liabilities — e.g., trade payable, outstanding expenses, bills payables, etc.

- Operating Cycle: The operating cycle is the time an entity requires to reach the initial stage of purchasing raw materials to realize the cash from the trade receivables. The operating cycle varies from company to company and considers lower as the company is quite efficient in achieving the cash invested in working capital. It is also known as the cash conversion cycle.

- Average Working Capital: If we are considering a longer span for working capital, it is better to take the average of working capital to remove the unevenness in the posted figures, if any. Let us say we are considering the ratio for a year. Hence, we could take the average working capital on the opening and closing dates of the year. Also, we could take quarters instead of opening and closing dates for our calculations.

- Operating Working Capital: Operating working capital denotes the subtraction of operating liabilities from the operating assets. Those current assets and liabilities that are used or directly contribute to the company’s operations are known as operating assets and liabilities.

The formula for operating working capital is as follows:

Operating Working Capital = (Operating Current Assets – Operating Current Liabilities)

Examples of operating items are fixed assets; plant, and machinery (involved in the production), inventories, trade payables and receivables, cash blocked for operating purposes, etc. Cash earmarked for investments, marketable securities, and other such assets or liabilities would not be considered for calculating operating working capital. Examples of operating items are fixed assets; plant and machinery (involved in the production), inventories, trade payables, and receivables, cash blocked for operating purposes, etc. Cash earmarked for investments, marketable securities, and other such assets or liabilities would not be considered for calculating operating working capital.

If there is a substantial presence of non-operating assets or liabilities in some organizations, or bifurcation for non-operating amounts is readily available, one could use this method.

The following example assumes that other current assets and liabilities are non-operating. So, these are not considered for the calculation of operating working capital.

Calculate Working Capital Video

Days Working Capital Examples

Below are examples of days working capital.

Example #1

Let us take the annual numbers of Microsoft Corp. as of 30th June 2019 to calculate the days working capital. Revenue of $ 125,843 million, Current Assets, current liabilities of $175,552 million, and $69,420 million, respectively.

Solution:

Below is given data for the calculation of days working capital

- Revenue: $125,843

- Current Assets: $175,552

- Current Liabilities: $69,420

Calculation of Working Capital

Working Capital = Current Assets – Current Liabilities

- = $175552-$69420

- = $106132.

- =($106,132 * 365) / $125,843 million

- = 307.83 days.

It indicates the entity’s ability to convert the working capital to revenue in approximately 308.

Example #2

Let us take into consideration the following figures and calculate days working capital. Revenue for the particular period is $ 2,00,00,000. Take 360 days in your calculation.

Solution:

Below is the given data:-

Calculation of Net Working Capital

Calculation of Net Working Capital

- =$180000-$100000

- Net Working Capital = $80,000

Calculation of Days Working Capital

- =($80000*360)/$200000

- = 144 days

In the above example, as we can see, the working capital is 126 days, which denotes the company can recover its total invested working capital in 144 days.

Example #3

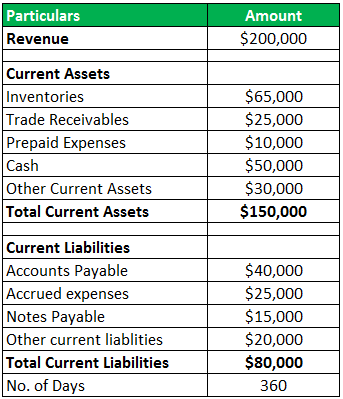

In the following example, we assume that other Current assets and liabilities are non-operating. Revenue for the particular period is $2,00,00,000. Take 360 days in your calculation. Calculate days and net operating working capital.

Solution:

Below is the given data:-

Calculation of Operating Working Capital

- =$150000-$80000

- Operating Working Capital = $70000

Calculation of Days Working Capital is as follows –

- =($70000*360)/$200000

- = 126 days

In the above example, as we can see, the working capital is 126 days, which denotes the company can recover its total invested working capital in 126 days.

Advantages

- It is a good indicator of the operational efficiency of the company. It entails the number of days the company would require to realize its initial investments in the working capital to realize the revenue from sales. So, if the resultant number is lower, it is considered better.

- This ratio helps the analysts consider the company with a better cycle of funds and the efficiency of the business’s operations.

Disadvantages

- If we consider the result an absolute number, the ratio does not clearly explain anything. Because the days’ working capital varies from company to company and industry to industry, it heavily depends upon the nature of the business. For example, a company with a trading business would have a much lower ratio than the businesses involved in the manufacturing process.

- It is also challenging to predict the correct direction of the company because it involves multiple variables in the numerator, such as various current assets and liabilities. To get the real picture, we need to dig deeper into the individual assets and liabilities items to measure their impact on the overall ratio. If we do not, one or two heavyweight indicators could manipulate the ratio and reflect the non-fair picture.

For instance, the ratio could be lower because of the following reasons: –

- Increase in the Revenue from Sales: It shows a better indication of increased sales ability to sell products.

- Delay in the Accounts Payable: It is also a good sign because this generally happens due to the reliable bargaining power of the entity and reflects a weakness on the part of the creditors.

- Inflated Cash or Accounts Receivables: Though in a cursory glance, this situation seems reasonable, the result is negative. Excess cash in the books denotes a lack of opportunity to invest funds in future ventures. Similarly, a growing accounts receivable also indicates the inability of the company to demand dues from the debtors. This situation generally stems from the lack of bargaining power and the presence of inferior or slow-moving products.

Conclusion

Overall, the working capital ratio is an essential measure for checking the efficiency and effectiveness of capital investment in the operating process of the business. It helps the investors/analysts to compare the companies of similar standing based on better usage of funds and operating cycle. However, though it gives a clear picture of the organization’s capabilities to convert initial investments to the realization of revenue, it becomes difficult to understand due to the involvement of multiple variables.

Frequently Asked Questions (FAQs)

What does negative days working capital mean?

When a business’s current liabilities are more significant than its income and assets, it is considered to have negative working capital days. It is usually a temporary situation when the company makes a necessary purchase, such as buying more stock, new products, or equipment.

Is days working capital and cash conversion cycle the same?

The days working capital cycle refers to the duration required to convert current net assets (current assets minus current liabilities) into cash. On the other hand, the cash cycle represents the time taken to complete the purchase-to-sales process.

How can Days Working Capital be improved?

To improve Days Working Capital, companies can focus on optimizing their inventory management, accelerating accounts receivable collection, and effectively managing accounts payable. Implementing just-in-time inventory practices, offering discounts for early payment, and negotiating favorable payment terms with suppliers can help reduce DWC.

Recommended Articles

This article is a guide to Days Working Capital. Here, we discuss the days working capital calculation, formula, examples, advantages, and disadvantages. You can learn more about Excel modeling from the following articles: –