Part of our Cash Flow Statement guide

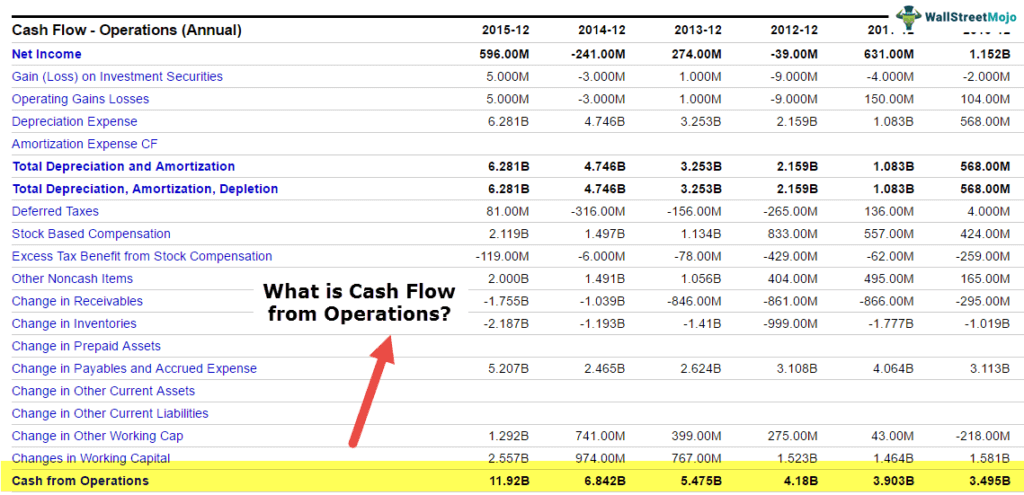

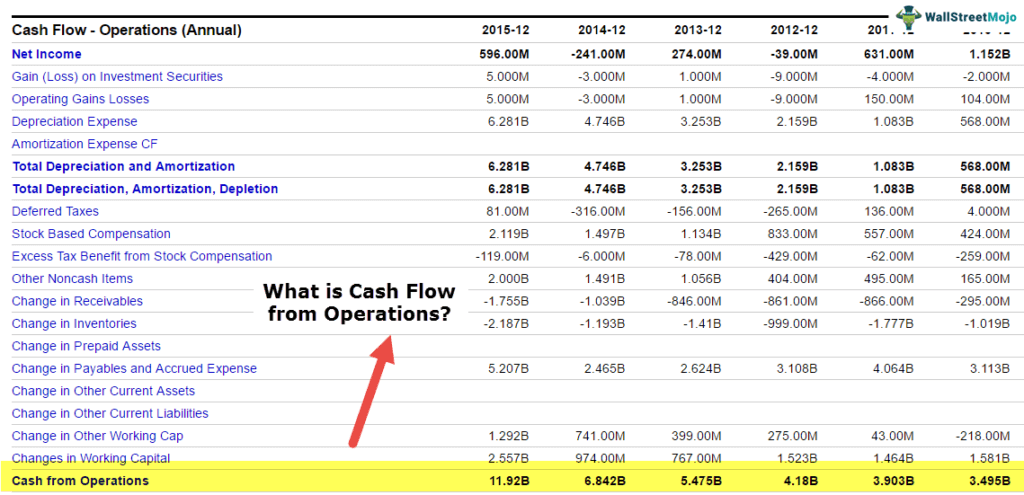

What is Cash Flow from Operations (Operating Activities)?

Cash flow from Operations is the first of the three parts of the cash flow statement that shows the cash inflows and outflows from core operating the business in an accounting year; Operating Activities include cash received from Sales, cash expenses paid for direct costs as well as payment is done for funding working capital.

‘Cash flow from operations’ tries to look into the cash inflows and outflows caused by the core business operations and, in turn, the cash generated by the company’s products and services. The main component, reflected in this part of the statement, shows the changes made in cash, accounts receivables, inventory, depreciation, and accounts payable segment. Analyst’s community looks into this section with hawkeye as it shows the viability of the business conducted by the company.

In the long run, if the company has to remain solvent at the net level, cash flow from operations needs to remain net positive (in other words, operations must generate positive cash inflows).

How to Prepare Cash Flow from Operating Activities?

Let us look at how this section of the cash flow statement is prepared. Understanding the preparation method will help us evaluate what all and were all to look into so that one can read the fine prints in this section.

The beginning point of this section is the net income figure, which is available from the income statement. If all of the company’s revenue was in the form of cash and there were no non-cash expenses, then this remains the main figure. However, since, in reality, it is not true, hence the non-cash charges and credit sales in the year need to be adjusted. Let us understand this through a hypothetical example.

Let us assume that Mr. X has started a new business and has planned that he will prepare his financial statements like income statement, balance sheet, and cash flow statement at the end of the month.

1st month: There was no revenue in the first month and no such operating expense; hence, the income statement will result in zero net income. In cash flow from the operation, the starting point would be net income, which will be zero. However, cash decreased by 700 dollars as the company decided to purchase some inventory.

| Cash from Operating activities (for the first month) | |

|---|---|

| Net Income | $ – |

| Increase in inventory | $ -700.00 |

| Cash Provided (used) in operating activities | $ -700.00 |

2nd Month: During this month, the company was able to sell 10 product units priced at 80 dollars each. The product was delivered on the 20th of the month, and the buyer was provided an invoice worth 800 dollars due by the 10th of the next month. The cost of this product is 500 dollars. Hence as per the income statement, the net income was $300 for the second month.

| CFO activities (for the second month) | |

|---|---|

| Net Income | $ 300.00 |

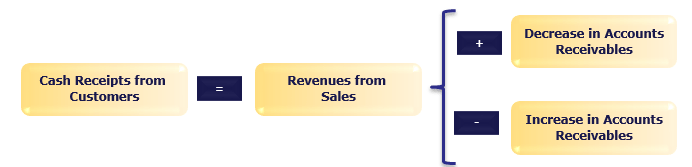

| Increase in accounts receivables | $ -800.00 |

| Decrease in inventory | $ 500.00 |

| Cash Provided (used) in operating activities | $ – |

Please note that the above cash flow from operating activities is just for the second month. The cumulative cash flow for two months would look like the one shown in the table below.

| CFO activities (end of the second month) | |

|---|---|

| Net Income | $ 300.00 |

| Increase in accounts receivables | $ -800.00 |

| Increase in inventory | $ -200.00 |

| Cash Provided (used) in operating activities | $ -700.00 |

Understanding this cumulative two-month statement: The net income for the two months of operation of the company has been 300 dollars. Since the amount is still not received by the company, it lies under accounts receivables (-800 dollars). During the two months’ inventory has increased by 200 dollars, hence shown as negative in the cumulative statement. As a result, the cash flows for the two months show that Mr. X’s cash from operating activities is a negative $700. So in simple terms, a company has brought goods and paid for them; hence cash outflow took place. The company could sell the goods, but money was still not received. Hence the company at a cumulative level is standing negative on CFO.

3rd Month: This is the month in which the quarter ends for the company. The company purchased office equipment at the start of the month for 1100 dollars (accounted for under operating activities). Due to the purchase of the office equipment, the company also incurred a non-cash depreciation charge of 20 dollars during the month.

| CFO activities (for the third month) | |

|---|---|

| Net Income | $ – |

| Depreciation charge added back | $ 20.00 |

| Cash Provided (used) in operating activities | $ 20.00 |

Please note that the above CFO is just for the third month; the cumulative cash flow for the quarter would look like the one shown in the table below.

| CFO activities (end of a quarter) | |

|---|---|

| Net Income | $ 300.00 |

| Depreciation charge added back | $ 20.00 |

| Increase in accounts receivables | $ – |

| Decrease in inventory | $ -200.00 |

| Cash Provided (used) in operating activities | $ 120.00 |

Understanding this cumulative quarter statement: The net income for the quarter of operation of the company has been 300 dollars. During the three months’ inventory has increased by 200 dollars, hence shown as negative in the cumulative statement. There is a depreciation charge of 20 dollars, which is added back. As a result, the cash flows for the three months show that Mr. X’s cash from operating activities is $120.

Calculating Cash Flow from Operations – Direct Method

Calculating Cash flow from Operations using the direct method includes determining all types of cash transactions, including cash receipts, cash payments, cash expenses, interest, and taxes.

Steps to calculate cash flow from operations using the direct method are given below –

A) Cash Receipt: Represents the actual amount of cash received during the period

B) Cash Payment: Represents the actual amount of cash payments to the suppliers

C) Cash expenses may include selling, administration, R&D, and changes in other operating liabilities

D) Cash interest-only recognizes interest expense paid in cash

E) Cash Tax: Represents only taxes paid in cash

Cash Flow from Operations Formula (Direct Method) = Cash Receipts – Cash Payments – Cash Expenses – Cash Interest – Cash Taxes

Cash Flow from Operations – Direct Method Example

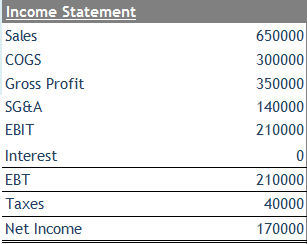

ABC Corporation’s income statement sales were $650,000; gross profit of $350,000; selling and administrative costs of $140,000; and income taxes of $40,000. The selling and administrative expenses included $14,500 for depreciation.

Calculate Cash Flow from Operations using the Direct Method.

The following additional information is available.

- Cash Receipt = $650,000 – ($81,000 – $65000) = $634,000

- Cash Payment = $300,000 – ($55,000 – $42,000) – (45,000 – $38,000) = $280,000

- Cash Expense = $140,000 – $14,500 = $125,500

- Cash Taxes = $40,000

Cash Flow from Operations using Direct Method formula =

$634,000 – $320,000 – $125,500 – $40,000 = $188,500

Video Explanation Of Cash flow from Operations

Calculating Cash Flow from Operations using Indirect Method

Calculation of Cash flow from operations using the indirect method starts with the Net income and adjusts it as per the changes in the balance sheet.

Steps to calculate cash flow from operations using the indirect method are given below.

Step 1:

- Start with Net Income

Step 2:

- Subtract: Identify gains or losses that result from financing and investments (like gains from the sale of land)

Step 3:

- Add: Non-cash charges to income (such as depreciation and goodwill amortization) and subtract all non-cash revenue components.

Step 4:

- Add or subtract changes to operating accounts.

- Operating Assets: An increase in operating asset balances is subtracted, while the decrease in those accounts is added.

- Operating Liabilities: Increases in the balances of operating liability accounts are added, while decreases are subtracted.

Cash Flow from Operations Formula (Indirect method) = Net Income + Gains & Losses from financing & investments + Non-cash charges + changes in operating accounts

Cash Flow from Operations – Indirect Method Example

Let us work through the same Cash Flow from Operations example we used for using the Direct Approach.

ABC Corporation’s income statement sales were $650,000; gross profit of $350,000; selling and administrative costs of $140,000; and income taxes of $40,000. The selling and administrative expenses included $14,500 for depreciation.

Calculate Cash Flow from Operations using Indirect Method

The following additional information is available.

Since we are not provided with the Income Statement, let us quickly prepare an Income statement for the above.

Step 1: Net Income is $170,000

Step 2: There are no gains or losses from financing and investments = $0

Step 3: Add depreciation (non-cash item) of $14,500

Step 4: Add or subtract changes to operating accounts

- Cash outflow due to changes in Accounts Receivable = 65,000 – 81,000 = -16,000

- Cash inflow due to changes in Inventory = 55,000 – 42,000 = 13,000

- Cash inflow due to changes in Accounts Payables = 45,000 – 38,000 = 7,000

- Total changes in Operating accounts = -16,000 + 13,000 + 7,000 = $4,000

Cash Flow From Operations formula (Indirect Method) = $170,000 + $0 + 14,500 + $4000 = $188,500

Why is it important?

CFO is always compared to the company’s net income. If it is consistently higher than the net income, it can be safely assumed that the company’s quality of earnings is high. It has been seen that analysts raise a red flag when the CFO is lower than the net income. The question, in this case, is why the reported net income is not turning into cash for the company.

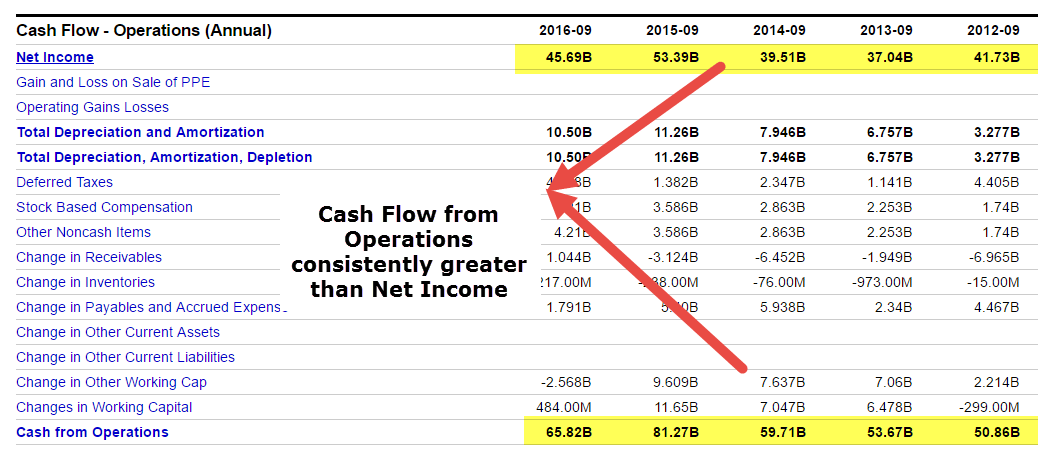

source: ycharts

The main reason why a company exists is to earn revenue and create shareholder revenue. This is the prime reason why assessing whether the company has been able to generate cash by operating activities is an important component. As from above, we can see that Apple Incorporation in FY15 has generated $81,7 billion as cash from operating activities, of which $53,394 billion has been generated as Net income.

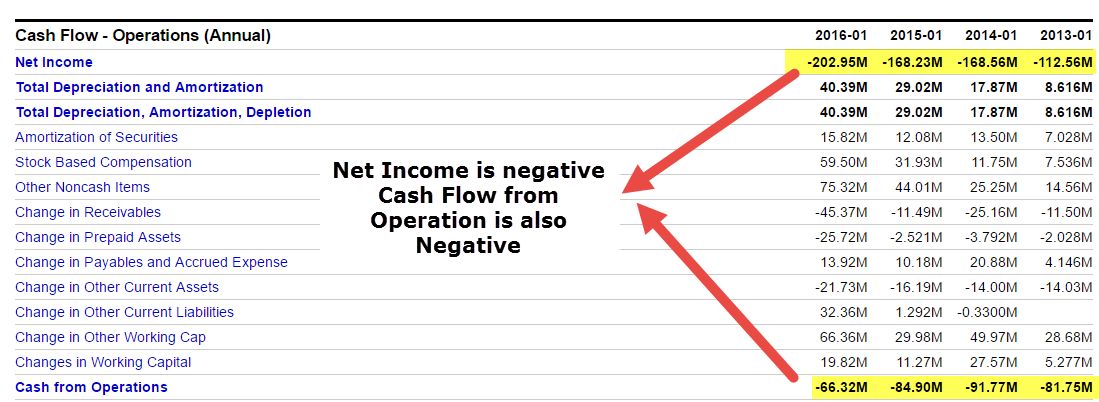

Let us now look at another company’s cash flow from operations and see what it speaks about the company. This is the case with Box. The company, for years, didn’t generate accounting profit, but investors kept putting money into the company on the backdrop of a solid business proposition.

source: ycharts

Think of a pharma company doing strong R&D, and there is a possibility of seeing a blockbuster patented drug being launched in a few years. During this period, investors will be looking at the fact whether the company has enough cash to continue operations during this period. Our objective is to make you assess the importance of cash flows in the company and how it plays a critical component in the business world.

Conclusion

As we have seen throughout the article, cash flow from operations is a great indicator of the company’s core operations. It can help an investor gauge the company’s operations and see whether the core operations are generating ample money in the business. If the company is not generating money from core operations, it will cease to exist in a few years.

Recommended Articles

For more on Cash Flow Statement, explore these related articles from our Cash Flow Statement guide.