Part of our Cash Flow Statement guide

Statement of Cash Flows Definition

A Statement of Cash Flow is an accounting document that tracks the incoming and outgoing cash and cash equivalents from a business. It helps identify the availability of liquid funds with the organization in a particular accounting period. Thus, it accounts for a company’s financial standing and reveals the corporate efficiency in managing its cash and liquidity position.

Besides, statement of cash flow equation also classifies business activities into operational, investing, and financing activities. This differentiation helps identify a company’s profitability arising from each activity. It also enables stakeholders like investors, shareholders, and creditors to assess the extent of risk and return expected from a business.

- A cash flow statement records the overall cash movement in and out of business throughout an accounting period. It ascertains the closing balance of cash and cash equivalents at the end of the year.

- It accounts for three major business activities in which cash is exchanged, i.e., operating, investing, and financing.

- The operating activities include everyday business cash transactions. The investing activities comprise the long-term asset purchase or sale. In contrast, the financing activities involve all transactions that affect the equity and liabilities of a company.

- There are two ways of calculating cash flows: direct and indirect.

Statement of Cash Flows Explained

A cash flow statement (CFS) is one of a business’s most important financial reports. Unlike the income statement and balance sheet, which concentrate on accounting profits, a CFS deals with the cash component of a business. Since cash provides liquidity, it is decisive for the survival of a business.

A CFS records a firm’s all cash-based transactions during a particular accounting period. In other words, it mirrors the availability and usage of business funds to reveal its current state of liquidity. Thus, it explains how well a corporate unit manages its resources (cash and cash equivalents) to ensure uninterrupted business functioning and generate profits.

Further, statement of cash flow analysis is essential for corporate planning in the short run as it gauges a company’s capacity to meet its short-term obligations. Besides, it is also crucial for business forecasting, determining liquidity status, dividend decision-making, borrowing in case of monetary shortage, and wisely allocating surplus funds.

Besides, it discloses vital information regarding the solvency of a business. As opposed to other financial statements, it is more difficult to manipulate and, therefore, more reliable. Hence it is widely sought after by the stakeholders of a business.

The cash flows in a business from three significant activities: operating, investing, and financing. Thus, a cash statement presents the cash generated and spent on all these activities individually and collectively.

Following are the basic steps to preparing a CFS:

- Take the opening balance of cash and bank available at the beginning of the respective accounting year.

- Add to it all the incoming cash from various sources like cash sale of goods or services, proceeds from the sale of assets or investments, the funds acquired by the issue of shares or through bank loans, etc.

- Subtract the cash outflows from payments like salaries, dividends, rent, insurance, loan repayment, stock repurchase, taxes, etc. Also, deduct the money invested in business projects or offered as a loan.

Then the net amount so evaluated is the cash in hand remaining with the company.

Formula

Let us understand the formula that shall act as a basis for us to form a statement of cash flow equation as explained below.

Net Cash Flow = Operating Activities + Investing Activities + Financing Activities

Here,

Operating Activities = Cash transactions related to core business operations, including receipts and payments for goods and services.

Investing Activities = The cash transactions related to the acquisition and sale of long-term assets.

Financing Activities = It involves cash transactions with the company’s owners and creditors, including equity and debt-related activities.

Cash Flow – Video Explanation

Purpose

Let us understand the purpose of this concept through the discussion below.

- The statement of cash flow equation provides a comprehensive snapshot of a company’s cash position, detailing cash inflows and outflows during a specific period.

- One of its primary purposes is to assess the liquidity of a business. It helps stakeholders understand if the company has enough cash to cover its short-term obligations.

- By categorizing cash flows into operating, investing, and financing activities, the statement offers insights into the sources and uses of cash, helping immensely in evaluating the company’s operational efficiency.

- Investors and creditors utilize the statement of cash flow to measure a company’s ability to generate positive cash flows. A positive cash flow shows financial stability, which brings confidence among stakeholders.

- Management relies on the statement of cash flow for strategic decision-making. It assists in planning investments, managing working capital, and determining the need for external financing.

- It serves as a key indicator of a company’s overall financial health. A consistent positive cash flow from operating activities indicates effective financial management, while negative cash flow may raise serious concerns.

Format

The CFS is subdivided into three categories:

#1 – Cash flow from Operating Activities

Cash Flow from Operating Activities includes cash used in or generated from the daily core business activities. The operational activities are the principal revenue-generating or expense-incurring activities of the company. It includes selling goods or services and payment towards expenses like salaries, taxes, etc.

Some operating activities that result in cash inflows and outflows are listed below.

| Cash flow from Operating Activities | |

| Cash Inflows | Cash Outflows |

| Sales revenue received from customers | Rent paid |

| The commission, brokerage, royalty, and other fees received | Cash payment to suppliers and vendors |

| Receipts from debtors | Salary, wages, and commission paid |

| Taxes paid | |

| Purchase of stock in cash | |

| Freight and other expenses paid | |

#2 – Cash flow from Investing Activities

Cash flow from Investing Activities represents the outgoing or incoming cash from acquiring or disposing of a company’s long-term assets and holdings. Assets include land, property, plant & equipment, investments in other companies, etc.

Listed below are some of the cash flows through investing activities:

| Cash flow from Investing Activities | |

| Cash Inflows | Cash Outflows |

| Proceeds from the sale of fixed asset | Purchase of fixed assets |

| Cash is received from selling investments in other companies like bonds, fixed assets, equity, debentures, etc. | Buying of shares, debentures, and other long-term or short-term investment instruments issued by other companies |

| Money received on maturity of shares, debentures, and bonds. | |

| Dividends and interest received on investments. | |

#3 – Cash flow from financing activities

Cash Flow from financing activities shows the capital receipts and payments marked by the transactions with the corporate finance providers like banks, shareholders, and promoters.

Given below are some the examples of cash flows from financing activities:

| Cash flow from Financing Activities | |

| Cash Inflows | Cash Outflows |

| Proceeds from borrowings from banks and other financial institutions | Repayment of borrowings or loan installments |

| Proceeds from issuance of the shares and debentures | Buyback of debentures and shares |

| Interest paid on loans and borrowings. | |

| Dividend paid on shares issued. | |

How To Prepare?

As discussed, the CFS is a sum of all operating, investing, and financing activities. Thus, it reflects the net increase or decrease in cash flows of a business.

There are two methods for calculating cash flows: direct and indirect. Note that the difference between the two methods lies in computing cash flows from operating activities. In contrast, the cash flows from investing and financing activities are treated similarly in direct and indirect methods.

#1 – Direct Method

Only the cash operating items are recorded using the direct method of preparing CFS. This method is relatively easy to understand as it considers the actual cash transactions.

The cash from operating activities can be straightaway computed by adding all the cash receipts and deducting all the cash payments. Later the cash from all the three activities, i.e., operating, investing, and financing, can be summed up to get the closing balance of cash and cash equivalents.

| Cash Flow Statement – Direct Method | |||

| Particulars | Amount | Total amount | |

| Opening Cash Balance | XXXX | ||

| Cash flow from operating activities: | |||

| Receipts from sale of goods and services, royalties, etc. | XXXX | ||

| Payment to employees, taxes, suppliers, etc. | (XXXX) | ||

| Net cash from operating activities (A) | XXXX | ||

| Cash flow from investing activities: | |||

| Sale of investments, vehicles, property, etc. | XXXX | ||

| Purchase of machinery, plant, equipment, etc. | (XXXX) | ||

| Net cash from investing activities (B) | (XXXX) | ||

| Cash flow from financing activities: | |||

| Proceeds from issuing shares, borrowings from banks, etc. | XXXXX | ||

| Repayment of loan | (XXXX) | ||

| Payment of dividends to shareholders | (XXX) | ||

| Net cash from financing activities (C) | XXXX | ||

| Add: Net cash flow during the year (A + B + C) | XXXX | ||

| Ending Cash Balance | XXXXX | ||

The Financial Accounting Standards Board (FASB) and International Accounting Standards Board (IASB) suggest that companies record their cash flows through the direct method. But it is not a handy method for the organizations since various accrual incomes and outstanding expenses are equally significant in accounting.

#2 – Indirect Method

The statement of cash flow analysis prepared through an indirect method requires adjustment of the non-cash items which are earned but not yet received. These changes are made to the net profit or loss of the company in the particular accounting year.

The non-cash and non-operating expenses are added back to the net profit/loss, while all the non-operating and accrued incomes are subtracted. Thus, it is the reverse treatment of the income statement and provides the operating profit before the working capital changes.

| Cash Flow Statement – Indirect Method | |||

| Particulars | Amount | Total amount | |

| Cash flow from operating activities: | |||

| Profits before tax | XXXX | ||

| Add: Non-operating expenses | |||

| Depreciation, accounts payable, accrued expenses, etc. | XXXX | ||

| Less: Non-operating income | |||

| Accounts receivable, prepaid expenses, unearned revenue, etc. | (XXXX) | ||

| Operating profits before working capital changes | XXXX | ||

| Add: Decrease in current assets and increase in current liability | XXXX | ||

| Less: Decrease in current liability and increase in current assets | (XXXX) | ||

| Net Cash from operating activities (A) | XXXX | ||

| Cash flow from investing activities: | |||

| Proceeds from sale of fixed assets | XXXX | ||

| Purchase of fixed assets | (XXXX) | ||

| Net cash from investing activities (B) | XXXX | ||

| Cash flow from financing activities: | |||

| Proceeds from issuing shares, borrowings from banks, etc. | XXXX | ||

| Payment of borrowings, dividends, etc. | (XXXX) | ||

| Net cash from financing activities (C) | XXXX | ||

| Net cash flow during the year (A + B + C) | XXXX | ||

| Add: Opening cash balance | XXXX | ||

| Ending Cash Balance | XXXX | ||

The corporates widely use the indirect method since the books of accounts are on an accrual basis, thus making it a more practical approach.

Examples

Now that we understand the theoretical aspect of the statement of cash flow equation through the discussion so far, let us also understand the practicality of the concept through the examples below.

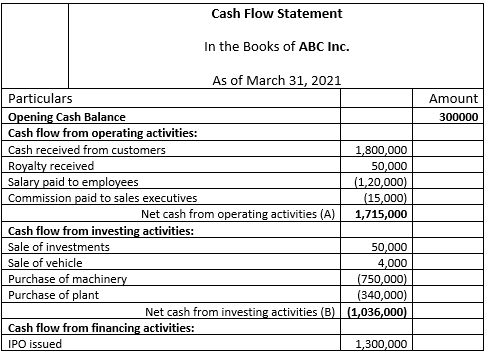

Example #1

ABC Inc. presented the following CFS for the year ending March 31, 2021:

Note that we have considered the direct method of preparing the CFS as recommended by IASB and FASB. Thus, we can say that by the end of the accounting year 2020-2021, ABC Inc. is left with $1,774,000 as cash and cash equivalents.

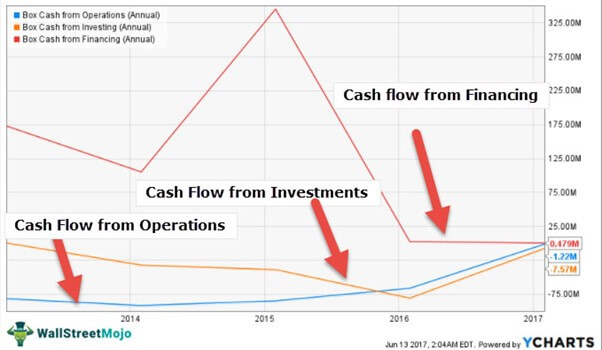

Now, moving on to a real-world example, let us discuss the cash flows of Box Inc. from 2014 to 2017.

Example #2

source: ycharts

- Cash Flow from Operations – Consists cash generated from Software-as-a-Service (SaaS) cloud content management platform. Box cash flow from operations is weak due to back-to-back losses over the years.

- Cash Flow from Investing Activities – Box cash flow from investing activities was at -$7.57 million in 2016 compared to -$80.86 million in 2015. This reduced cash flow was primarily due to reduced capital expenditure in the core business.

- Cash flow from Financing Activities – Box cash flow from financing activities has shown a variable trend. In 2015, Box came up with its IPO. This magnified its cash flow from financing ($345.45 million) in 2015. Before its IPO, Private Equity Investors financed Box Inc.

Importance

Let us understand the importance of the concept through the points below.

- The statement of cash flow analysis is crucial for evaluating a company’s liquidity and its ability to meet its short-term obligations, as it provides a clear picture of cash inflows and outflows.

- By segregating cash flows into operating, investing, and financing activities, the statement helps investors and stakeholders understand the sources of a company’s cash and how it is allocated.

- Investors often rely on the statement of cash flow to verify a company’s financial stability. A positive cash flow indicates efficient financial management and the ability to fund operations and growth without relying heavily on external financing.

- For management, the statement of cash flow is a decision-making tool. It assists in strategic planning, helping executives make decisions about investments, financing, and day-to-day operations.

- Monitoring cash flow is instrumental in identifying potential financial distress. A negative cash flow from operating activities could signal issues that require immediate attention.

Statement of Cash Flow Vs Income Statement

→ Explore all 32 Income Statement articles

While both these statements provide important insights into the financial health of the business, there are distinctions in their fundamentals and implications. Let us understand them through the comparison below.

Statement of Cash Flow

- It primarily deals with the movement of cash in and out of the business.

- Includes operating, investing, and financing activities, offering a detailed view of cash-related movements.

- It provides insights into the company’s ability to meet short-term obligations and assess its overall liquidity.

- It also emphasizes the timing of cash transactions, regardless of when revenues or expenses are recognized.

Income Statement

- The income statement focuses on the company’s profitability during a specific period, detailing revenues, expenses, and net income.

- It utilizes accrual accounting principles, recognizing revenues and expenses when incurred, irrespective of cash movements.

- It reflects the company’s operational performance and efficiency in generating profits.

- Also, it includes non-cash items like depreciation, which impact profitability but may not involve actual cash transactions.

Frequently Asked Questions (FAQs)

What is a statement of cash flows?

A cash flow statement is a financial report that keeps a record of the inward and outward movement of business cash and equivalents in a given accounting period. It helps to figure out the funds available to the company.

How to prepare a cash flow statement?

Following are the basic steps to proceed with a cash flow statement:

1. Write the opening balance of cash and bank for the year.

2. Add all the annual cash inflow from operating, investing, and financing activities.

3. Deduct all outbound cash flows via operating, investing, and financing activities.

4. Finally, you get the cash and cash equivalents closing balance for the respective accounting period.

What is the purpose of the cash flow statement?

The chief aim of preparing a cash flow statement is to trace the cash journey from opening to the ending balances. This journey traces the sources of cash generation and usage during a particular accounting year.

Is cash flow the same as profit?

Cash flow indicates the available funds with the company at the end of the accounting year. On the other hand, profit is an organization’s earnings after all expenses have been met in a particular period.

Recommended Articles

This has been a Guide to Statement of Cash Flows. Here, we discuss the definition, formula, purpose, format, direct and indirect method, and importance. You can learn more about financing from the following articles –