Table of Contents

What Is A Community Reinvestment Act (CRA)?

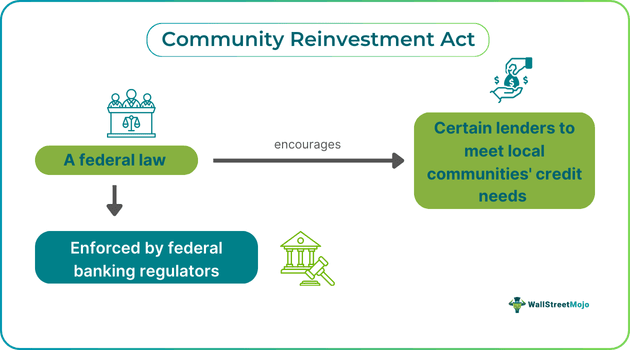

The Community Reinvestment Act or CRA, in short, refers to a federal law that came into existence in 1977. It mandates the federal banking regulators to encourage banks and other depository institutions to fulfill the credit requirements of the communities where they operate, including low-to-moderate income or LMI neighborhoods.

Federal banking agencies or regulators are responsible for enforcing this Act. They gauge how well the depository institutions fulfill their obligations towards the communities. They take such assessments into account when doing the evaluation of applications concerning the approval of bank charters, acquisitions, deposit facilities, branch openings, and mergers in the future.

Key Takeaways

- The Community Reinvestment Act definition refers to a law introduced in the US in 1977.

- The aim of this Act is to encourage deposit-accepting financial institutions to take measures that can fulfill the credit requirement of the communities where they offer their services.

- Banks must provide LMI communities with safe and sound operations consistently to meet the Community Investment Act requirements.

- There are four categories of ratings per this Act. Among them, the best overall rating is ‘Outstanding.’

- The OCC, FRB, and FDIC gauge the performance of banks with regard to the fulfillment of local communities’ credit requirements.

Community Reinvestment Act Explained

The Community Reinvestment Act definition refers to a federal law in the US. It aims to encourage depository institutions to adequately cater to the banking requirements of every member belonging to the communities served by them.

Three federal banking regulators have the responsibility to enforce this Act. They are the Federal Deposit Insurance Corporation or FDIC, the Office of the Comptroller of the Currency or OCC, and the Federal Reserve Board or FRB. Each of these regulators has an exclusive CRA site that gives information regarding the banks that they supervise and those financial institutions’ performance evaluations and CRA ratings.

Among the three regulators, FRB chiefly has the responsibility to evaluate if the state banks that are members of the Federal Reserve System are fulfilling the obligations according to the regulations of the Act.

History

A federal agency known as HOLC developed maps classifying neighborhoods across the nation and color-coding them based on a perceived risk level. It determined the risk level on the basis of information accumulated from different sources, including loan officers, city officials, real estate agents, and local appraisers.

Per the agency, the red color depicted hazardous communities having primarily ethnic and racial minority populations. As a result of this classification, the banks in the US systematically refused to provide mortgages to people of color, including black Americans residing in specific areas, which were “redlined”.

The enactment of this law took place in 1977 to address the inequities concerning access to credit and systematic divestment in urban areas. It aimed to do so by encouraging banks to fulfill the LMI communities’ credit requirements and put an end to redlining. In various cases, loan providers moved from having adversarial relationships with certain communities to cooperating with the purpose of fulfilling mutual objectives.

The Community Reinvestment Act of 1977 also gave the public the capacity to make comments or file protests in case they deemed the lenders’ practices insufficient.

Ratings

Upon the completion of a regulator’s CRA exam, it assigns an overall CRA rating utilizing four categories of ratings, which are as follows:

- Substantial non-compliance

- Needs to improve

- Satisfactory

- Outstanding

The regulators need to assign the above ratings to the state member banks after taking into account investment and lending data following an update in 1995. However, the assessment is still somewhat subjective, and there is still no particular quota that the banks must satisfy.

The Federal Deposit Insurance Corporation keeps an online database in which the general public can view a specific bank’s score. In addition, banks have the obligation to give the consumers their performance assessments if the latter place a request.

Examples

Let us look at a few Community Reinvestment Act examples t understand the concept better.

Example #1

Suppose ABC Bank is a financial institution offering its services in a community that primarily includes people of color who do not have much access to credit. To meet the Community Reinvestment Act requirements, ABC decided to launch a housing loan program that would provide LMI individuals with mortgages at a very low interest rate. Moreover, ABC launched a small business loan program with the aim of providing financial assistance to minority businesspersons.

The above initiatives taken by ABC Bank helped in the expansion of minority-owned businesses and increased the number of homeowners in the community. Because of these measures, the bank received an overall ‘Outstanding’ CRA rating.

Example #2

On September 16, 2024, Santander Bank announced that the OCC gave it an overall ‘Outstanding” CRA rating for the exam period of 2020-2022. According to the bank’s US chief executive officer, Time Wennes, the ‘Outstanding’ rating serves as proof that the organization is committed to having a positive effect on the communities where it operates.

In the performance assessment report, OCC highlighted various areas in which the bank excelled. For example, it offered flexibility to customers from the start of the COVID-19 pandemic till the end of the assessment period.

During this time, the bank supported small businesses across its footprint that were affected by the pandemic. Besides this, Santander showcased great responsiveness to community credit requirements, made significant investments, provided grants, and made its offerings readily accessible to individuals and geographies having different income levels.

Importance

One can understand the advantages of this Act by going through the following points:

- This act plays a key role in helping different communities meet their credit requirements.

- It aims to ensure that LMI borrowers get access to safe and secure banking operations on a consistent basis.

Criticisms

According to a few conservative pundits and politicians, the Community Reinvestment Act of 1977 led to risky lending practices, which, in turn, resulted in the 2008 financial crisis. They claim that lenders, including banks, relaxed specific standards to get mortgage approvals and satisfy the CRA examiners.

However, economists Daniel Ringo and Neil Bhutta argued mortgages based on CRA accounted for a small portion of the overall subprime loans that the banks issued during the crisis. Hence, both concluded that the Act was not a major contributing factor concerning the subsequent downturn in the housing market.

Some experts believe that this law has not been that effective. According to a researcher of the Federal Reserve, Jeffrey Gunther, although the LMI communities witnessed an inflow of loans following the Act’s enactment, loan providers that do not have to abide by the law, for example, credit unions account for an identical share of the loans.