Part of our Financial Planning guide

What Is Asset Allocation Calculator?

An asset allocation calculator is an ideal way to divide the funds to achieve maximum return with minimum cost and risk. Even though professional financial advisors are there to help with investment advice through proper client assessment, a calculator is an equally smart way to do so.

An individual will use this calculator to allocate their funds or investments in the different asset classes depending upon their age, risk profile, life goals, etc. It gives suggestions regarding how the portfolio can be arranged across various asset classes, after taking into account the risk-taking capacity, investment goals and time horizon.

Asset Allocation Calculator Explained

An asset allocation calculator refers to a tool that can be used to allocate and bring a balance to the portfolio of an individual through evaluation of risk and return. It is an ideal way in which one can seek to access the most effective investment strategies based on their risk profile, time horizon and objective.

There are different types of asset classes where one can park their hard-earned money. They can be stocks, mutual funds, commodities, fixed income, gold, real estate, as so on. Each of them has its own return and risk levels. It is essential to understand every asset class before putting money in them by using the investment or retirement asset allocation calculator.

Fluctuation in the financial market is the main reason why investors gain as well as lose money if allocation is not done in the optimum manner. With the help of proper advice and usage of a good financial tool like an asset allocation calculator can help minimize the risk, so that they get averaged out. Such ready-to-use asset allocation calculator excel are being increasingly adopted by investors, where dividing the funds is quite easy. The user needs to enter some necessary information and create a profile that can be used to get the allocation recommendation. However, it should be noted that the tool can only give suggestions. And it is upto the investor whether they will accept it or not.

Calculator

The formula for Calculating Asset Allocation is as below:

Asset Allocation for Stock = 100 – A

Wherein,

A is the age of the individual.

Note: The rest of the portion will be either invested in bonds or cash, which are less risky when compared to stock.

Asset allocation is not an easy task, and there is no one method to determine the same, and it varies from case to case and individual to individual. This involves considering factors such as age, risk profile, life goals, current debt, etc., which affect many asset allocation decisions. The portfolio manager would handle those funds and change asset allocation accordingly. They have an Investment Policy Statement, commonly called IPS, which shall have a predetermined rate of return required on the portfolio, and allocation will be determined accordingly and keeps on changing if there is a change in any of the important factors.

However, since these involve a lot of complications and calculations, we shall focus on a simple formula (a thumb rule) wherein we shall subtract an age from 100 to determine the allocation to be made in stock, which is considered risky assets. The remaining percentage can be allocated to less risky assets or even can be kept in cash. For simplicity, we shall consider three asset classes – stock as a risky asset, bonds as a less risky asset, and cash equivalents treated as the least risky when compared with the other two.

How To Calculate?

One needs to follow the below steps in order to calculate the Asset Allocation using asset allocation calculator excel.

Step #1 – Determine the individual’s risk profile, the investment’s goal, and the number of years for which the investment is to be made.

Step #2 – Age is the most important factor here, which should be noted down.

Step #3 – Determine the ranges within which the investment would be allowed for risky assets per factor determined in step 1.

Step #4 – Now subtract the age noted down in step 2 from 100, which shall be the asset allocation towards a risky asset, which is equity.

Step #5 – The remaining percentage can be equally allocated to bond and cash or per individual requirement, either the remaining percentage in cash or bond.

Step #6 – The resultant is rough allocations per rule of thumb, although not the accurate ones.

Asset allocation is not easy and depends upon case to case and type of individual; their risk factors, time horizon, liquidity requirements, tax requirements, legal requirements, etc., are some of the factors that derive asset allocation. Since many individuals lack knowledge of the capital markets, this rule of thumb method would be useful.

Examples

Let us understand the concept investment or retirement asset allocation calculator with the help of some suitable examples.

Example #1

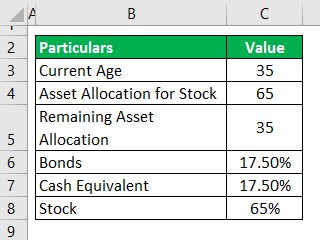

Mr. Vinay is an individual who is staying single and is 35 years old. He has never been into investment and doesn’t understand much about it. He is nicely settled in his own house and doesn’t owe any liability. His only goal is to have enough funds for himself during retirement, which is 30 years away from now.

He approaches a financial advisor who acknowledges his factors and considers his concerns and investment goal, and provides him with an IPS statement which he barely understood, and hence as the last option, recommends him to use the rule of thumb approach, which would be easy for him to understand and on an average the allocation will come close per Mr. Vinay’s requirement.

Further, Mr. Vinay chooses to allocate cash and bonds as well.

Based on the above information, you are required to calculate Asset Allocation per the rule of thumb approach.

Solution:

We can note here that Mr. Vinay is well settled, and there is no debt obligation for him; the only goal of his life is to have funds during his retirement, and therefore the risk appetite would be to allocate lesser funds in risky assets and more funds in the less risky asset.

Now we can use the below formula to calculate the Asset Allocation:

Asset Allocation = 100 – A

- = 100 – 35

- = 65%

Per the above rule of thumb formula, the allocation toward risky assets should be 65% as the time frame to invest in 30 years, and the remaining portion, which is 100 – 65, which is 35%, can be invested in cash equivalents and bonds.

However, since we aren’t given any specific allocation, we can split them into equal ratios, which are 35% / 2, which is 17.5% in cash equivalents and 17.5% in bonds.

Example #2

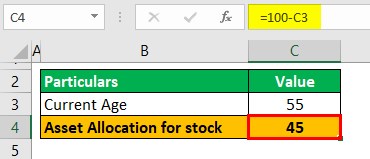

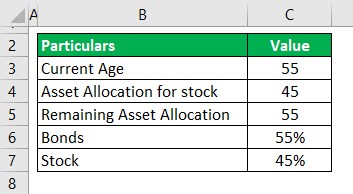

Mr. Kapoor, who is 55 years old, has been investing in the market for quite some time but has suffered losses, so he decided to reduce the asset allocation to risky assets. Since his portfolio is down, he is unsure of what has to be done further. He wants to receive a fixed monthly income and a lump sum amount at the end of 15 years. He doesn’t have any outstanding debt. He takes advice from his friend, who is MBA in finance. Because of his long-term investment, age factor, and limited knowledge of asset allocation, suggest he use a rule of thumb method for his asset allocation. Mr. Kapoor is not interested in holding any asset in cash.

Based on the given information, you are required to calculate the Asset Allocation percentage both in stocks and bonds per the suggested method of portfolio asset allocation calculator.

Solution:

We can note here that Mr. Kapoor is well settled, and there is no debt obligation for him; the only goal of his life is to have funds during his retirement, and therefore the risk appetite would be to allocate lesser funds to risky assets and more funds in the less risky asset.

Now we can use the below formula to calculate the Asset Allocation:

Asset Allocation = 100 – A

- = 100 – 55

- = 45%

He is disinterested in increasing the allocation towards risky assets. Per the above rule of thumb formula, the allocation toward risky assets should be 45% of the investment time frame in 15 years. The remaining portion, which is 100 – 45, which is 55%, can be invested in bonds and shall meet his requirement of earning a fixed income.

These portfolio asset allocation calculator can be safely used for a range of financial planning and goal achievement. It acts as an encouragement for the ones who are apprehensive regarding starting the investments because they are easy to use and understand. They often give multiple solutions at one go, providing options to the investors, from where they can choose the most suitable one. These tools may also provide the tax implications of the selected investment allocation so that the investor does not get misguided simply by the suggested return levels.

However, it is necessary to not the negative sides of best asset allocation calculator as well. All calculators may not be dependable and may have faulty algorithms that may project incorrect returns and risk levels. It is important to select the ones that have good feedback from users. The investors should also be careful not to enter incorrect information, because this will result in assessments that are unsuitable for them. Sometimes people who are not comfortable using such online tools may prefer to stay away from them. Lastly users of best asset allocation calculator should keep in mind that the calculators are just suggestions, based on assumptions. It is necessary to have a good understanding about the financial products before using the same.

Recommended Articles

This has been a guide to the what is Asset Allocation Calculator. We explain calculator, how to calculate, along with examples. You may also take a look at the following useful articles –