Compilation Report Meaning

A compilation report is a document prepared by a certified public accountant (CPA) that provides an overview and evaluation of a company’s financial statements. This report is often requested by stakeholders such as investors, lenders, and regulatory authorities to assess the reliability and accuracy of the financial information presented.

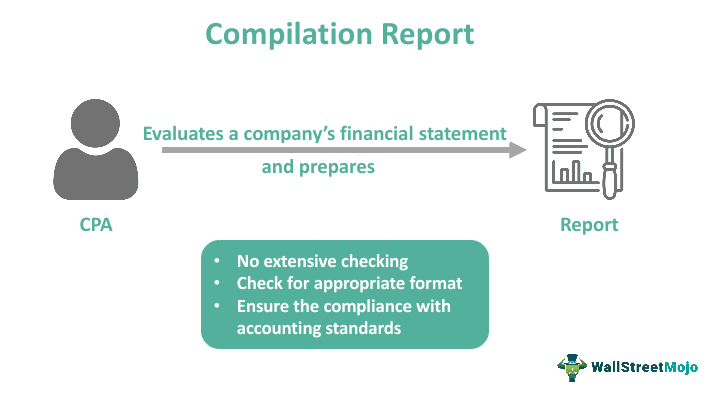

In the compilation process, the CPA collects and organizes the financial data provided by the company and performs certain analytical procedures to ensure consistency and reasonableness. However, unlike an audit or a review, a compilation does not involve extensive testing or verification of the financial information. Instead, the CPA’s objective is to present the financial statements in the appropriate format and ensure that they comply with the relevant accounting standards.

- A compilation report is a document prepared by a CPA or qualified accounting professional that provides limited assurance on the financial statements.

- It provides limited assurance on the financial statements, indicating that the CPA has organized and presented the information but does not provide an opinion on accuracy or completeness.

- A compilation report should not replace a full audit or review engagement, as it involves fewer procedures and offers a narrower assurance scope.

- Users should be aware of the limitations of a compilation report, including the absence of assessments on internal controls, data accuracy verification, and evaluation of accounting principles used.

Compilation Report Explained

The compilation report is a document that offers limited assurance on financial statements. It begins with an introductory paragraph that identifies the financial statements being compiled and states the responsibilities of the company’s management and the CPA. It clarifies that a compilation does not constitute an audit or a review and that the CPA does not express an opinion or assurance on the financial statements.

The report then describes the compilation procedures performed by the CPA, including inquiries made to the company’s personnel and analytical procedures applied to the financial data. It emphasizes that these procedures do not provide a basis for expressing an opinion on the financial statements but solely aim to assist in presenting the financial information.

Furthermore, the compilation report highlights the limitations of the compilation engagement. For example, it explains that the CPA does not assess the company’s internal controls. It also verifies the accuracy or completeness of the data provided or evaluates the appropriateness of accounting principles used. Therefore, the report advises users of the financial statements to exercise caution when relying on the information presented.

Requirements

To prepare a compilation report, the CPA must adhere to certain requirements. They should have the necessary qualifications and independence to perform the compilation engagement. Additionally, the compiled financial statements should be properly labeled and include all essential components, such as the balance sheet, income statement, and statement of cash flows. Finally, CPA should write the report following professional standards and follow a prescribed format.

Format

A typical compilation report follows a standard format that includes the following sections:

- Introductory Paragraph: Identifies the compiled financial statements and states the responsibilities of management and the CPA.

- Management’s Responsibility: Describes management’s responsibility for the financial statements and the compilation engagement.

- Accountant’s Responsibility: Explains the CPA’s responsibility in performing the compilation engagement.

- Compilation Procedures: Details the CPA’s procedures in compiling the financial statements.

- Disclaimer of Opinion: States that the CPA does not express an opinion or assurance on the financial statements.

- Limitations: Highlights the limitations of the compilation engagement.

- Signature and Date: Includes the CPA’s signature, address, and report date.

Example

Let us look at the compilation report example to understand the concept better:

[Letterhead of Accounting Firm]

[Date]

[Client Name and Address]

[City, State ZIP Code]

Compilation Report on the Financial Statements of [Client Name]

We have conducted a compilation engagement to compile the accompanying financial statements of [Client Name] as of [Balance Sheet Date], including the balance sheet, income statement, statement of changes in stockholders‘ equity, and statement of cash flows. These financial statements have been prepared following generally accepted accounting principles.

The responsibility for preparing and fairly presenting these financial statements lies with the management of [Client Name]. As the accounting firm engaged in the compilation, we are responsible for compiling these financial statements based on the information provided by management. Accordingly, we have not audited or reviewed the financial statements and do not express an opinion or any other assurance.

Our compilation followed the standards established by the American Institute of Certified Public Accountants. These standards require us to plan and perform the compilation to ensure the financial statements are free from material misstatement reasonably. However, our procedures are not designed to detect or prevent fraud or other irregularities. Nevertheless, we did perform certain analytical procedures on the financial statements and made inquiries of management regarding any known or suspected fraud affecting the company.

Based on our compilation procedures, we are unaware of any material modifications that should be made to the financial statements for them to follow generally accepted accounting principles.

We would like to emphasize that a compilation is less in scope than an audit or a review, and the objective is solely to assist in presenting the financial statements in the appropriate format. Consequently, this compilation report should not be used as a substitute for an audit or review conducted following generally accepted auditing standards.

[Accounting Firm Name]

[Accountant’s Signature]

[Accountant’s Name]

[Accountant’s Title]

[Date]

Frequently Asked Questions (FAQs)

1.What is a compilation report vs. notice to the reader?

A CPA prepares a compilation report to provide limited assurance on financial statements. At the same time, a non-CPA prepares a notice to the reader with limited assurance. It is without the same level of detail and procedures as a compilation report.

2.How much does a compilation report cost?

The cost of a compilation report varies based on factors like complexity, company size, and scope of work. Therefore, consulting with the CPA or accounting firm for a specific quote is important.

3.Can a non-cpa issue a compilation report?

Regulations may vary. However, in most cases, CPAs or qualified accounting professionals issue compilation reports. While non-CPAs may have limitations in issuing them.

4.What is an accounting officer report vs. a compilation report?

An accounting officer report is required in certain jurisdictions and focuses on compliance. At the same time, a compilation report is a broader evaluation of financial statements performed by a CPA or qualified accounting professional.

Recommended Articles

This has been a guide to Compilation Report and its meaning. We explain it with its examples, requirements, and format with example. You can learn more about it from the following articles –