What Is A Compilation Engagement?

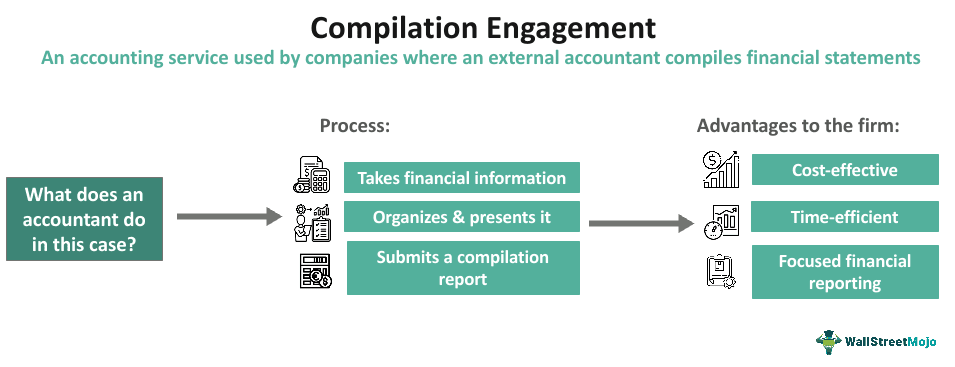

A Compilation Engagement refers to a company engaging a third-party accountant for the organization and presentation of financial statements. Though it helps firms save the cost of paying an in-house accountant, the financial statements finalized in this manner offer a lower level of assurance compared to audits.

Per this accounting service, the company provides the required information to the accountant, an independent entity. However, the accountant does not audit or review it. Their job is only to compile this information into financial statements. It means the accountant does not offer any assurance about the accuracy or completeness of such financial statements. Hence, compiled statements carry a tag that reads – No opinion or assurance is provided.

Key Takeaways

- A compilation engagement is the process of an external accountant placing a company’s financial information into specific formats to create and present financial statements without providing assurance on them. The responsibility for the accuracy and completeness of such reports lies with management.

- Some businesses use external accounting service providers to prepare financial statements on a regular basis to reduce the expense of engaging an accountant.

- An external accountant needs specific records and information to correctly organize and present financial statements, including data, existing financial records, etc.

- It helps a company finalize its financial statements. Review engagements require accountants to test the data for misstatements and errors. As part of preparation engagements, accountants prepare a company’s financial statements.

Compilation Engagement Explained

Compilation engagement involves hiring an external accountant to organize and present financial statements based on the financial data and reports a company shares for this activity. Firms issue a compilation engagement letter, which specifies the terms and conditions of the compilation engagement.

CPAs typically perform such activities, but even public accountants can be hired. They need not verify the authenticity of the data given to them for compiling the company’s financial statements. However, they can request clarifications from the firm when necessary.

Compilations are meant to explain to the reader of the financial statement that the report was prepared by an external accountant without any review engagements or audit of the data. The compilation report is attached to the financial statements organized and presented by the accountant. It is important to note that the compilation report states that no audit or review was conducted, and no assurance is provided on the accuracy, completeness, or correctness of the financial statements.

Reasons

The primary reasons for which compilation is conducted are:

- It helps management prepare financial statements without hiring a regular accountant as an employee, saving both time and money.

- Companies can enjoy the benefits offered by accounting firms in terms of expertise.

- It helps management standardize a company’s financial statements, complying with the rules and regulations applicable to companies operating in the region.

- It allows firms to file tax returns.

- It empowers management to make correct decisions related to business growth.

- Lenders get a fair idea of the financial health of a firm before approving loans.

Compilation Engagement Framework

Before preparing a compilation engagement, a structure must be followed. It has been described below.

- Planning: The accountant examines and understands the company’s business and outlines the requirements of the engagement.

- Case Reviews: This involves examining the existing accounting information and financial records to structure the compilation activity.

- Communications: With this, the accountant gets the information required to complete the assigned task, where deadlines and requirements are clearly stated.

- Acceptance of Engagement: The type of accounting service to be provided is determined at this stage. It is documented and finalized.

- Execution of the Engagement: The accountant studies the financial statements, seeks additional information (if needed), and completes the activity per the defined terms.

- Documentation and quality control: The activity is documented, and the necessary paperwork is completed. Accountants submit evidence of the activity being performed in accordance with the required accounting practices and procedures.

- Notice and Conclusion to Reader: Such agreements were previously also called Notice to Reader. As part of the compilation engagement procedures, a notice highlighting the fact that no assurance is provided is provided to the users.

- Folders of work: Accountants submit organized files and folders to show every procedure that was performed and completed during the assigned activity.

Though independent audit firms or auditors may perform both audit and compilation engagements for companies, a compilation engagement is not necessarily considered part of auditing. Hence, compilation engagement in auditing depends on the terms of engagement. For instance, compilations may sometimes be part of a full-fledged audit engagement.

Requirements

An external accountant requires certain documents, data, and information to organize and present financial statements and submit a compilation report. They are:

- Letter of engagement: It is an in-principle contract between a client and the external accountant that defines the services the accountant will provide for a fee. When both parties sign the document, it becomes a legally binding agreement. The contents of such letters are:

- Introduction (contract date, company/client name, accounting firm name, etc.)

- Scope of services

- Management’s responsibilities

- Fees and any other payments (as agreed upon and applicable)

- Duration, terms and conditions, termination clauses

- Confidentiality requirements

- Communication requirements

- Financial statements: The accountant secures the required information from management based on the engagement terms and uses the information to prepare financial statements in line with the applicable financial reporting framework. After studying the information, the accountant compiles the financial statements (based on the data provided) and drafts a compilation report stating no assurance is provided. Upon completion of the compilation, the statements and compilation report are submitted to management with the date specifically mentioned. The work is documented per the required compilation standards.

- Compilation report: This report states that no audit or review has been performed, and no opinion or any other form of assurance is provided on the financial statements. It also states that management is responsible for the fair presentation of the financial statements in adherence to the applicable financial reporting framework. The report is dated upon the completion of the compilation activity and is marked as of the date of compilation.

Examples

Let us study some examples to understand the concept in detail.

Example #1

Stargold Ltd., a business selling handicrafts, hired Expert Accounting Services to prepare its financial statements for the year ending December 31, 2023. For this purpose, the following steps were taken.

- A team from Expert Accounting Services scheduled a meeting with executives of Stargold Ltd. and met with them to finalize the terms of engagement, including scope, timeframe, fees, and reporting requirements.

- Eliza, an accountant, was assigned by Expert Accounting to this case, and she gathered the relevant information from management, including items like general ledgers, bank statements, previous tax returns, invoices, receipts, inventory records, payroll, etc.

- Eliza began the inquiry process and gathered further information about the company’s accounting processes, internal controls, etc.

- She organized the financial information and undertook reconciliations based on the accounting standards finalized during the initial discussions.

- Eliza prepared the balance sheet, income statement, cash flow statement, etc., and presented them in a clear and concise manner.

- Expert Accounting Services then issued a compilation report stating that the compilation work was done as agreed upon between the parties and Stargold Ltd. was responsible for the accuracy of the information. It also stated that the accountant does not offer any assurance for the accuracy and completeness of this information.

Stargold Ltd. now has access to compiled financial statements prepared in adherence to the applicable accounting standards. These statements can be used for internal decisions, tax filing, potential investor and lender communications, etc. However, executives at Stargold Ltd. must keep in mind that these statements have not been audited or reviewed.

Example #2

Suppose a tire manufacturer, FastWheel Tire Co., needs to present financial statements for the year ending December 31, 2023, to its lenders.

As the company operates on a small scale, it does not have an in-house accounting team. Hence, management decided to hire an accounting firm, AccuSecure & Co., to secure accounting compilation services. Adam, a CPA, has been assigned to work on this project by AccuSecure.

Adam holds a meeting with FastWheel Tire Co.’s management, discusses their needs, and studies the company’s accounting records. He gathers information about the company’s transactions, vendors, etc., and organizes the accounting information accordingly in various accounts and statements.

Adam also maintains documented records of all the procedures he undertakes while doing his job. The accounting firm provided the compilation engagement report upon completion of the assigned compilation jobs. It clearly states that the responsibility for the accuracy and completeness of the financial statements lies with the company.

When FastWheel Tire Co. submitted its loan application, it was rejected due to discrepancies in accounting records. However, the company could not hold AccuSecure responsible for this problem since the accounting firm only accessed the information that was made available to it during compilation.

Compilation Engagement vs Review Engagement vs Preparation Engagement

These terms refer to the varied levels of service accountants offer while reviewing and presenting financial statements. The differences between the three have been discussed in the table below.

| Basis | Compilation Engagement | Review Engagement | Preparation Engagement |

|---|---|---|---|

| Definition and scope | An accountant is appointed from an external firm/entity to organize and present financial statements based on the information a company provides. | An accountant reviews and analyzes financial records through certain accounting procedures to identify issues or misstatements. | An accountant prepares a company’s financial statements based on the accounting and financial records of the firm. |

| Assurance level | Accountants do not express any opinion on the correctness and completeness of financial statements. Hence, the level of assurance is low. | Accountants do not express opinions on financial statements but offer limited assurance about the absence of misstatements in a company’s records. | Accountants do not express any opinion on the financial statements since it only involves preparation, not auditing. |

| Responsibility | Management prepares the financial statements, while accountants only study and finalize them. | Management prepares the financial statements, and accountants are responsible for performing review procedures to evaluate the chances of them containing potential errors. | Accountants are responsible for preparing the financial statements. |

| Cost | These costs the lowest since it requires basic or minimal work. | The costs associated with this accounting engagement are moderate. | This costs more than the other two accounting engagement types because it involves the full preparation of financial statements. |

| Use | The compiled financial statements are generally used for internal purposes. They have limited uses. | Reviewed statements are used where a full audit is not demanded. For instance, companies preparing for an Initial Public Offering (IPO) may need reviewed statements. | These statements are used for financial reporting, investments, etc. |

Frequently Asked Questions (FAQs)

1.When performing a compilation engagement, which procedures does an accountant comply with?

When undertaking a compilation engagement, accountants must understand the industry and read financial statements in light of this context. They are also required to comply with the requirements stated in the agreement, including any accounting and financial reporting protocols. Accountants make inquiries as and when needed but do not need to validate management/company responses. They issue a compilation report stating that no audit or review was performed and no opinion or assurance is provided on the financial statements.

2.What is a compilation engagement report?

A compilation engagement report is prepared by an external accountant hired to collate, summarize, and present a company’s financial information. It differs from other financial reports since the focus is on data collection and presentation without any assurance of accuracy or completeness. Also, the scope of engagement is limited, with the company using such reports only for certain tasks—for example, internal decision-making, tax filing, etc.

3.Is an accountant who performs a compilation engagement associated with an accounting firm?

Accountants who undertake such jobs can be associated with accounting firms, or they may act independently as accounting practitioners. The most common scenario involves working for accounting firms since it gives them better access to a firm’s resources and technology compared to working independently. A key point is that they are required to hold the necessary qualifications, expertise, and experience to work on accounting compilations.

Recommended Articles

This article has been a guide to what is a Compilation Engagement. We compare it with review engagement, and explain its requirements, and examples. You may also find some useful articles here –