What Are The Components of Financial Statements?

The components of Financial Statements are the building blocks that together form the Financial Statements and help understand the business’s financial health. And consists of an Income Statement, Balance Sheet, Cash Flow Statement, and Shareholders’ Equity Statement. Each component serves a purpose and helps understand the business’s financial affairs in a summarized fashion.

Top 4 Components of Financial Statements

The four components are discussed below:

#1 – Balance Sheet

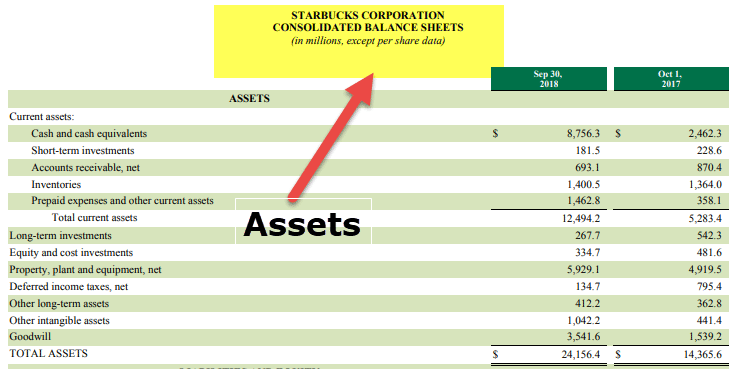

The balance sheet reports the business’s financial position at a particular point in time. It is also known as the Statement of Financial Position or Statement of Financial Condition or Position Statement.

It shows the Assets owned by the business on one side and sources of funds used by the business to hold such assets in the form of Capital contribution and liabilities incurred by the business on the other side. In a nutshell, the Balance Sheet shows how the money has been made available to the company’s business and how the company employs the money.

Balance Sheet Consists of 3 Elements:

Assets

These are the resources controlled by the business. They can take the form of Tangible Asset or Intangible Assets and can also be classified based on Current Assets (which are to be converted into cash within a year) and Non-Current Assets (which are not converted into cash within a year).

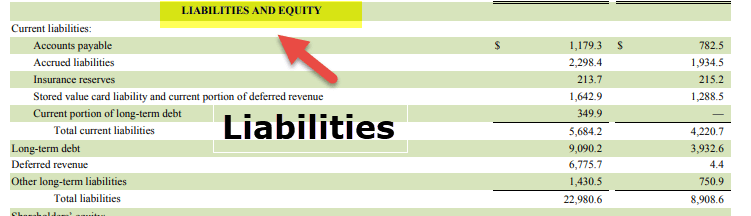

Liabilities

These are the amounts owed to lenders and other creditors. Liabilities are furtherclassified into Current Liabilities such as Bills Payable, Creditors, etc. (which are payable within a year) and Non-Current Liabilities such as Term Loans, Debentures, etc. (which are not payable within a year).

Owners Equity

Also known as Capital Contribution by the Owner. It shows the residual interest in the Net Assets of an entity that remains after deducting its liabilities. It is also a sign of the promoter’s skin in the game (i.e., business).

For each transaction in the Balance Sheet, the fundamental accounting equation holds:

Assets = Liabilities + Owners Equity

#2 – Income Statement

The Income Statement reports the financial performance of the business over some time and comprises Revenue (which comprises all cash inflows from the manufacturing of goods and rendering of services), Expenses (which comprise all cash outflows incurred in the manufacturing of goods and rendering of services) and also comprise of all gains and losses which are not attributable in the ordinary course of business. Excess of Revenues over Expenses results in Profit and vice versa, resulting in Loss for the business during that period.

Under IFRS, Income Statement also comprises Other Comprehensive Income, which consists of all changes in Equity except for shareholder transactions and, as such, can be presented together as a single statement. However, as per US GAAP guidelines, Statement of Comprehensive Income forms part of the Statement of Changes in Equity.

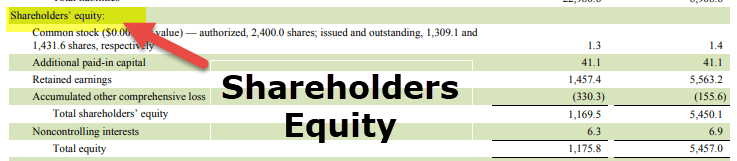

#3 – Statement of Changes in Equity

This statement is one of the financial statement components, which reports the amount and sources of changes in Equity Shareholders’ Investment in the business over a while. It summarizes the changes in the capital and reserves attributable to equity holders of the company over the accounting period. Accordingly, all the increases and decreases during the year, when adjusted with the Beginning balance, result in the ending balance.

The statement includes transactions with shareholders and reconciles each equity account’s beginning and ending balance, including capital stock, additional paid-in capital, retained earnings, and accumulated other comprehensive income. The statement shows how the composition of equity (share capital, other reserves, and Retained Earnings) has changed over the years.

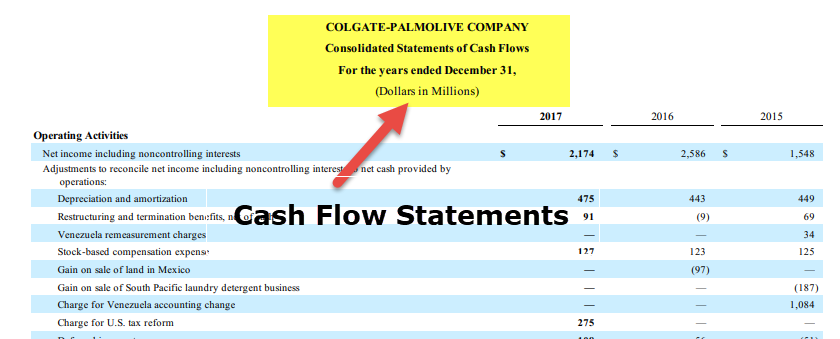

#4 – Cash Flow Statement

This statement shows the changes in the business’s financial position from the perspective of the movement of cash into and from the business. The primary rationale behind preparing a cash flow statement is to supplement the Income Statement and Statement of Financial Position. These statements don’t provide sufficient insight into movements in cash balances.

The cash flow statement bridges that gap and helps various business stakeholders understand the sources of cash and utilization of cash. There are three sections to the cash flow statement, namely:

- Cash Flow from Operating Activities starts from Operating Profit and reconciles operating profit to cash.

- Cash Flow from InvestingActivities – comprises all acquisition/purchase of long-term assets and disposal/sale of long-term Assets and other investments that are not included in cash equivalent. It also includes receipts of interest and dividends from investments.

- Cash Flow from Finance – It accounts for equity capital and borrowings changes. It comprises the payment of dividends to the shareholders cash flows arising from the repayment of loans, and fresh borrowing and issue of shares.

Conclusion

Each component of the Financial Statements serves a unique and useful purpose and helps various stakeholders understand the business’s financial health in a more simplified manner and make better decisions, either an investor or a lender, and so on.

- The balance sheet statement has its utility lies in showing the position of the business on a particular date.

- On the other hand, the income statement shows the performance of the business during the year and provides a more granular view, thereby complementing the Balance Sheet.

- The statement of changes in Equity shows how equity capital changed during the accounting period and helps stakeholders understand the Owner’s perspective.

- A cash flow statement provides information about the company’s cash receipts and cash payments during an accounting period, which provides meaningful information to analyze the business’s liquidity, solvency, and financial flexibility.

Recommended Articles

This has been a guide to Components of Financial Statements. Here we discuss the top 4 components, including income statement, balance sheet, cash flows, statement of changes in Equity with its format, and explanation. You may learn more about accounting from the following articles –