What is Temporal Method?

The temporal rate method, or the historical rate method, is employed to convert the financial statements of a parent company’s foreign subsidiaries from its local currency to its “reporting” or “functional” currency when the functional currency and the local currency are not the same. The temporal method is also utilized in the acquisition of assets and liabilities.

- The temporal method entails a majority of assets and liabilities to be evaluated by utilizing the rate of exchange in effect at the time of the creation of a particular asset or liability. Only those assets and liabilities that include a fixed foreign currency value translate at the prevailing (current) exchange rate.

- The rate of exchange used is dependent upon the valuation technique employed. For assets and liabilities valued at current prices, the present exchange rate is used. On the contrary, the assets and liabilities valued at historical prices involve using historical exchange rates.

- Income-generating assets like property, inventory, plant, equipment, etc., are updated regularly to reflect their market values by utilizing this method of currency translation. The profits and losses resulting from translation directly go to the consolidated income statement. Due to this, it affects the consolidated earnings regularly, making them somewhat volatile.

According to FASB Rule number 52, you also apply the temporal rate method if the operations at your firm carry out in an exceedingly hyperinflationary environment.

Temporal Method Video Explanation

Temporal Method Example

Consider a company based in the U.K. that acquires 70 % of the share capital of another company based in Tajikistan (where the native currency is TJS). Let’s name the acquiring company as Company ABC and the acquired company as Company XYZ. So ABC acquired 70 % of XYZ.

Now, ABC paid £ 2,600 for the acquisition of XYZ’s 70 % share capital. And for acquiring the reserves of XYZ, ABC had to pay down a sum equivalent to TJS 3,200 on the date of acquisition.

Now consider that the following rates apply:

| Time | Rate |

|---|---|

| At Subsidiary Acquisition | TJS 7.0 = £ 1 |

| When Acquiring Hard Assets | TJS 6.1 = £ 1 |

| On 31st Dec of the previous year | TJS 5.6 = £ 1 |

| Average rate through the year of acquisition | TJS 5.1 = £ 1 |

| On 31st Dec of the year of acquisition | TJS 4.6 = £ 1 |

| On the date of Dividend payment | TJS 4.9 = £ 1 |

Now, the P/L statement of Company XYZ looks like the following:

| Sales | TJS 37,890 |

| COGS | TJS 8,040 |

| Depreciation | TJS 5,600 |

| Gross Profit | TJS 24,250 |

| Distribution costs | TJS 2,090 |

| Admin. Expenses | TJS 7,200 |

| Profit before tax (PBT) | TJS 14,960 |

| Tax | TJS 6,880 |

| Profit After Tax (PAT) | TJS 8,080 |

Now, the following table shows which rate will apply to each of the above items as per the temporal method example and what will be the £ values of these items after applying these rates:

| Applicable Rate | Calculation | Value in £ | |

|---|---|---|---|

| Sales | 5.1 | TJS 37,890/5.1 | £ 7,429 |

| COGS | 5.1 | TJS 8,040/5.1 | £ 1,576 |

| Depreciation | 6.1 | TJS 5,600/6.1 | £ 918 |

| Gross Profit (GP) | – | Sales–COGS-Dep. | £ 4,935 |

| Distribution costs | 5.1 | TJS 2,090/5.1 | £ 410 |

| Admin. Expenses | 5.1 | TJS 7,200/5.1 | £ 1,412 |

| Profit before tax (PBT) | – | GP-Dist. Costs-Admin. Exp. | £ 3113 |

| Tax | 4.6 | TJS 6,880/4.6 | £ 1,496 |

| Profit After Tax (PAT) | – | PBT-Tax | £ 1,617 |

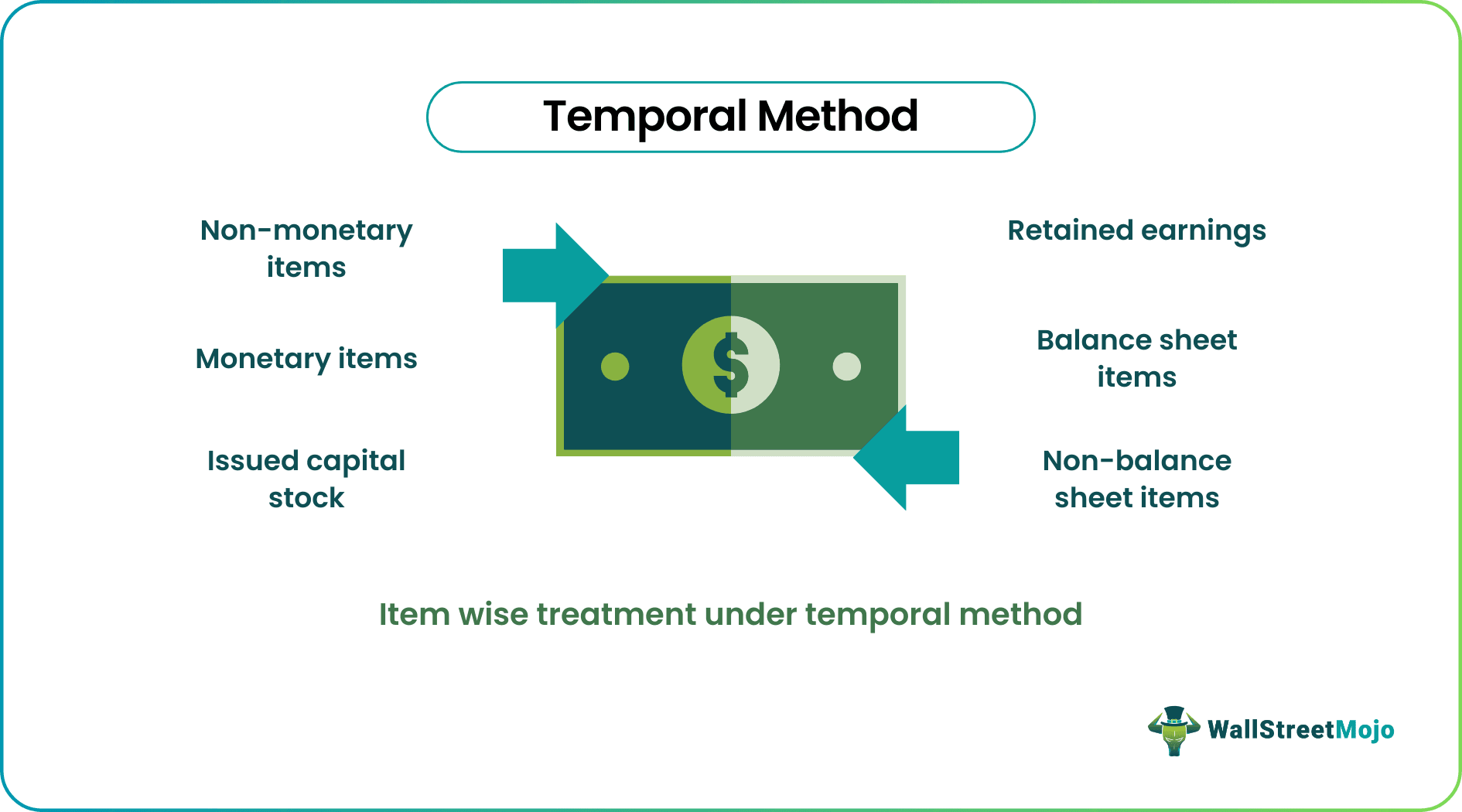

Item wise treatment

The conversion of different balance sheet and non-balance sheet items under the temporal rate method for foreign currency translation includes some item-wise nuances. The conversion is done based on various exchange rate rules for particular items. Here are some of those items and the standards used for their conversion:

- Non-monetary items: Items reported at the historical price translated by utilizing historical exchange rates that existed when the assets were purchased. Such items are inventories, fastened assets, intangible assets, etc.

- Monetary items: Translated by currency exchange rates; They include money, receivable accounts, payable accounts, long-term debt, and alternative assets or liabilities that measure in currency outside of the general rate of exchange changes.

- Issued capital stock: Translated by using the rate that existed on the date of the issuance of stock;

- Retained earnings: Retained Earnings is not required to be translated. However, it could be used to balance the assets with liabilities & owner’s equity on the balance sheet.

- Balance sheet items: Expenses, coupled with specific non-financial balance sheet items, are translated with the associated rate on the balance sheet item. Expenses translated in this way include COGS, depreciation, and amortization.

- Non-balance sheet items: Sales and a few expenses are translated by using the weighted average rate of exchange at the time of accounting.

Exchange rates used for the Temporal method

Specific exchange rates are included in the translation methodology used in the temporal rate method of currency translation. The exchange rates used are:

- Current exchange rate: the rate of exchange which exists of the date of financial reporting

- Historical exchange rate: the rate of exchange that prevailed on the date when a specific transaction took place.

- Weighted average exchange rate: a rate that captures the change in rates of an exchange over a long accounting period;

Applications

The temporal method applies the present rate of exchange to all the financial assets and liabilities (short-term as well as long-term).

The physical (non-financial) assets evaluated at past rates are translated at past rates. The different assets of an overseas subsidiary will, in all cases, be acquired over a very long period. Now, the exchange rates do not remain stable for such long periods. Hence, many different exchange rates are applied for translating these foreign assets into the multinational’s home currency.

However, the utilization of this method will result in changes in different financial ratios when the balance sheet is converted into the presentation currency because the assets and liabilities are affected in several ways.

Advantages

- Lines up with a valuation basis utilized in accounting; Therefore, the numbers have the most consistent internal meaning.

- However, they will still be misspecified just to the extent the underlying accounting numbers already are.

Disadvantages

- The financial statements of the firm will have a lot of volatility

- The mixing up of valuations makes a lot of confusion.

Conclusion

As a result of the rapid globalization of markets and the company’s presence across the globe, the businesses are not dealing in just their native currencies. Instead, they need to deal with various currencies on a very regular basis. This is why foreign currency translation becomes something that cannot be avoided. Thus, several methods are designed to ensure a consistent foreign currency translation; and the temporal method example is one among them.

The accounting standards incorporate foreign operations to use the temporal or historical rate method in cases where the native currency differs from the functional currency.

Therefore, a subsidiary of a Canadian company with foreign operations in a small country where all business transpires in U.S. dollars, not the country’s native currency, would use the temporal rate method.

Once you apply the temporal rate method, you update income-generating assets on the balance sheet and profit-and-loss statement items by using the historical exchange rates of transaction dates; or from the date that the organization last assessed the fair market price of the account. You acknowledge this adjustment as current earnings.

Recommended Articles

This article has been a guide to what the temporal method is. Here, we discuss examples of the temporal method and its applications, advantages, and disadvantages. You can learn more about accounting from the following articles –