Part of our Financial Statements guide

What Are Commitments And Contingencies?

Commitment and contingencies are essential financial concepts in any business entity. A commitment is an obligation of a company to external entities that often arises in connection with the legal contracts executed by the company. It is the implied obligation that is expected to occur depending on the outcome of the future event.

Hence, one can say that contingencies are those obligations that may or may not become liabilities to the company because of the uncertainty of the future event. Contingencies, however, are different from commitments. They can affect the organization significantly. They have a probability. that can be estimated reasonably.

- Commitments refer to the obligation to the company’s external parties. It concerns any lawful contract the company makes with external parties.

- Contingencies refer to the company’s obligations depending on the future event’s results.

- In daily life, organizations make contracts to operate business appropriately. But, the organizations must express the warranties in the financial statements for accounting and do not qualify as liabilities. Simultaneously, contingencies are the potential liabilities that happen due to past events. Still, the probability of loss or the actual loss remains undetermined.

Commitments And Contingencies Explained

Commitments are the obligation to the external parties of the company, which arise concerning any legal contract made by the company with those external parties. In contrast, the contingencies are the company’s obligations whose occurrence is dependent on the outcome of specific future events.

Both the above concepts and accounting for commitments and contingencies are equally important for analysts, investors and all other stakeholders and are widely used for evaluating the financial health and risk taking ability of the business. It is necessary to disclose and communicate both contingency levels and external commitments of the business in a clear and transperant manner so that stakeholders get a true and fair picture of the opeartional process and where it stands in the market.

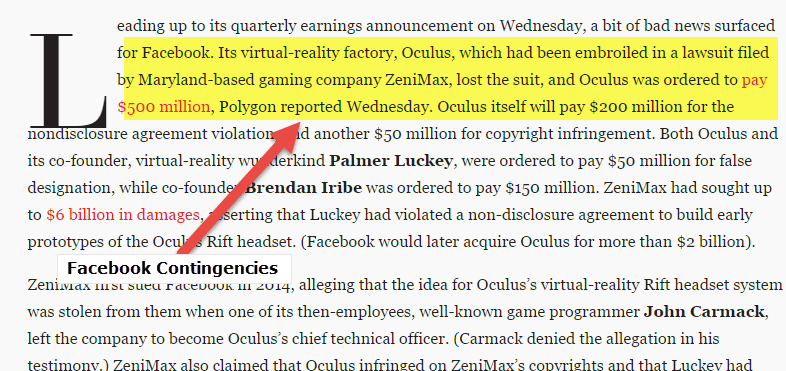

Source: vanityfair.com

As we see above from the snapshot, Facebook virtual reality division Oculus has been in a lawsuit due to allegations of violating the nondisclosure agreement, copyright infringement, and more. In its SEC filings, Facebook has included this lawsuit under the contingent liability section. This article discusses the nuts and bolts of accounting for commitments and contingencies.

What Are the Commitments?

A commitment is an obligation of a company to external entities that often arises in connection with the legal contracts executed by the company. In other words, commitments are potential claims against a company concerning its future performance under a legal contract.

Therefore, one can say that the commitments are those agreements expected to take place in the future. However, if the company hasn’t made any payment for such contracts at the balance sheet date, they are not included on the balance sheet, although they are still considered liabilities. Nevertheless, the company must disclose such commitments along with the nature, amount, and any unusual terms and conditions in the 10-K annual reports or SEC filings. These agreements or contracts may include the following items.

- Short-term and long-term contractual obligations with the suppliers for future purchases;

- Capital expenditure commitment contracted but not yet incurred.

- Non-cancelable operating leases.

- Lease of property, land, facilities, or equipment.

- Unused letters of credit or obligation to reduce debt;

Let us understand commitment through an example. Suppose a company plans to purchase raw material under a predetermined contract. But, as per the agreement, the company will make payments for these raw materials only after these raw materials have been received. Although the company will require cash for these raw materials in the future, the event or transaction hasn’t yet occurred when preparing the balance sheet. Hence, no amount is recorded in the income statement or balance sheet.

However, the company is expected to disclose such transactions as they are supposed to occur in the future and will impact its cash position. Therefore, the company provides an extensive explanation regarding these commitments in the notes to the financial statement.

What Are Contingencies?

Contingencies are different from commitments. It is the implied obligation that is expected to occur depending on the outcome of the future event. Hence, one can say that contingencies are those obligations that may or may not become liabilities to the company because of the uncertainty of the future event.

Let us understand contingencies by the following example. Let’s assume that a former employee sues a company for $100,000 because the employee feels that he has been terminated wrongly. So, does it mean that the company has liabilities of $100,000? Well, it depends on the outcome of this event. If the company justifies the employee’s termination, it may not be a liability to the company. However, if the company fails to justify the termination, it will have to incur a liability of $100,000 in the future because the employee has won the lawsuits.

FASB has recognized several examples of loss contingencies that are evaluated and reported in the same manner. These loss contingencies are as follows.

- The risk of loss or damage to property by fire, explosion, or other hazards;

- The threat of expropriation of assets;

- Actual or possible claims and assessments.

- Pending or threatened litigation.

- Obligation related to product warranties and product defects;

Video Explanation of Commitments and Contingencies

Examples

Let us understand the concept commitments and contingencies on balance sheet and other parts of financial statements with the help of some suitable examples.

Commitment Examples

Example #1

When such commitments are described in the notes to the financial statement, the investors and creditors will get to know that the company has taken a step, and this step is likely to lead to liability. Therefore, the information concerning future commitment remains critical for the analysts, lenders, shareholders, and investors because it provides a complete picture of a company’s current and future liabilities.

Now, let us take a real-life example of a firm and find out its current and future commitments and how they are presented in its financial statements. For instance, AK Steel (NYSE: AKS) has entered into various contracts that obligate the company to make legally enforceable payments. These agreements include borrowing money, leasing equipment, and purchasing goods and services. AK Steel has given detailed information regarding these commitments, as shown in the below graph.

Source: AK Steel

As you have seen in the above snapshot, AK Steel has given an extensive explanation regarding its future commitments or obligation in the notes of the financial statement. The most important point to observe here is that commitments are not shown on the balance sheet despite being the liabilities. It is because commitments need special treatment, and therefore, they are disclosed in the footnotes of the financial statements.

Likewise, AK Steel has given complete information regarding its operating leases. Operating leases are the commitment to pay the future amount. However, it is not recorded as a liability. Instead, the company records it in the annual financial statement or 10-k reports’ footnotes. This disclosure includes items like the length of the lease and expected yearly payments coupled with minimum lease payments over the entire term of the lease. The graph below illustrates AK Steel’s operating lease payments for the lease period.

Source: AK Steel

Another example of commitment could be a capital investment decision that a company has contracted with a third party but hasn’t yet been incurred. For example, AK Steel committed the future capital investment of $42.5 million that it planned to incur in 2017. Although AK Steel has agreed, it has not recorded the amount in the balance sheet in 2016 because it hasn’t yet incurred the investment. Still, it has given a note in the financial statement, as shown below in the snapshot.

Source: AK Steel

Example #2

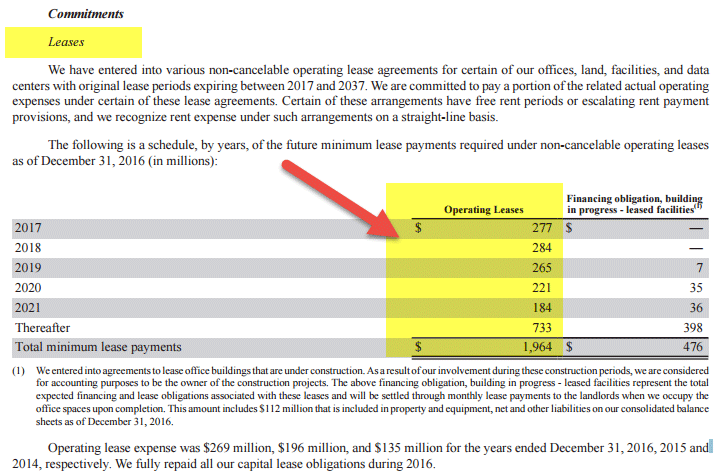

Facebook has primarily two types of Commitments.

#1 – Leases

Facebook has entered into various non-cancelable operating lease agreements for offices, data centers, facilities, etc.

The operating lease expense commitment for 2017 is $277 million.

source: Facebook SEC Filings

#2 – Other Contractual Commitments

Facebook has also entered into non-cancelable contractual payment commitments of $1.24 billion related to network infrastructure and data center operations. These commitments are due within five years.

source: Facebook SEC Filings

As an analyst, it is important to note these commitments as they affect the company’s cash position.

Contingencies Examples

Example#1

Now, let us take a real-life example of contingencies and their reporting in the balance sheet. For instance, Whole Foods Market (NASDAQ: WFM), has recently been involved in class-action lawsuits for its grocery chains. According to the Chicago Tribune, Nine managers were fired by Whole Foods Market due to allegedly manipulating a bonus program. However, these managers filed a class-action lawsuit against Whole Foods Market for not paying bonuses to employees.

As per Foxnews.com, these plaintiffs are now seeking nearly $200 million in punitive damages, among other reliefs. However, WFM is investigating the issues raised by the accusers. Nevertheless, the company has established a loss provision for matters such as these. Although WFM has not shown the amount separately, it has included the loss liability in the other current liabilities in the balance sheet ending December 2016. A snapshot of the fiscal note for commitments and contingencies of Whole Foods Market is given below that discloses the detailed information regarding the probable liabilities.

Source: WFM

Source: WFM

Note – the issue about the termination of employees hasn’t yet been resolved. Therefore, the company hasn’t included the potential loss liability in its balance sheet. In other words, the concerning issue for WFM might be a possible obligation, which is yet to confirm if the current liability could lead to an outflow of resources or present economic benefits such as gaining employee confidence, market presence, etc.

Example #2

Among other contingencies listed in Facebook SEC Filing, the most important is related to Oculus VR inc. ZeniMax Media Inc sued Facebook for trade secret misappropriation, copyright infringement, a break of contract, and tortious interference with Contracts. ZeniMax was seeking actual damages of up to $2.0 billion and punitive damages of up to $4.0 billion. On Feb 1, 2017, when the verdict was announced, Facebook was asked to pay $500 million.

source: Facebook SEC Filings

Reporting Contingencies

Three critical treatments have to be taken care of while reporting contingencies. They are as follows.

- A loss contingency is not recorded in the balance sheet if it is not realized due to improbability. If the likely losses are not more than 50% or the amount is not a reliable measure, they are not recorded on the balance sheet. Meanwhile, the gain contingencies are usually reported in the income statement upon realization.

- A probable contingency can be defined as more than 50% due to a prior obligation.

- If a probable loss can be determined based on historical information, it is considered a reliable measure.

Loss Contingencies

Let us understand loss contingencies through an example. Assuming a company incurs a contingency at the end of year one. The company believes that a loss of $300,000 is probable, but a loss of $390,000 is reasonably possible. However, nothing was settled at the end of year two. When preparing the balance sheet for year two, the company believes that a loss of $340,000 is probable, but a loss of $430,000 is reasonably possible. Finally, at the end of the third year, the company pays $270,000 to the third party to settle the problem. Therefore, the company recognizes a gain of $70,000.

Now let us find out how this gain has been calculated. We know that the company identifies a loss of $300,000 at the end of year one. I have taken $300,000 because it is a possible amount (more than 50%). However, the company expects to recognize an additional probable loss of $40,000 at the end of year two. Therefore, its total possible loss reported at the end of year two is now $340,000. But, at the end of the third year, the company pays only $270,000 to the third party to settle the problem. Thus, it recognizes a gain of $70,000 ($340,000-$270,000).

Gain Contingencies

There are times when companies can gain contingencies. Yet, the reporting of gain contingencies is different from that of loss contingencies. In loss contingencies, losses are reported when they become probable, whereas, in gain contingencies, the gain is delayed until they occur. The following example better illustrates the gain contingencies.

Company A files a lawsuit against company B, and company A thinks it has a reasonable chance of winning the claims. Now, the company’s accountant believes that a gain of $300,000 is probable, but a gain of $390,000 is reasonably possible. Thus, its accountants again believe that an increase of $340,000 is probable, but a gain of $430,000 is reasonably possible. The contingencies get settled at the end of year three, and company A wins the claims and collects $270,000. However, nothing is settled at the end of year two.

We do not include any amount in the income statement in gain contingencies until a substantial completion is reached. In this case, the gain contingencies are $270,000, which company A reports in its income statement at the end of year three. Here, I have taken $270,000 as a contingency because it is the final amount at the end of the completion of the lawsuit.

Disclosure Requirements

A contingent liability, which is probable and the amount is easily estimated, can be registered in both the income statement and balance sheet. The income statement is recorded as an expense or loss, and on the balance sheet, it is recorded in the current liability section. Due to this reason, a contingent liability is also known as a loss contingency. The typical examples of contingent liabilities include warranties on the company’s products and services, unpaid taxes, and lawsuits.

In the case of product warranty liability, it is recorded when the product is sold. The customers can make claims under warranty, and the probable amount can be estimated.

But let us also understand the requirements of commitments and contingencies on balance sheet and other parts of financial statements as per the two accounting standards, the Generally Accepted Accepted Accounting Principles (GAAP) and the International Financial Reporting Standards (IFRS).

GAAP – As per the GAAP, the recording of commitments in the books of accounts are done as and when they happen. But contingencies are recorded or disclosed as notes in the balance sheet while creating the financial statements, provided they relate to some cash outflow in the future or any similar liability. However, if the amount can be estimated and there is a high probability of occurrence of the loss, then it can be recorded in the financial statements.

IFRS – As per the requirements of IFRS commitments and contingencies, all commitments should be recorded in the financial statements as liability of the business during the accounting period in which they occur, and it is compulsory to disclose them as notes to the financial statements. In case the entity is not able to meet the commitment, it should justify its action by disclosing the same again as notes in the financial statements stating the details about the type of commitment, its time, cause, etc. But the business should try their best to meet it, which will exhibit a good image to its stakeholders.

In case of contingencies, they should be shown as notes in the financial statements, which will not depend on the fact that they will result in inflow or outflow of fund or not. The amount can also be recorded in the footnotes if they can be estimated, and the probability of occurrence is high.

However, while recording the IFRS commitments and contingencies both of them in the footnotes of financial statements is necessary to meet the disclosure requirements and obligations of both GAAP and IFRS.

However, let us understand this through an example. An automobile manufacturer debits $2,000 for a car as a warranty expense once it is ready and credits warranty liabilities of $2,000 in the books of account when the car is sold. However, if a car needs a repair of $500 under warranty, the manufacturer will now reduce the warranty liability by debiting the account for $500. In contrast, another account, such as cash, will be credited $500 to the dealers that undertake the repair work. The manufacturer will have left the warranty liability of $1,500 for the new repair under the warranty period.

Why The Disclosure Of Contingent Liability Remains Important For Companies?

We know that contingent liabilities are the future expenses that might incur. Hence, the risk associated with the contingent liabilities is high due to the increased frequency it occurs in day-to-day life. Therefore, the disclosure of contingent liability remains critical for credit rating agencies, investors, shareholders, and creditors because it exposes the hidden risks of the businesses. Besides, contingent liabilities might pose a different risk. For instance, a company may overstate its contingent liabilities. Doing so might scare off investors, pay high interest on its credit, or remain hesitant to expand sufficiently due to fear of loss. Owing to these risks, the auditors keep an eye on the undisclosed contingent liabilities and help the investors and creditors with transparent financial information.

Organizations in day-to-day life enter into contracts to run their business in the best possible manner. But, the organizations have to describe these contracts in the notes of the financial statements for accounting purposes. Thus, these contracts are considered future obligations that do not necessarily qualify as liabilities. At the same time, contingencies are considered potential liabilities that might occur due to past events. However, the likelihood of loss or the actual loss both remains uncertain.

Frequently Asked Questions (FAQs)

What are the disclosure requirements for commitments and contingencies?

The disclosure requirements of commitments comprise the category, amounts, and any not standard terms and commitment uncertainties. A contingency displays a situation concerning a probable loss that may eventually be fixed if one or more future events happen or do not occur.

Why should the auditor be concerned with commitments and contingencies?

The disclosure and acknowledgment of commitments and contingencies provide comprehensive organizational clarity and increase suitable stakeholders’ trust. In addition, the revelations drive the organization with legal and monetary reporting needs.

Why are commitments and contingencies on the balance sheet?

Commitments and contingencies may occur in a few words on the balance sheet, but still, they are essential to the financial statements. In addition, it gives the reader a complete idea about the company’s financial strength. Therefore, it is crucial when contemplating future performance.

Recommended Articles

Guide to what are Commitments And Contingencies. We explain them with the disclosure requirements and examples.