Part of our Financial Statements guide

What is Translation Exposure?

Translation Exposure is defined as the risk of fluctuation in the exchange rate that may cause changes in the value of the company’s assets, liabilities, income, and equities and is usually found in multinational companies as their operations and assets are based in foreign currencies. At the same time, its financial statements are consolidated in domestic currency. Therefore, many companies prefer to hedge such risks in the best possible way.

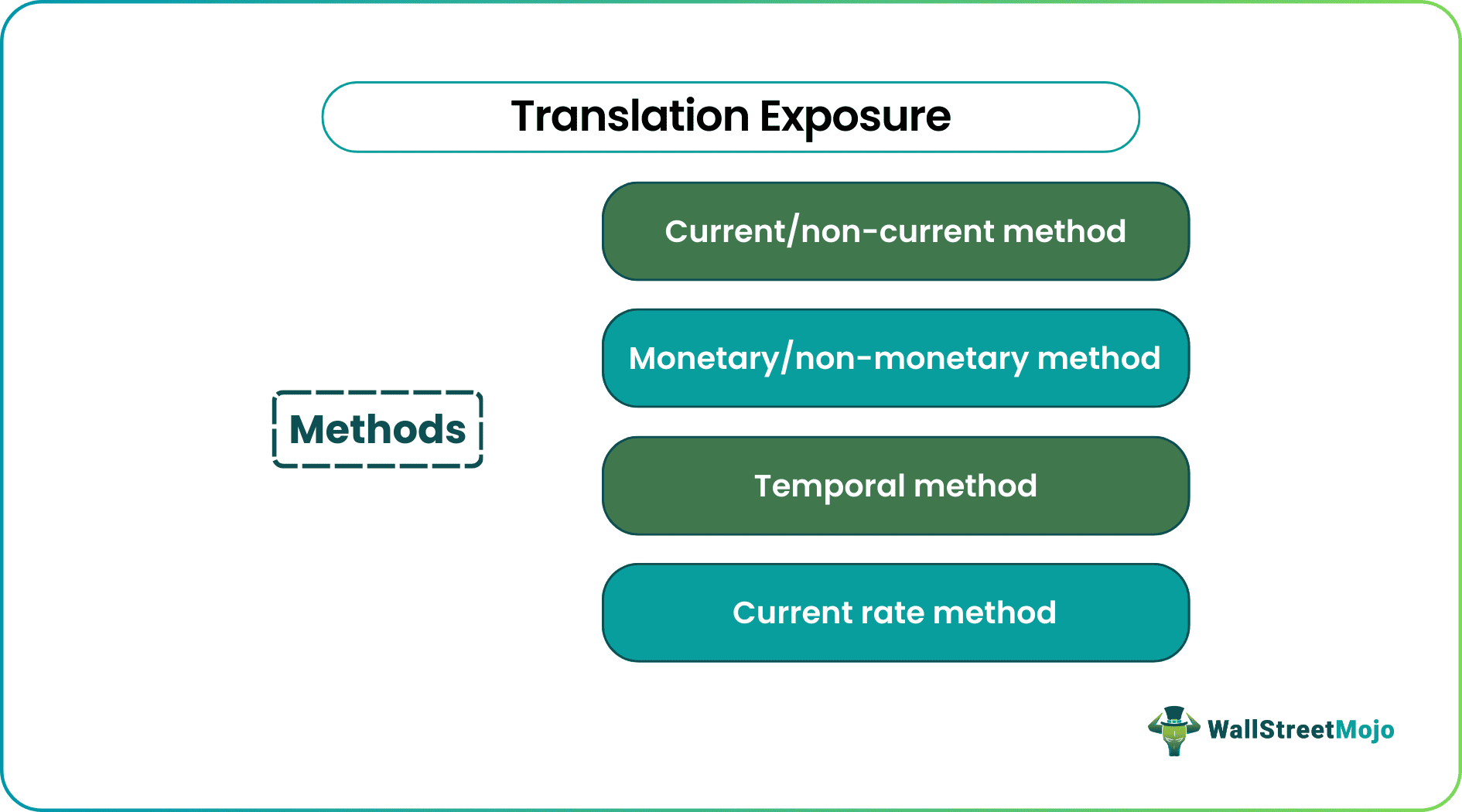

4 Methods to Measure Translation Exposure

#1 – Current/Non-Current Method

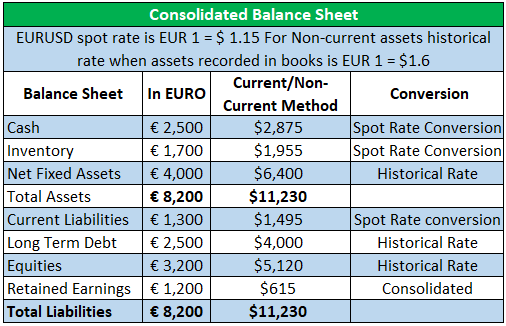

In this method, current assets and liabilities are valued at the currency rate, while non-current assets and liabilities are valued per the historical rate. All amounts from income statements are valued based on the currency exchange rate. In some cases, an approximated weighted average can be used if there are no significant fluctuations over the financial periods.

#2 – Monetary/Non-Monetary Method

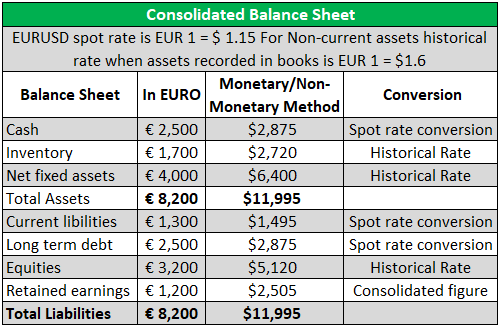

In this method, all monetary accounts in balance sheets such as Cash/Bank and bills payable are valued at the current rate of foreign exchange, while remaining non-monetary items in the balance sheet and shareholder’s equity are calculated at the historical rate of foreign exchange when the account was recorded.

#3 – Temporal Method

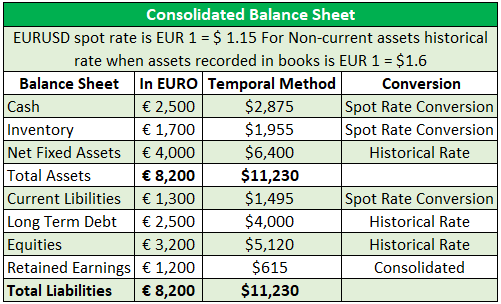

In this method, current and non-current accounts that are monetary on the balance sheet are converted at the current foreign exchange rate. In addition, non-monetary items are converted at historical rates. For example, all accounts of a foreign subsidiary company are converted into the parent company’s domestic currency. The basis of this method is items are translated in a way they are carried as per the firm’s books to date.

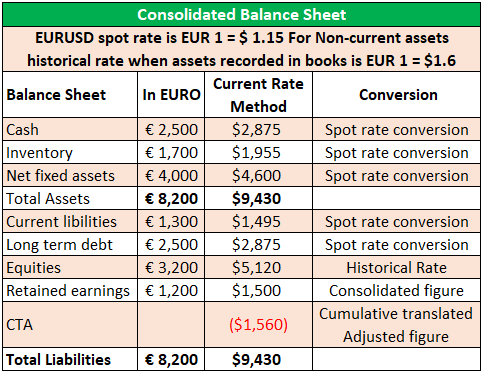

#4 – Current Rate Method

By this method, all items in the balance sheet except shareholder’s equity are converted at the current exchange rate. In addition, all items in income statements are converted at an exchange rate at their occurrence.

Translation Exposure Examples

Company XYZ is a US Company that has a subsidiary in Europe. Since the operating currency in Europe is the EURO.

#1 – Current/Non-Current Method

#2 – Monetary/Non-Monetary Method

#3 – Temporal Method: Continued to translate as per policy.

#4 – Current Rate Method

How to Manage Translation Exposure?

#1 – Balance Sheet Hedge

This method focuses on eliminating mismatches between assets and liabilities in the balance sheet denominated in one currency.

#2 – Derivatives Hedge

The use of derivative contracts for hedging purposes might involve speculation. But, if done carefully, this method manages the risk.

- Swaps: A currency swap agreement between two entities to exchange cash flows in the given period will help manage risk.

- Options: Currency options give the right but not the obligation to the party to exchange a particular amount of currency on a decided exchange rate.

- Forwards: Two entities enter into a contract for the specific exchange rate to settle transactions on a fixed date in the future. All forward contracts are predefined, which manages the risk of fluctuation in the exchange rate but still involves speculation.

Differences Between Translation Exposure vs. Transaction Exposure

| Difference | Translation Exposure | Transaction Exposure |

|---|---|---|

| Definition | The risk involved in reporting consolidated financial statements due to fluctuation in exchange rates; | The risk involved due to changes in the exchange rate, which affects the cash flow movement arises in the company’s daily operations. |

| Area | Legal Requirements and accounting issues; | Managing daily operations; |

| Foreign Affiliate/Subsidiary | It only occurs while consolidating financial statements of parent company and subsidiary or foreign affiliate. | The parent company does not require having a foreign subsidiary for transaction exposure. |

| Profit or Loss | The result of Translation exposure is notional profit or loss. | The result of transaction exposure is realized profit and loss. |

| Occurrence | By the end of every quarter of the financial year while consolidating financial statements. | It only arises at a time of transaction involving foreign currency. |

| Value Impact | The value of the company is not affected. | Since it Directly affects the cash flows of the company, it changes the value of the company. |

| Tax | Translation exposure is more concept instead of an actual impact on the value of the company. Hence it does not affect tax payment and does not provide any benefits in case of loss in terms of fluctuation in the exchange rate. | Since Transaction exposure affects cash flows, it affects the tax payments of the company. Provides benefits in case of loss due to changes in the exchange rate |

Conclusion

- Translation exposure is inevitable for companies operating in other countries than their home country. It is usually a legal requirement for regulators; it does not change cash flow but only changes the reporting of consolidated financials. The translation is done on time of reporting, not at the time of realization, resulting in notional profit and losses.

- Translation exposure poses a threat when presenting unpredicted figures in financial statements in front of shareholders, which might result in questions for the company’s management. Many times such kinds of scenarios occur due to fluctuation in the foreign exchange rate and are considered normal.

- A company trying to mitigate translation exposure has various measurements through hedging and minimizing effect on numbers. To maintain investors’ confidence and avoid any legal hassles, a firm needs to report, manage, and present such exposure.

Recommended Articles

For more on Financial Statements, explore these related articles from our Financial Statements guide.