What is General Purpose Financial Statements?

General-purpose financial statements are the financial statements that are issued by the management at regular intervals, usually, monthly, quarterly, semi-annual, and annual basis. Such statements help investors and creditors interpret the business and financial condition of the company so that they can take informed investment decisions.

Key Takeaways

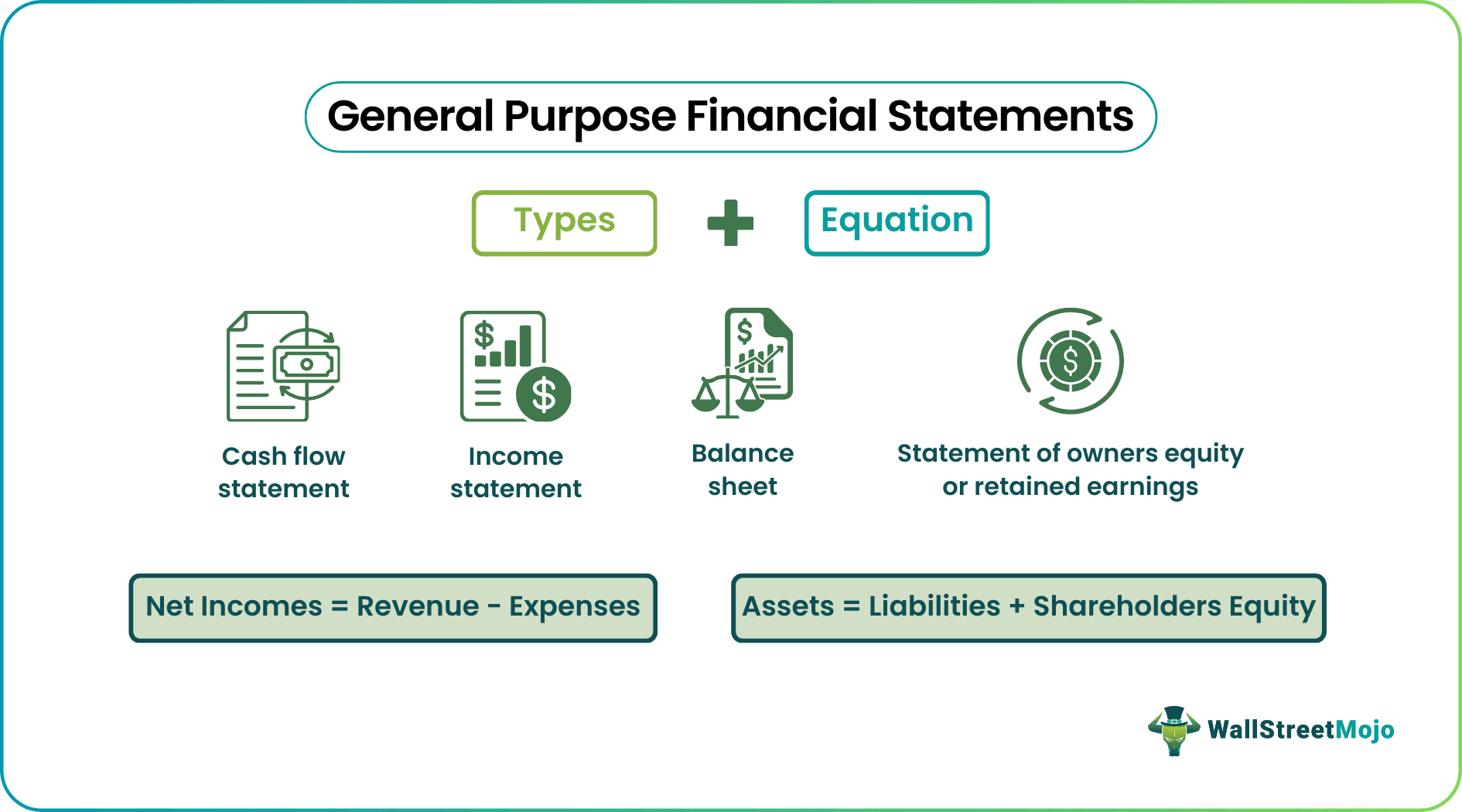

Types of General Purpose Financial Statements

Below are the types of general-purpose financial statements, i.e. cash flow statement, income statement, balance sheet, statement of owners equity or retained earnings.

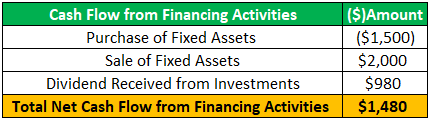

#1 – Cash Flow Statement

- The statement of cash flows describes how a company’s cash inflows and outflows change the company’s cash balance from the beginning of the year to the end of the year. The types of cash flows that cause the cash balance to change are classified into the following three activities, operating activities, investing activities, and financing activities.

- Cash flows fluctuations can be easily traced, thereby controlling the expenditure on unnecessary items and investment in a profitable manner.

Format of cash flow statement given below:

- + / – Operating cash inflows

- + / – Investing cash inflows

- + / – Financing cash inflows

Change in cash flows

- + opening cash balance

- = closing Cash balance

Example:

#2 – Income Statement

- The Income Statement indicates a business’s profitability for a given period of time. By this statement, investors can estimate their return on their investments.

- It is also called a profit and loss account. This statement takes into account all revenue expenses and incomes & required provisions are created for meeting future obligations that have probable nature of occurring losses.

- Based on this statement, the share of profit attributable to the investors is decided by the management according to the investment made by individual investors.

Basic income statement equation is:

Net Incomes = Revenue – Expenses

Example:

#3 – Balance Sheet

The Balance Sheet indicates at a given point of time how a company effectively used its resources. It shows all assets and liabilities at the given point of time.

An accounting equation in the balance sheet is given below:

Assets = Liabilities + Shareholders Equity

Example:

#4 – Statement of Shareholder Equity or Statement of Retained Earnings

The statement of shareholder equity indicates how the shareholders’ ownership in the business, known as shareholder equity or stockholder equity, increased or decreased from the beginning to the end of the given accounting period. As per US GAAP, official term to be used for this statements is a statement of shareholder equity

The statement of shareholder equity equation is:

Beginning Shareholder Equity + Additions to Shareholder Equity – Deductions from Shareholders Equity = Ending Shareholders Equity

Advantages

- Detect Patterns in Market – Financial statements show the market position where it will be identified based on sales fluctuations from period to period. By this management can take necessary steps to improve its standards by employing efficient marketing personnel who suggests product sales improvement.

- Budget Preparation – Financial statements are used for future planning, and decision making is that they show the company’s budgets. There will be estimations and accordingly fix the limits of expenses to be spent in a particular period for a specific project. There are different types of the budget like flexible budget, expenditure budget, fixed budget, etc., these types may be selected according to the need of the entity.

- Reliable – General-purpose financial statements are reliable because an audit of financial statements to be conducted at regular intervals of time, depending on the statutory obligation. For example, banks required to get their accounts audited by chartered Accountant quarterly, annually. Investors rely on financial statements without much analysis when they are audited.

Disadvantages

- Market Demand Fluctuations – Company product demand may frequently vary according to market conditions. By this irregular market fluctuations, sales will have a direct impact. During inflations, sales will have an adverse effect.

- A One-Time Analysis – Financial statements show how company performance at a single point in time. So we cannot compare whether it is doing well or not as compared to earlier years. But we can analyze the financial position over a period of time but not exactly during a short period of time.

Recommended Articles

This has been a guide to What is General Purpose Financial Statements. Here we discuss the types of General-purpose financial statements, objectives along with examples, advantages, and disadvantages. You can learn more about from the following articles –