What Is Credit Risk Management?

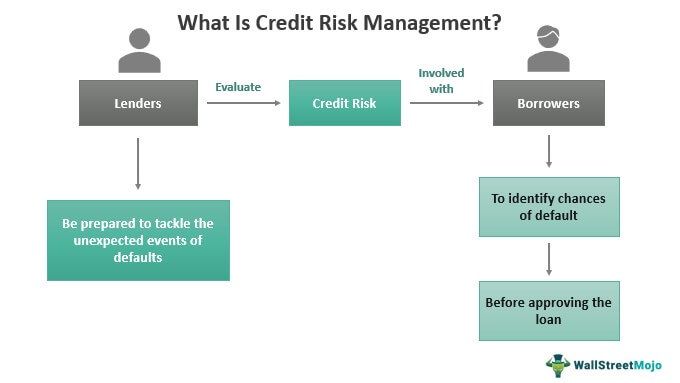

Credit risk management refers to measuring and mitigating the risks associated with the lent amount and being aware of the bank’s reserves to be used at any given time. Risk management here involves facilitating proper decision-making of lenders or banking institutions.

The economic stability of a nation highly depends on the lending business, which becomes a link between the common people looking for investment and the financial market, which runs on this flow of money. The ability of lenders to decide which loan application to approve or disapprove plays a major role in credit risk management.

Key Takeaways

- Credit risk management refers to managing the probability of a company’s losses if its borrowers default in repayment.

- The main purpose is to reduce the rising quantum of the non-performing assets from the customers and to recover the same in due time with appropriate decisions.

- It is one of the important tools for any lending company to survive in the long term since, without proper mitigation strategies, it will be very difficult to stay in the Lending Business due to the rising NPAs and defaults happening.

- Every bank/NBFC has a separate department to take care of the quality of the portfolios and the customers by framing appropriate risk mitigating Techniques.

Credit Risk Management Explained

Credit risk management involves examining a series of steps to ensure the amounts are lent to reliable hands. The lenders are expected to evaluate the loan applications from borrowers thoroughly. In addition, they must ensure that borrowers can make monthly payments in the future.

The lenders must examine their current financial situations and their credit history and score. It builds trust towards the borrowers, who understand whether they can be trusted with the money. Once the borrowers are found creditworthiness, the loan application gets approved. On the other hand, if the applicants are found untrustworthy, the loan application gets disapproved.

The lenders should have an eye for detail to guess it right. Proper evaluation is a must. They have to be particular about the current financial status of the loan seekers, along with being ready for the warning signs that their past credit records indicate to them. The evaluation is normally done concerning the five Cs of credit – character, capacity, capital, conditions, and collateral.

In case the assessment turns out to be wrong, and the possible trustworthy borrowers turn into defaulters, it affects the financial stability of the lending institution, which plays an important role in ensuring the economy’s financial stability.

Steps

From assessing the borrower’s personality through the personal details, they provide to checking on how their property could help them recover the amount in the event of default; the lenders should evaluate everything. Once the evaluation is done, they need to verify and validate details to decide on the approval or disapproval of the loan application.

However, there is more to credit risk management in banks than deciding whether to lend money to an applicant. To help themselves manage Credit Risk well, banking or other lending institutions can check on data sources they are taking information from and validate their reliability. In addition, the institutions can have a third-party entity involved to assess if the models and measures adopted for credit management are proper. They could help them identify the weakness, leading to improvements in the framework.

The third-party unit is the best element to be included in assessing the entire system without bias. They monitor the active models and suggest changes based on their opinion. These entities use the most dynamic datasets to conduct their studies to reach valid conclusions. In addition, they help deploy advanced technology, like artificial intelligence and machine learning, to make risk management more efficient and accurate. As a result, the entities effectively manage credit risks and remain prepared for upcoming financial crimes.

Principles

The strategies can be many, but the basic ones must be incorporated to make the credit risk management tools and framework effective. The first and foremost thing is to have a proper setup to ensure a feasible environment for credit risk assessment. There should be a proper protocol to follow, from assessing the measures to approving them to reviewing them from time to time.

The next thing is to have an efficient credit-granting process. The criteria should be such that the abilities are assessed well. Finally, the capacity must be examined to ensure timely payment of monthly installments.

Thirdly, an administrative framework for measuring and monitoring the process of granting and recovering loans is important. When lenders have a setup to observe and monitor individual credit status, they accurately identify risk-bearing portfolios and prepare for future financial issues.

Fourthly, deploying controls to keep a check on credit risks is important. This includes communicating reviews on current credits to the board of directors and top management officials. This helps in the quick handling of risk-driven portfolios. Lastly, the supervisory bodies must be active to ensure the proper implementation of the policies and strategies.

Examples of Credit Risk Management

Here are the examples to understand how the entire concept works:

Example #1

XYZ Bank believes in helping loan seekers obtain finances for their requirements. Moreover, it keeps the interest rate low, so people do not face trouble repaying them. Thus, the bank allows loans to people belonging to all sections of society once they meet a few minimum criteria.

For fair practice, the lenders deploy an automated system that does not accept the loan application is falling short of those requirements. Hence, they effectively manage credit risks by restricting loan options to those with a certain income level.

Example #2

The lender may insert certain provisions or debt covenants in the loan agreements before disbursing the funds to the borrower. For example, the capital adequacy ratio is one of the most important covenants for Non-Banking Financial Company (NBFC) to maintain up to 15% per the recent RBI guidelines changes in India. If this ratio goes below 155, it would be a regulatory breach for the NBFC, which can seriously affect the Company and its lenders for not monitoring the same efficiently.

Benefits & Challenges

Pros

- Predicting risk becomes easier

- Lenders or banks can plan strategies based on portfolio assessments.

- Credit scoring models tend to be the most effective

- Fraud detection becomes simpler.

Cons

- Improper data management

- Updating details is a frequent affair.

- Insufficient tools for portfolio concentration

- Lack of groupwide risk models

Frequently Asked Questions (FAQs)

What is mortgage credit risk management?

When it comes to mortgage credit risks, the lenders assess the factors affecting the housing market and then determine the risks associated with properly managing it. For example, when the housing market is less active, there are chances of interest rate changes or a falling unemployment rate. In addition, other risks could also affect mortgage financing, including legal, reputation, compliance, etc.

What are the most effective credit risk management strategies?

Some of the most effective strategies to manage credit risks include:

– Efficient data aggregation

– Apt credit-scoring model

– Realistic credit limits

– Streamlined onboarding of customers

– Clear contracts

– Advanced automated systems

Why is credit risk management important?

An efficient management system to check all credit portfolios against risks is important as it helps lenders learn about the creditworthiness of the loan seekers, thereby helping them decide whether or not to approve their loan applications.

Recommended Articles

This has been a guide to What is Credit Risk Management. Here, we explain its steps, principles, examples, benefits, and challenges. You can learn more about Risk Management from the following articles –