What is Overdraft?

An Overdraft is a banking facility that allows customers to withdraw money with a zero balance. Banks offer a loan protecting clients from a bounced check. This facility is chargeable.

A one-time processing fee is charged for this facility. Since overdrafts are a form of loan, account holders also have to pay interest on the overdraft amount. The predetermined limit differs from customer to customer, depending on the relationship with the bank. The customer’s credit history and credit ratings are crucial in determining authorized limits on the amount that can be overdrawn.

Key Takeaways

- An overdraft is a bank credit facility. It lets account holders withdraw or pay a higher amount than what is available in their current or savings accounts.

- There are two basic types of overdrafts – secured and unsecured. While the former requires assurance in the form of collateral, the latter only needs the borrower to hold an account with the lending bank.

- The banks charge a processing fee initially and then impose interest on the sum overdrawn or the borrowed amount.

- It saves the account holder from encountering a bounced check.

How Does Overdraft Work?

An overdraft offers financial freedom to account holders. It aids them in paying off bills even when they are out of funds. It potentially prevents embarrassing situations and helps customers maintain relationships with business parties.

Account-holders can submit a written application with their banks activating this facility. For activating the feature, account holders can either visit their bank physically or apply for the same online. Banks can accept or reject such an application at their discretion. For certain types of accounts, these services are provided by default. When the bank accepts a request, the customer has to pay a one-time processing fee.

This facility differs from other credit options. First of all, the bank declares a specific credit limit for each of its clients. Also, this service is not free; banks impose interest on the overdrawn sum. This interest amount is computed daily. It is important to note that the account holder will only need to pay interest on the borrowed amount and not on the total permissible limit. For this facility, banks do not charge any pre-closure penalty. Additionally, joint account holders are also eligible for this facility by co-applying for the same.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Types of Overdrafts

There are primarily two types of overdrafts – secured and unsecured. A mortgaged asset or collateral always backs the loan, and if the account holder doesn’t pay off the outstanding sum, the bank has the right to recover the loss by selling off this asset. On the other hand, the unsecured type is not secured by any collateral and therefore allows a lower credit limit.

Given below are some of the most common types of overdrafts available:

- Overdraft Against Salary: If borrowers hold a salary account with the lending banks, then they can be eligible for a limit of two or even three times their salary amount.

- Overdraft on Savings Account: The banks also provide this facility for clients who have active savings accounts with frequent transactions.

- Overdraft Against Equity: Keeping the equity as collateral, a borrower can get this facility; however, the permissible limit is significantly less than the market value of those stocks.

- Overdraft Against House: Homeowners can also overdraw upto 40-50% of their house’s value.

- Overdraft Against Fixed Deposit: An account can be overdrawn up to a certain percentage of a fixed deposit. Generally, the interest rate on such credits is 2% higher than the Fixed Deposit’s ROI.

- Overdraft Against Insurance Policy: The facility can also be availed on the grounds of an insurance policy depending upon its surrender value.

Overdraft Protection

Overdraft protection is the next level of assistance offered by banks. It links checking accounts to other bank accounts. There could be a second checking account, a savings account, a line of credit, or a credit card. Thus, whenever the checking account is overdrawn, the bank pools in money from the linked account. The bank uses funds from alternate accounts to clear a check. In order to avail such protection, customers need to apply specifically.

Again, the bank imposes a protection charge. While the fees vary from bank to bank, this facility protects the customer from non-sufficient funds (NSF) charges. Banks keep an eye on the number of times the protection is used. If the protection is used repeatedly, the facility will be discontinued.

Overdraft Fee

Initially, banks charge a one-time processing fee. Thereafter, the bank makes payments even when there is a shortage of funds. On top of the initial fee, a certain percentage is charged as interest on the deficit sum. This interest varies from bank to bank. Also, the one-time processing fee can be charged multiple times if a customer keeps making payments with an insufficient account balance. However, there is a per-day limit for the processing fee.

In the US, while Ally Bank and Alliant Credit Union don’t levy any coverage fee when customers overdraw from their accounts. The top financial institutions like Capital One 360 and Bank of America impose $35 for this option. The fee can be charged a maximum of 4 times a day. At $38, BBVA and Comerica charge the highest. This fee can be charged six times a day.

Advantages

This facility can protect the customer’s reputation. Given below are the various advantages of availing of this option:

- Prevents Check from Bouncing: This option prevents checks from getting bounced. Consequently, the customer can maintain fair credit ratings with a clear payment record.

- Timely Payments: It also assists account holders in disbursing pending payments on time. This way, customers avoid any dues or delayed remittances, despite having a nil balance.

- Ease of Application: An account holder can opt for this option by filling a simple form by visiting the respective bank or doing it online on the bank’s portal. The facility requires minimal paperwork.

- No Pre-Closure Charges Applicable: Unlike other loans, this facility does not impose any early payment penalty on the account holder.

- No Collateral in Unsecured Overdraft: In some cases, banks don’t ask for any asset, mortgage, or collateral at all. All it takes is an existing account with the respective financial institution.

- Minimal Interest: The bank charges interest only on the sum that has been overdrawn. This too is incurred only till the amount is repaid.

- Flexibility and Convenience: It is a beneficial option considering emergencies. It provides flexibility in financial planning.

Disadvantages

This facility mandates having a bank account with the respective financial institution. Also, this option is charged with a high-interest rate, much higher than other loan options. Moreover, account holders end up paying penalties for overdrawing beyond the permissible limit. If account holders fail to pay back the due amount in the allowed time frame, credit ratings are brought down.

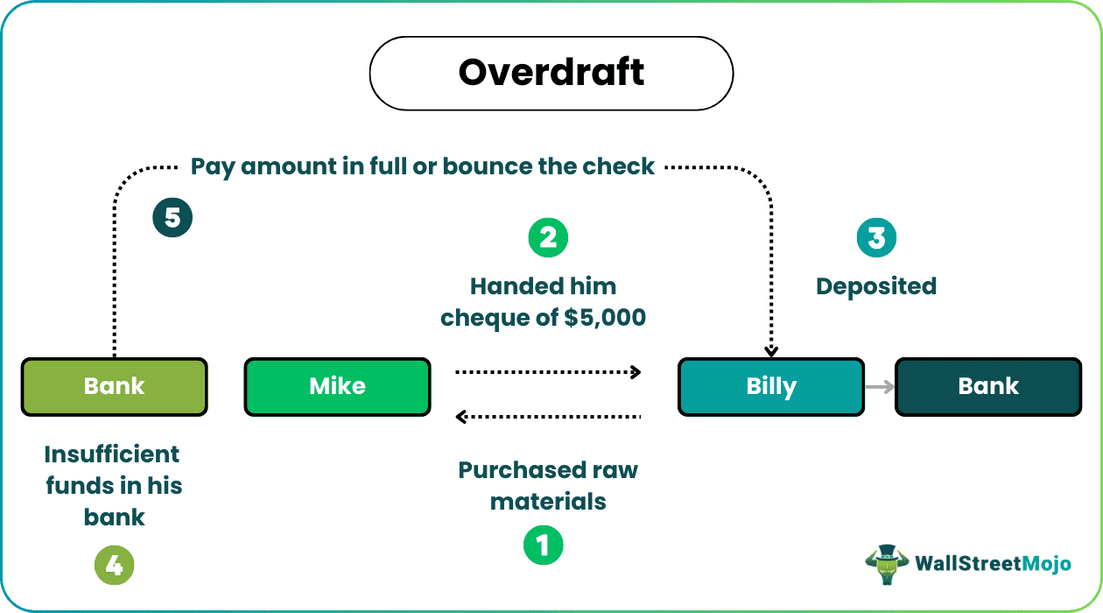

Overdraft Example

To better understand overdrafts, consider the following example.

Mike purchased raw materials from Billy and handed him a check of $5,000. Billy then deposited the check at a bank. Mike had insufficient funds. Since Mike had an account balance of $4,000, he was short by $1,000.

In this case, there are two probable outcomes. Mike’s bank can pay billy the amount in full, or check bounces on account of insufficient funds. If the bank extends credit to Mike, preventing the check from bouncing, he will be charged interest on the $1,000.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

What does overdraft mean?

It is a banking facility that offers short-term credit to the account holders by allowing them to withdraw money from their savings or current account even if their account balance is insufficient. It is a form of credit provided by a banking institution to ensure their clients’ uninterrupted payments and fund withdrawals. However, there are limits on the amount that can be overdrawn.

Do overdrafts affect credit score?

Overdrawing does not harm the customers’ credit scores unless they fail to reimburse the outstanding amount on time. This includes the interest. Instead, it saves the account holders from ruining their credit scores with a bounced check. Checks can bounce without the customer even being aware of insufficient funds. This facility protects customers from such oversights.

How does an overdraft get paid back?

If a customer overdraws from their account, the amount can be repaid by depositing the due amount in the bank account. This includes the sum overdrew and the applicable interest payable on it.

Recommended Articles

This has been a guide to overdraft and its meaning. Here we discuss overdraft protection, types, fee, examples, advantages, disadvantages, and how it works. You can learn more from the following articles –