Part of our Financial Planning guide

What Is Financial Independence?

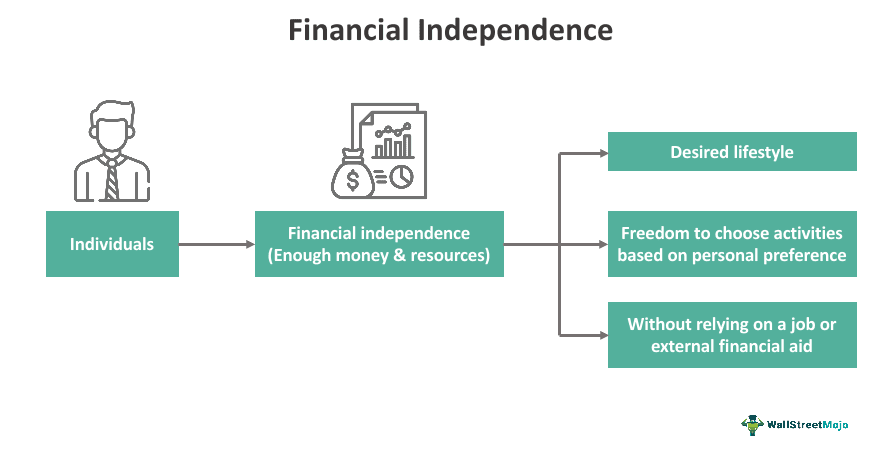

Financial independence is a state where an individual or household has enough financial resources to cover expenses and maintain a desired lifestyle without relying on employment or income. It allows individuals to choose and pursue personal goals without being constrained by financial obligations or paycheck requirements.

Financially independent people have more security, freedom, and flexibility in their lives. They can manage their money, follow their interests, and have a work-life balance. It lessens dependency on other revenue sources and acts as a safety net against monetary difficulties. Planning for retirement and living a happy, stress-free life are also made possible through it.

- Financial independence grants individuals the freedom and flexibility to live on their terms without being constrained by financial obligations or paycheck requirements.

- Financial independence involves setting clear goals, creating a budget, reducing debt, saving and investing wisely, diversifying investments, and seeking professional guidance.

- It offers freedom, reduced stress, personal goals achievement, early retirement, and financial security. Disadvantages include requiring time, effort, short-term sacrifices, market volatility, limited social safety nets, and unexpected challenges.

- There is no single financial independence formula, but various methods, like the 50/30/20 rule, can be used as guidelines.

Financial Independence Explained

Financial independence refers to attaining financial adequacy, enabling individuals or households to live their desired lives and pursue their goals and aspirations. It’s common to view financial independence as an individual objective. It is about being free to live life without restrictions and financial obligations. It is also about having enough money to pay bills and have money for additional needs.

Financial independence allows individuals to manage their time effectively and make informed decisions about their spending habits. It involves having sufficient funds to live a desired life without a job, with savings and investments potentially providing income for the rest of one’s life. There are multiple ways to accomplish this. One such technique is the 50/30/20 rule of budgeting. It permits the following distribution of after-tax income: 50% for wants like clothes and entertainment, 30% for requirements like housing, water and food, and 20% for debts, savings, and other financial objectives.

Steps

Some of the steps through which an individual can become financially independent are given as follows:

- Setting Clear Goals: It’s important to define individual financial objectives and establish specific targets to work.

- Creating a Budget: It is essential to track income and expenses and establish a budget that aligns with individual goals.

- Reducing Debt: Prioritizing paying off high-interest debts and systematically planning to eliminate other liabilities helps clear the path to investing.

- Saving and investing: Developing the habit of saving a portion of income and investing it wisely to generate passive income will help individuals maintain their income levels.

- Additional sources of income: Exploring opportunities to boost income, such as side hustles, freelancing, or entrepreneurship, can help individuals reach goals faster.

- Building an Emergency Fund: Setting aside funds to cover unexpected expenses or financial emergencies.

- Maximizing Retirement Contributions: regular contributions to retirement accounts shall be made to ensure long-term financial security.

- Diversification of Investments: Spreading investments across different asset classes helps to minimize risk and maximize returns.

- Reviewing and making timely adjustments: This step involves regularly reviewing financial plans and tracking progress. Also, adjustments as needed to stay on track toward financial independence shall be made.

- Seeking Professional Guidance: Consulting with financial advisors or other professionals who can provide expertise and guidance on achieving financial independence can make the journey easier.

- Practicing Discipline: Cultivating disciplined financial habits, avoiding unnecessary expenses, and making conscious choices aligned with individual long-term goals are critical in the journey toward financial independence.

- Staying Committed: Recognize that financial independence is a long-term journey; stay focused and committed to financial plans.

Additionally, it helps to stay informed about personal finance, investment strategies, and financial management.

Examples

Let us look at a few examples to understand the concept better.

Example #1

Let’s say Daisy, a recent college graduate working as an accountant, is planning to build financial independence. Daisy creates a budget to track her income and expenses, establishes an emergency fund to cover unexpected expenses, and pays off student loans and credit card debt. She uses a financial independence calculator for the same. She enrolls in her company’s retirement plan and contributes a portion of her salary, taking advantage of employer-matching contributions.

Daisy also explores passive income opportunities, such as investing in dividend-paying stocks and real estate properties. She is also an online tutor, which brings her additional income after office hours. Daisy continuously learns about personal finance and investing strategies, making informed decisions. She invests in low-cost index funds to benefit from long-term market growth. Daisy also pursues career growth by pursuing professional certifications and seeking promotions or higher-paying positions.

Example #2

A real-life study was conducted regarding factors that are associated with financial independence.

This study aimed to examine the factors that impact the financial independence of young adults aged 18-23 in the United States. The study proposed that economic, psychological, and family-related factors significantly determine financial independence. The data utilized for this study were obtained from the 2009 Transition into Adulthood data set and the 2009 Panel Study of Income Dynamics.

The study’s findings indicated that economic factors, such as income, assets, work status, and educational attainment, positively influenced financial independence among young adults. Additionally, psychological factors, including economic self-efficacy, money management skills, and problem-solving abilities, positively contributed to financial independence. On the other hand, family economic factors, such as parental income, stock holdings, and financial assistance, were identified as factors that decreased financial independence among young adults.

Furthermore, the study revealed that young adults who had completed college exhibited higher levels of financial independence. This was when compared to individuals who had never attended college or were currently enrolled but had not completed their studies. However, there were no significant differences in financial independence between college graduates and individuals who had dropped out of college.

This study’s findings have implications for consumer educators, suggesting the need to develop targeted financial education programs specifically tailored for young adults aged 18-23. By addressing the identified factors that influence financial independence, these programs can better equip young adults with the necessary skills and knowledge to achieve greater financial autonomy.

Advantages & Disadvantages

Some of the advantages and disadvantages are given as follows:

Advantages

- Freedom and Flexibility: Gain control over financial decisions, enabling the pursuit of a desired lifestyle.

- Reduced Stress: Attain financial peace of mind by eliminating money-related worries.

- Personal Goals: Have the freedom to prioritize personal passions and interests without financial constraints.

- Early Retirement: Achieve the possibility of early retirement for a longer period of leisure and fulfillment.

- Financial Security: Enjoy a sense of security with the ability to handle unexpected expenses and maintain a comfortable living standard.

Disadvantages

- Time and Effort: Building financial independence requires disciplined, long-term efforts in saving, investing, and planning.

- Sacrifices: Often involve short-term sacrifices, such as delayed gratification or cutting back on certain expenses.

- Market Volatility: Investing for financial independence exposes individuals to market risks and fluctuations that can impact returns.

- Limited Social Safety Nets: Relying solely on personal resources reduces dependence on social safety nets, potentially affecting support during unforeseen circumstances.

- Unexpected Challenges: Despite careful planning, unforeseen events like medical emergencies or economic downturns can impact financial independence, requiring plan adjustments.

Frequently Asked Questions (FAQs)

1. Why financial independence is important?

Financial independence is crucial as it allows individuals to make choices aligned with their goals, reduces stress, and ensures security. It enables a lifestyle based on personal preferences rather than financial obligations, fostering long-term well-being.

2. What is financial independence vs financial freedom?

Financial independence signifies having enough resources to cover living expenses. In contrast, financial freedom extends to having surplus funds for discretionary spending and indulging in non-essential activities, offering higher financial flexibility.

3. What is the FIRE movement?

The FIRE (Financial Independence, Retire Early) movement is a lifestyle choice emphasizing aggressive saving and investing to achieve early financial independence, allowing individuals to retire early and pursue personal goals, passions, and experiences. It centers on frugality, strategic investment, and intentional living.

Recommended Articles

This article has been a guide to what is Financial Independence. Here, we explain its examples, steps, advantages, and disadvantages. You may also find some useful articles here –