Part of our Types of Audit guide

What Is Auditor Independence?

Auditor independence refers to the impartiality and objectivity of an auditor in conducting an audit, free from conflicts of interest and bias. It aims to increase public confidence in financial reporting by ensuring that the auditor’s opinions and assessments are unbiased.

It aims to maintain the professional integrity of the auditing profession by avoiding situations that could compromise the auditor’s impartiality. It increases the credibility of the financial statements and enhances their usefulness for stakeholders.

- Auditor independence is crucial for ensuring the quality and reliability of financial reporting, protecting investors, promoting transparency and accountability, and maintaining public confidence in the financial reporting process.

- Auditors must follow ethical standards, such as those outlined in the Sarbanes-Oxley Act, to maintain their independence and ensure the quality of financial reporting.

- Auditors must issue an opinion on the financial statements, which provides the reliability of the financial reporting process.

Auditor Independence Explained

Auditors’ independence enables the auditor to ensure that balance sheets are carefully and unbiasedly audited, giving stakeholders reliable data on the company’s financial performance. Auditors must avoid having intimate financial and personal ties to their clients to retain their independence, including refraining from taking gifts or loans from them or investing in their shares. It also provides a foundation for high-quality financial reporting and increases public confidence in auditing.

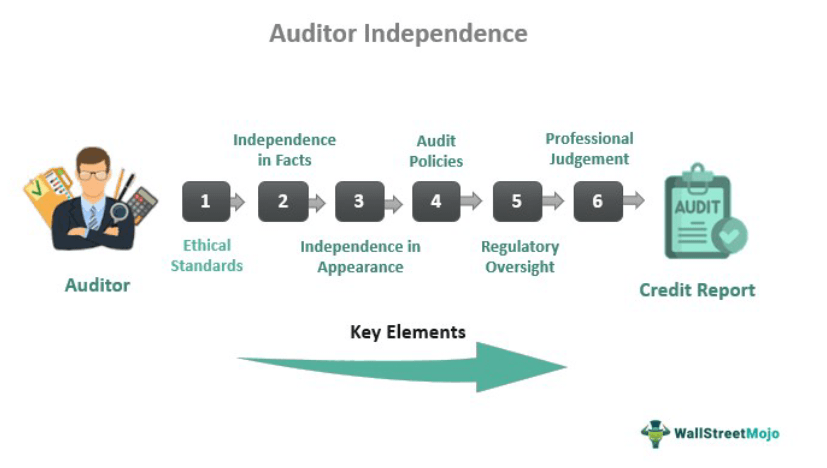

It includes the following elements:

- Ethical Standards: Auditor independence standards, such as the International Ethics Standards for Professional Accountants, must be met to maintain impartiality and objectivity.

- Independence in Fact: Auditor independence in facts is a must, meaning they cannot have a financial interest in the company they are auditing and must avoid relationships that compromise their impartiality.

- Independence in Appearance: Auditor independence in appearance avoids situations that lead others to believe they are not impartial. For example, auditors must not have close personal or business relationships with company management.

- Audit Firm Policies: Audit firms have policies to ensure auditor freedom, such as rotations of auditors, restrictions on non-audit services, and limitations on business and personal relationships.

- Regulatory Oversight: Regulators, such as the U.S. Securities and Exchange Commission (SEC) in the United States, monitor and enforce such independence through inspections, enforcement actions, and professional standards.

- Professional Judgment: Auditors use their professional judgment to assess their independence in each audit engagement and must take steps to ensure their impartiality is not compromised.

Rules

The rules of auditor independence vary by jurisdiction but generally include the following:

- Prohibition of Non-Audit Services: Auditors are generally restricted from providing non-audit services to the clients, such as tax services, consulting, or management functions, to avoid conflicts of interest.

- Limitations on Business Relationships: Auditors must avoid close business relationships with their audit clients, such as joint ventures, partnerships, or interlocking directorates.

- Independence in Fact: To avoid conflicts of interest, auditors must not have a financial interest in their audit clients, such as owning stock or having a loan relationship.

- Independence in Appearance: Auditors must avoid situations that would lead others to question their integrity, such as close personal relationships with management or providing preferential treatment.

- Rotation of Auditors: Some jurisdictions require the process of auditors after a certain number of years to promote independence and prevent auditor-client relationships from becoming too personal.

- Professional Standards: Auditors must follow professional standards, such as International Standards on Auditing, to maintain their independence.

- Regulatory Oversight: Regulators, such as the SEC in the US, monitor and enforce auditor independence through inspections, enforcement actions, and professional standards.

Examples

Let us understand it in the following ways.

Example #1

Suppose Amacon Company hires FinFix Auditing Firm to perform its annual audit. During the audit, Amacon Company’s CEO approaches the lead auditor and asks him to provide non-audit services, such as tax preparation, in addition to the audit work. The lead auditor recognizes that providing non-audit services to the same client creates a conflict of interest. Accordingly, he informs the CEO that the auditing firm has policies prohibiting auditors from providing non-audit services to their clients.

By declining the non-audit services, the lead auditor maintains his independence and integrity. He also demonstrates the importance of following ethical standards and policies to ensure the quality of the audit and the credibility of the financial statements.

Example #2

A real-life example of auditor independence is the Enron scandal. Enron’s auditor, Arthur Andersen, was accused of failing to maintain its integrity while auditing its financial statements. Despite numerous red flags, including the use of off-balance-sheet entities, Arthur Andersen signed off on Enron’s financial statements, which turned out to be fraudulent. The scandal led to the company’s collapse, the accounting firm’s downfall, and increased scrutiny of auditor independence.

Importance

Auditor independence is essential for several reasons:

- High-Quality Financial Reporting: An independent auditor assures the financial statements are accurate, complete, and free of material misstatements. It helps increase confidence in the financial reporting process. It also provides stakeholders with the information they need to make informed decisions.

- Investor Protection: Independent auditors check corporate management and help prevent financial crime and management. It helps to protect investors and increase the overall transparency and accountability of the financial reporting process.

- The credibility of Financial Statements: An independent auditor’s opinion on the financial statements adds credibility to the financial information. It helps companies access capital markets and secure funding.

- Public Confidence: Independent auditors assure the public that the financial reporting process is credible, transparent, and trustworthy. It helps to maintain the public’s confidence in the financial reporting process.

- Regulation Compliance: Independent auditors help companies comply with regulations and reporting requirements. It helps ensure financial information’s quality and reliability.

Internal And External Auditor Independence

Internal Auditors are the company’s employees. They are responsible for performing audits within the organization. They are typically responsible for identifying and assessing the organization’s risks and recommending improvements to the company’s internal controls.

External Auditors, on the other hand, are independent third-party professionals the company hires to audit its financial statements. They assure stakeholders, such as investors and regulators, that the financial statements are accurate, complete, and free of material misstatements.

The main differences between internal and external auditors are as follows:

- Purpose: Internal auditor independence focuses on improving the efficiency and effectiveness of the organization’s operations. At the same time, external auditors focus on assuring stakeholders of the reliability of the financial statements.

- Objectivity: Internal auditors are company employees and are under the influence of management. In contrast, external auditors are independent third parties who maintain neutrality in their work performance.

- Scope: Internal audits may be broader, covering operations, risk management, and internal controls. In contrast, external audits focus on financial statements and related disclosures.

- Reporting: Internal auditors report their findings and recommendations to management. In contrast, external auditors issue stakeholders an opinion on the financial statements.

Frequently Asked Questions (FAQs)

What are the five critical requirements for auditor independence?

Companies and auditors must ensure that all standards are per the charter. Code of Ethics, Independent Period, General Independent Documentation of Audit and Review Involvement, and non-assurance services provided to an assurance client.

How to improve auditor independence?

It reinforces when the audit team appoints auditors and serves as the primary overseer of the audit function.

What are the threats to auditor independence?

It includes self-review threats, self-interest threats, multiple referral threats, ex-staff and partner threats, advising, and related threats.

Recommended Articles

This article has been a guide to what is Auditor Independence. We explain its rules, importance, examples, and comparison with internal auditor independence. You may also find some useful articles here –