Part of our Types of Audit guide

Internal Audit Meaning

Internal audit checks how well a company maintains operational efficiency and manages accounting processes while complying with its standard rules and regulations. Conducting audits from time to time ensures the firms are strict enough in following the administrative fundamentals and sticking to a maximum accuracy rate so far as financial reporting is concerned.

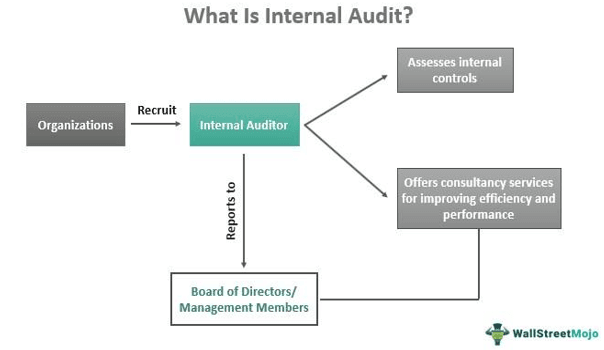

An internal auditor is appointed to check the overall performance of different companies with respect to the administrative, executive, financial, and legal standards they follow. The audit effectively identifies corporate frauds while assessing the internal controls to ensure a business’ efficiency.

- Internal audit is a process through which the companies get to know the loopholes in the system and improve the respective aspects for making businesses more efficient.

- Companies recruit auditors to acquire certification from a popular internal audit institute to check its different business activities and offer consultancy services.

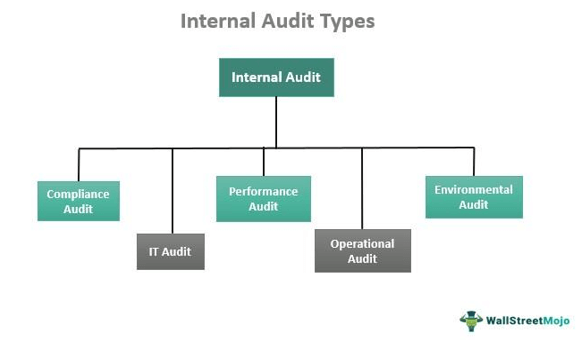

- Compliance, IT, Performance, Operational, and Environmental audits would be a few commonly found internal audits.

- It is different from external audits in which auditors validate the accuracy of the financial documents and send reports to stakeholders and other external members associated with the organization.

Understanding Internal Audit Process

An internal audit is conducted to properly check whether a company follows the internal protocols, regulations, and standards. Every organization has a specific set of rules to follow. The companies, therefore, have an auditor acquiring internal audit certification to ensure the employees and top officials abide by all of them for legal and operational efficiency.

Conducting audits internally helps the management identify if anything wrong in an organization. The financial reports and data collection methods are studied to see if the firms are impartial in applying different means to achieve their corporate goals.

These audits have become more significant, especially after the Sarbanes-Oxley (SOX) Act of 2002, which holds managers responsible for the rights and wrongs in a company’s financial statement. Once the audits go smooth, the management prepares accordingly for the external audit.

In India, the Institute of Chartered Accountants of India (ICAI) has a separate Committee for Internal Audit, which assesses the required compliance as made mandatory under Section 138 of the Companies Act, 2013.

Types of Internal Audit

Audits conducted internally assess firms based on a wide range of parameters. Depending on these determinants, such audits are classified into different categories. These include:

#1 – Compliance Audits

An internal auditor checks whether the company complies with the rules, regulations, and laws of the region, state, or country it operates. In case of non-compliance, firms are subject to payment of fines and penalties or other punishments. As far as the compliance audit is concerned, companies must stick to Foreign Corrupt Practices Act (FCPA) or General Data Protection Regulation (GDPR).

#2 – IT Audits

The Information Technology audits include the assessment and evaluation of the technological infrastructure. The auditor, in this case, checks if the hardware and software equipment is processing requests and operating properly. This audit covers the cyber issues that might require immediate attention. In addition, the professional examines the general IT controls, system operation, and backup-recovery processes.

#3 – Performance Audits

While conducting this type of audit, the auditor ensures that the companies’ standards and core competencies are efficiently met. The management sets these standards, expecting employees and the overall workforce to strengthen their performance while remaining compliant with the standards and regulations.

#4 – Operational Audits

The operational auditors are accountable for issues with the company’s operational infrastructure. They check how efficiently a business works to achieve its set output. Starting from quality control, accounting controls to human resources function, they assess every aspect of the company. In addition, they also offer advice and guidelines to improve the operational procedures to enhance the company’s efficiency and effectiveness.

#5 – Environmental Audits

Having an eco-friendly environment is a must for any company. When an auditor is asked to conduct environmental audits, they see that the premises do not violate any environmental laws or policies.

Internal Audit Functions

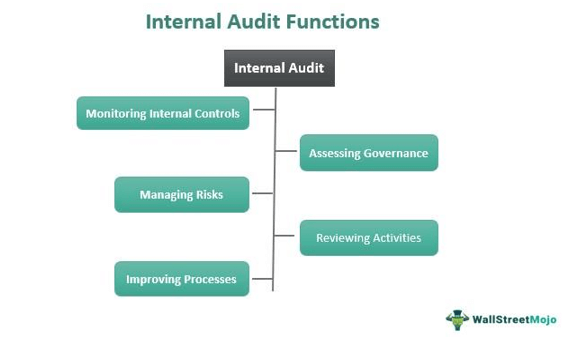

These audits can be conducted daily, monthly, quarterly, or annually, given how frequently the directors want the companies to be inspected and supervised. The main motives behind conducting the audits internally are:

- Through this audit, auditors monitor internal controls to ensure that the accounting processes are effectively conducted and the accuracy is maintained in the released financial reports.

- The internal audit manager checks governance to ensure companies do not compromise their ethical values. They see if the firms in question adopt fair practices for a growing business.

- Risk management is easier as the audits conducted internally also involve auditors’ consultancy services whereby they identify the loopholes and let the businesses improve their standards and become more efficient.

- Auditors review the activities, be it human resources procedures or operating activities, or compliance with laws and regulations. They examine the means used to measure the financial and other information. The auditor may make inquiries about transaction balances and other specific matters.

Example

Company A presents its financial report to the board of directors for the current year. Stella, the finance director, raises concerns over the discrepancies in the invoices. She notices the mismatch between invoices and puts a lot of questions. As it was an internal audit, the company gets a chance to improve the system to ensure it passes through the next audits successfully.

Internal Audit vs External Audit

While internal audits are conducted to examine and improve the efficiency of businesses, external audits validate and assure the accuracy of the financial reports. Besides this, there are other differences too that have been listed below:

| Category | Internal Audit | External Audit |

|---|---|---|

| Objective | Enhances the efficiency of a business by identifying loopholes and advising means to improve accordingly | Makes financial reports reliable |

| Reports to | Board of Directors or higher officials | Stakeholders or external members of the organization |

| Covers | Detects all kinds of risks an organization is likely to face | Identifies finance-related risks and issues |

| Consultancy services | Guides organizations to improve their processes and functions in accordance with the issues and risks identified | Not responsible for giving any improvement advice. |

Frequently Asked Questions (FAQs)

What is an internal audit?

It refers to the audit conducted to evaluate and improve the risk management effectiveness in the company, examine different internal controls followed in the company and ensure that the company is complying with all applicable laws and regulations.

Is internal auditing a good career?

Yes, it is a good career as it offers a prestigious opportunity for individuals to earn and grow simultaneously.

What do internal auditors do?

These auditors examine and identify the issues with companies’ processes, starting from the accounting department to its HR and legal division. In addition, they also offer consultancy services to firms and make sure they improve in the aspects they are lacking.

Recommended Articles

This article is a guide to Internal Audit and its definition. Here we explain the process of internal auditing along with its types, functions, and example. You can learn more about accounting from the following articles –