Part of our Types of Audit guide

What Is Agreed Upon Procedures (AUP)?

Agreed Upon Procedures (AUP) is a type of engagement in which an independent auditor performs specific procedures agreed upon with the client. These procedures are designed to meet the client’s particular needs and are tailored to address specific areas of concern.

It serves various purposes, such as compliance with regulatory requirements, due diligence in mergers and acquisitions, or evaluation of internal controls. The procedures are an agreement between the auditor and the client or prescribed by a regulatory body or industry standard.

- Agreed Upon Procedures engagements involve the auditor performing specific procedures agreed upon with the client.

- The operations performed are usually limited to a particular area of concern or risk.

- The scope and objectives of the engagement are tailored to the client’s specific needs.

- The resulting report must provide an overall opinion or assurance on the financial statements or other information.

Agreed Upon Procedures Explained

Agreed Upon Procedures can help organizations improve their processes, identify areas of risk or weakness, and provide stakeholders with confidence in the accuracy and reliability of the reported information. They can also help organizations comply with regulatory requirements and evaluate internal controls, providing a valuable risk management and assurance tool. It can be necessary for a business organization in several ways:

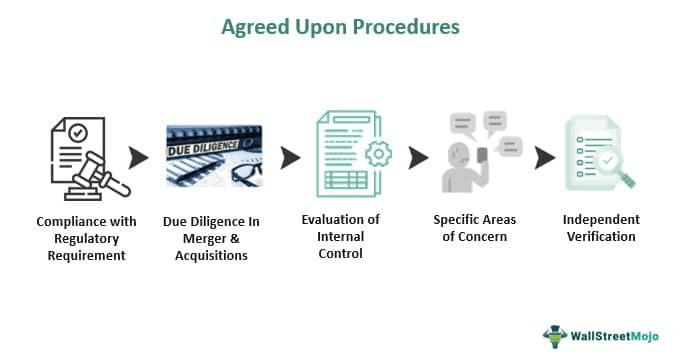

- Compliance with regulatory requirements: It can help organizations comply with regulatory requirements by verifying that regulatory standards handle specific processes or data.

- Due diligence in mergers and acquisitions: Agreed-upon procedures audit can provide independent verification of data and processes during mergers and acquisitions, helping to identify potential risks and liabilities.

- Evaluation of internal controls: It can be used to evaluate internal controls, identifying weaknesses and opportunities to improve the organization’s processes.

- Specific areas of concern: It can be tailored to address particular areas of concern within the organization, providing targeted insights into areas of risk or weakness.

- Independent verification: It provides an independent guarantee of specific data or processes, giving stakeholders confidence in the accuracy and reliability of the reported information.

Checklist

The specific checklist of agreed-upon procedures in a business organization will depend on the nature and scope of the engagement, as well as the particular needs of the client. However, some standard procedures in its checklist are:

- Identify the scope of the engagement and the specific procedures.

- Verify the accuracy and completeness of financial data and other records.

- Check compliance with specific laws, regulations, and internal policies.

- Review specific contracts, agreements, or other legal documents.

- Confirm the accuracy and completeness of inventory and other assets.

- Check the accuracy and completeness of accounts payable and accounts receivable.

- Review the effectiveness of internal controls and identify any weaknesses or deficiencies.

- Verify the accuracy and completeness of tax filings and related records.

- Confirm the accuracy and completeness of payroll records and related payments.

- Evaluate the accuracy and completeness of financial statements and related disclosures.

- Verify the accuracy and completeness of vendor and supplier contracts and related payments.

- Confirm the accuracy and completeness of customer contracts and related payments.

Examples

Let us understand in the following ways.

Example #1

Suppose an online retailer is concerned about the accuracy of their inventory data and decides to commission such engagement. The retailer wants to ensure that their inventory data is accurate and complete and that its internal controls for managing inventory are adequate.

The auditor performs the following procedures as part of the engagement:

- First, review the retailer’s inventory records and verify the accuracy and completeness of the data.

- Check the effectiveness of the retailer’s internal controls for managing inventory.

- Confirm the correct valuation and account for it in the financial statements.

- Evaluate the accuracy and completeness of inventory-related disclosures in the financial statements.

- Identify any weaknesses or deficiencies in the retailer’s inventory management processes.

Example #2

In August 2021, the International Olympic Committee (IOC) announced they had commissioned an AUP engagement to verify the data provided by the Tokyo Organizing Committee of the Olympic and Paralympic Games (TOCOG). The IOC requested an AUP engagement to ensure that the data provided by TOCOG regarding athletes’ participation and the competitions’ results were accurate and complete.

Agreed Upon Procedures vs Audit vs Consulting

Here are the differences between Agreed procedures, audit, and consulting points:

#1 – Agreed Upon Procedures (AUP)

- Agreed-upon procedure engagements are for a specific purpose, usually to address a particular concern or risk.

- The procedures in an AUP engagement are an agreement between the auditor and the client, which meets the client’s specific needs.

- The agreed-upon procedure report describes the procedures performed and the results obtained but does not provide an opinion or assurance on the overall financial statements or other information.

- AUP engagements are often less extensive than audits and may focus on specific data or processes.

#2 – Audit

- An audit is a comprehensive examination of an organization’s financial statements, internal controls, and compliance with laws and regulations.

- Audits are a requirement for public companies and may be optional for private companies.

- Auditors must express an opinion on the financial statements, assuring stakeholders that the financial statements are accurate and complete.

- Audits by generally accepted auditing standards (GAAS) may involve testing of internal controls, analytical procedures, and substantive testing of financial transactions.

#3 – Consulting

- Consulting services advise and assist organizations in a specific area, such as strategy, operations, or technology.

- Individuals or firms may perform consulting engagements with specialized expertise in a specific area.

- Consulting services may involve providing recommendations or advice on specific business processes or strategies but do not provide an opinion or assurance on the accuracy or completeness of financial statements or other information.

- Consulting engagements are not subject to the same level of regulation as audit or AUP engagements, but ethical and professional standards still apply.

Frequently Asked Questions (FAQs)

Are agreed-upon procedures attest services?

Yes, Agreed Upon Procedures engagements are considered to attest services. In an attest engagement, a practitioner (i.e., an auditor or accountant) performs specific financial or non-financial information procedures and provides a report describing the operations and results.

Is agreed-upon procedures an assurance engagement?

Yes, Agreed Upon Procedures engagements are considered assurance engagements. In an assurance engagement, a practitioner (i.e., an auditor or accountant) performs procedures to obtain evidence to support a conclusion, expressed in a report, about the reliability of an assertion being made by management.

What agreed-upon procedures explain its scope and objectives?

The scope and objectives of an engagement are tailored to the client’s specific needs, and the meeting provides users with relevant, reliable, and valuable information for decision-making. The objective is not to give an overall opinion or assurance on the financial statements or other information but to provide users with specific information about a particular area of concern or risk.

Are agreed-upon procedures an audit?

No, Agreed Upon Procedures engagements are not audits in the traditional sense. While audits are also an assurance service, they are performed by Generally Accepted Auditing Standards (GAAS) and involve the auditor obtaining sufficient evidence to provide an opinion on the overall financial statements.

Recommended Articles

This is a guide to what is Agreed Upon Procedures. We explain its examples, differences with audits and consulting, and checklists. You can learn more about accounting from the following articles –